Trulieve Offers An Excellent Entry

Summary

- I have followed Trulieve since it went public in 2018.

- The company has evolved from solely a Florida operator to one that is a big player in a few markets.

- The stock has fallen a lot since I called it out 3 months ago and is an extreme bargain.

- Looking for more investing ideas like this one? Get them exclusively at 420 Investor. Learn More »

Rex_Wholster

I called Trulieve (OTCQX:TCNNF) a timely buy in late February, but three months later, it has dropped 37.6% to a new all-time low close of $3.87. The analyst outlooks have deteriorated, but the stock has dropped too much in my view. While I remain cautious on the largest MSOs, I include a lot of this one in both of my model portfolios. Today, I discuss its operations and assess its announcement to exit two states, I review its two recent financial reports, I look at its valuation, and I look at its chart.

Operations

Last week, the company announced that it is closing its one dispensary in California and all of its operations in Massachusetts.

"These difficult but necessary measures are part of ongoing efforts to bolster business resilience and our commitment to cash preservation as we continue to focus on our business strategy of going deep in our core markets and jettisoning non-contributive assets," said Chief Executive Officer, Kim Rivers. "We remain fully confident in our strategic position and the long term prospects for the industry."

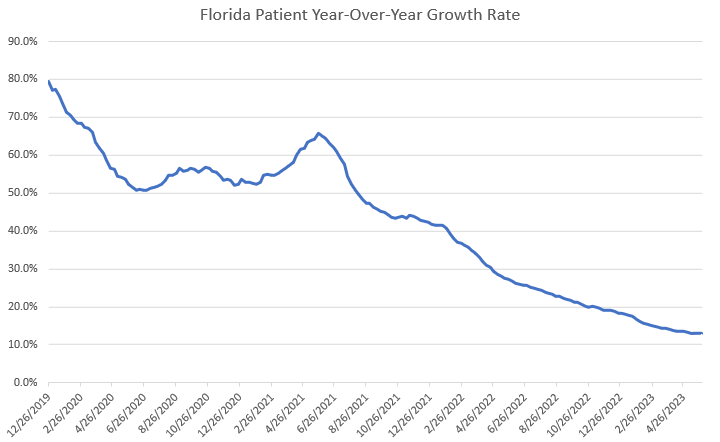

As I discussed in February, the company's largest operation is in its home state of Florida. I pointed out that the medical patient growth in that state has been plunging, and this remains the case. The annual growth has dropped from 15% to a new all-time low of 13%:

Alan Brochstein, Florida Office of Medical Marijuana Use

The 823K patients represent about 3.8% of the state's population, which is quite high.

Financials

In Q1, the company saw revenue shrink 9%, a remarkable change from a year ago, when its results were boosted by the acquisition of Harvest Health & Recreation and grew 64%. The company had been expected to generate revenue of $294 million and adjusted EBITDA of $84 million. Sales were slightly lower at $289 million, with adjusted EBITDA also lower than expected at $78 million.

The company provided financial targets of a small decline sequentially in revenue in Q2 with 2023 operating cash flow of $100 million and for the company to generate free cash flow for the year. In 2022, the company generated operating cash flow of only $23 million and spent $165 million on capital spending.

Going into the report, analysts had expected Q2 revenue to fall 6% to $300 million with adjusted EBITDA of $88 million, but now they project revenue will decline 11% to $285 million. Adjusted EBITDA is expected to be $76 million.

The outlook for 2023 going into the Q1 report was for revenue of $1.216 billion, down 2%, with adjusted EBITDA of $363 million, down 9%. Now the analysts expect revenue will drop 6% to $1.16 billion, with adjusted EBITDA falling 19% to $322 million. For 2024, the analysts had expected revenue of $1.293 billion with adjusted EBITDA of $398 million, a margin of 30.8%. Now they forecast revenue will grow 6% to $1.232 billion, 5% lower than before. Adjusted EBITDA is expected to increase 11% to $357 million, a drop of 10% from the prior forecast and a margin of 29.0%. Note that these estimates don't include any impact from the recently announced market exits.

Valuation

Trulieve currently trades at just 3.7X enterprise value to projected 2023 adjusted EBITDA. Of the leading MSOs, Curaleaf (OTCPK:CURLF) trades at 7.7X, Cresco Labs (OTCQX:CRLBF) trades at 6.6X, Green Thumb Industries (OTCQX:GTBIF) trades at 5.8X and Verano Holdings (OTCQX:VRNOF) trades at 4.2X. I think that the analyst estimates for margins are too high on Verano, which would mean that it trades at an even higher valuation.

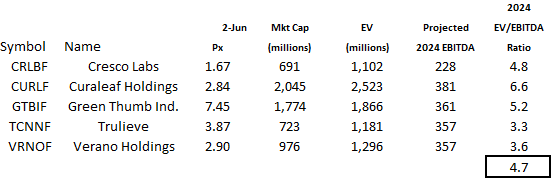

Here is a look at the 2024 valuation:

Alan Brochstein, using Sentieo

Trulieve now has the second-lowest market cap also the second-lowest enterprise value of the largest 5 MSOs. This valuation leaves it the cheapest relative to projected adjusted EBITDA in 2024. The five largest MSOs don't have a lot of tangible book value. The only two that are positive are GTBIF and TCNNF.

My target for TCNNF has dropped with the lower estimates. Before, I was targeting for year-end based on 7X a 28% adjusted EBITDA margin, which was $12.30. Based on the current projected revenue and using still a 28% adjusted EBITDA margin and still a 7X multiple of 2024 projected adjusted EBITDA, I get $345 million. This would give an enterprise value of $2.415 billion, which works out to a stock price of $10.47, up 170%.

The Chart

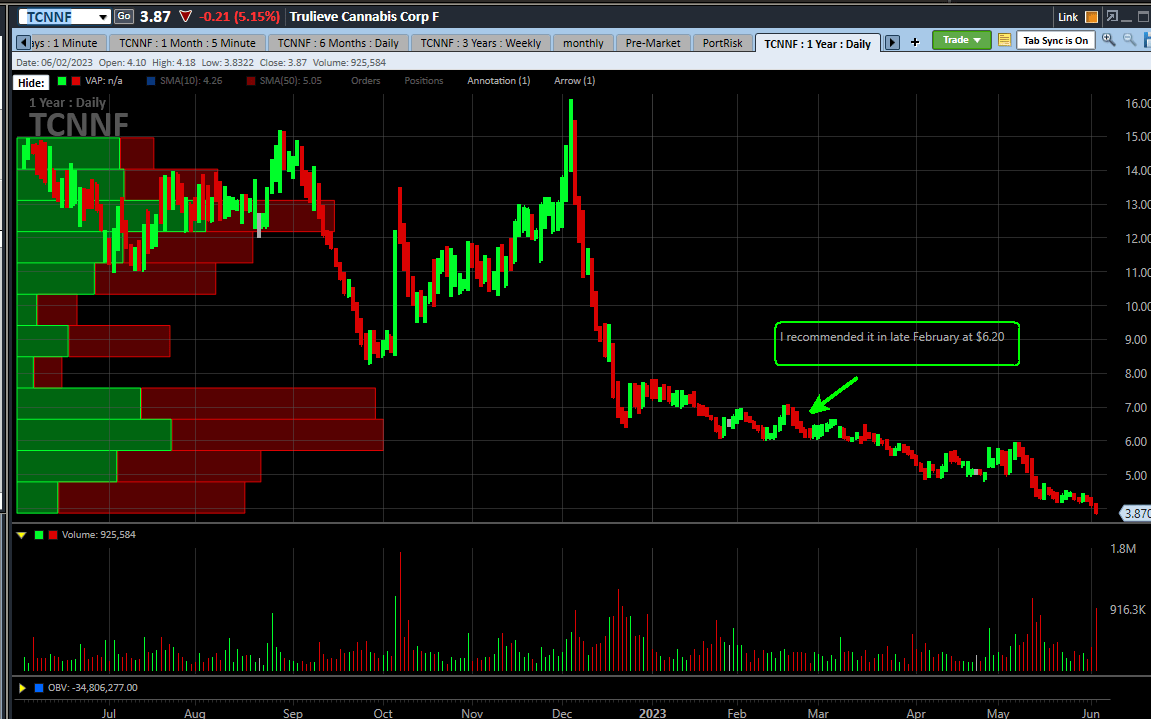

Over the past year, the stock has declined 73.4%, and it has plunged 74.1% from its peak in early December when the market was running up on SAFE Banking hopes:

Charles Schwab StreetSmart Edge

The stock has broken the $5 level and now the $4 level, which fell on very heavy volume Friday. The old all-time low, set in early 2020, had been $5.74, so it has set a new all-time low.

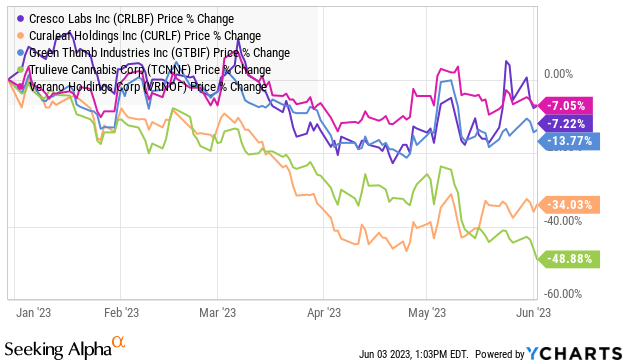

Here is how it looks against the other four large MSOs in 2023:

YCharts

The stock is down way more than its peers.

Conclusion

I am disappointed to have called it out before it bottomed, but the stock was down a lot when I wrote about it in late February. I think that the market is responding poorly to what I expected: lower margins.

The company is now at spot #4 in the AdvisorShares Pure US Cannabis ETF (MSOS) at 11.2%. The ETF reduced its shares held from 10.19 million at year-end, when it was 17.2% of the portfolio, to 9.68 million earlier this year. I am not expecting the ETF to add to TCNNF after the big decline, but it might. More importantly, the chances of them selling shares has dropped in my view.

Trulieve is the only large MSO that I include in my model portfolios, and I have substantial positions, to which I added on Friday. I think the recovery could be very strong and have a year-end target 170% higher than the current price.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

420 Investor launched in 2013, just ahead of Colorado legalizing for adult-use. We are moving to Seeking Alpha and will let our followers know when that occurs. Historically, we have provided great coverage of the sector with model portfolios, videos and written material to help investors learn about cannabis stocks.

This article was written by

Alan Brochstein, CFA, was one of the first investment professionals to focus exclusively on the cannabis industry. He has run 420 Investor, a subscription-based due diligence platform for investors interested in the publicly-traded cannabis stocks that he has moved to Seeking Alpha, since 2013, and he is also the managing partner of New Cannabis Ventures, a leading provider of relevant financial information in the cannabis industry since 2015. Alan is based in Houston. He and his wife have two adult children.

Before focusing exclusively on the cannabis industry in early 2014, Alan had worked in the securities industry since 1986, primarily with the responsibility for managing investments in institutional environments until he founded AB Analytical Services in 2007 in order to provide independent research and consulting to registered investment advisors. In addition to advising several different hedge funds and investment managers, including Friedberg Investment Management, where he participated as a member of its investment management committee, Alan was also a senior analyst for the independent research firm Management CV. In 2008, he began providing a first-of-its-kind subscription-based service for individual investors, Invest By Model, which offered two different portfolios that investors could replicate in their own accounts. Alan also offered The Analytical Trader at Marketfy, where he used fundamental and technical analysis in a disciplined process to offer specific trade ideas geared towards swing traders.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.