MUC Vs. NAC: Comparing California Quality Muni Funds

Summary

- The BlackRock MuniHoldings California Quality Fund invests primarily in a portfolio of long-term investment-grade municipal obligations, the interest on which is exempt from Federal and California income taxes.

- The Nuveen California Quality Municipal Income Fund invests in undervalued municipal securities that are exempt from regular federal and California income taxes.

- Both CEFs are reviewed and compared. Which has done better for investors has changed based on periods reviewed.

- I will also try to calculate how they both compare to a municipal bond CEF that invests nationally in quality bonds. The results are close.

- From what I found, California investors, especially those in the upper brackets, should consider owning MUC over NAC or a national municipal bond CEF.

- Looking for more investing ideas like this one? Get them exclusively at Hoya Capital Income Builder. Learn More »

Andrii Dodonov

(This article was co-produced with Hoya Capital Real Estate)

Introduction

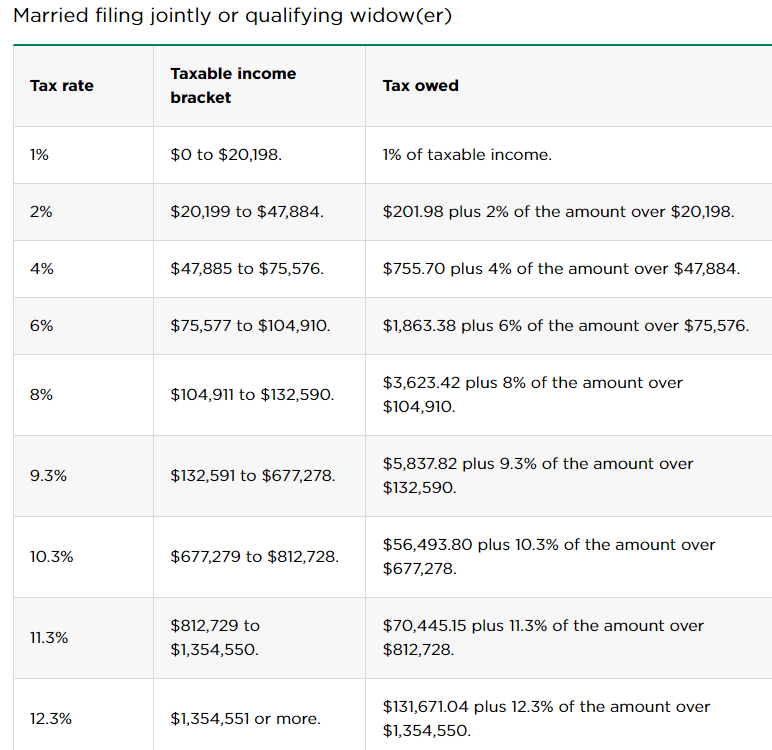

The next chart shows why many residents of California prefer Municipal bond funds that only invest in bonds that are exempt from state (and some local) income taxes.

nerdwallet.com

Single-filers would cut the bracket dollars in half. But there is more: California also levies a 1% mental health services tax on income exceeding $1 million, making the state's highest tax rate 13.3%. That gives these funds an after-tax advantage over a Nationally-invested Municipal bond fund.

Here, I will review funds from different managers who both follow a "quality" strategy in their portfolio construction.

- BlackRock MuniHoldings California Quality Fund (NYSE:MUC)

- Nuveen California Quality Municipal Income Fund (NYSE:NAC)

BlackRock MuniHoldings California Quality Fund review

Seeking Alpha describes this CEF as:

The Fund seeks to achieve its investment objective by investing primarily in a portfolio of long-term investment-grade municipal obligations, the interest on which is exempt from Federal and California income taxes. Under normal market conditions, the Fund invests at least 80% of its assets in investment grade municipal obligations with remaining maturities of one year or more at the time of investment. MUC started in 1997.

Source: seekingalpha.com MUC

MUC has $1.19b in AUM and shows a Forward Yield of 3.87%. Fees on Net Assets, as reported by BlackRock (3/31/23), come to 175bps, comprised of the following:

- Management fee: 91bps

- Interest expense: 73bps (recently annualized cost: 4.15%)

- Other costs: 11bps

MUC holdings review

BlackRock provides some basic information on the portfolio.

blackrock.com

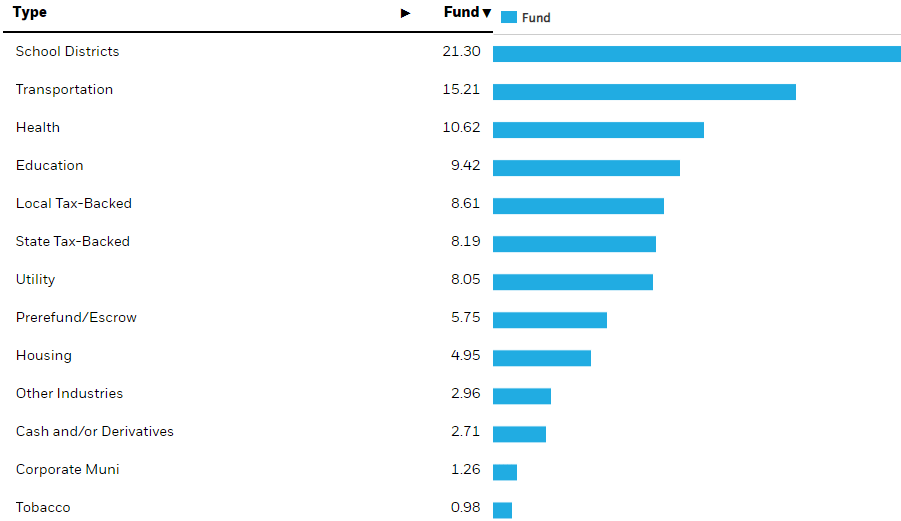

Currently, MUC holds about 4% in Puerto Rico bonds and has just under 4% in cash. The sector allocations are:

blackrock.com sectors

If you add School Districts and Local Tax-backed, at least 30% of the portfolio is not dependent on state-level debt and I suspect that percent is much higher as other sectors could represent local issues too.

All rated bonds are classified as investment-grade, with over 65% in the top letter ratings.

blackrock.com Ratings

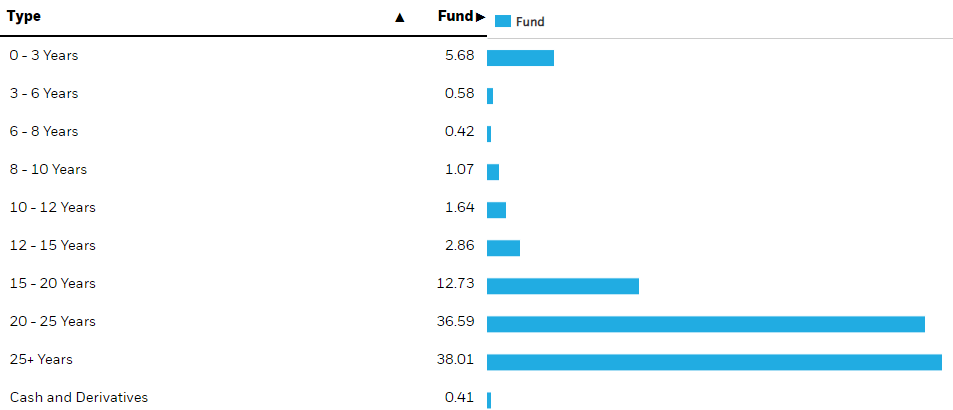

With most of the portfolio maturing after 20 years, MUC has a WAM of over 29 years; an Effective Duration over 15 years.

blackrock.com Maturities

Little of the portfolio matures in the near term which could have resulted in rising the WAC, which is currently at 4.06%. With rates the highest in years, it is unlikely many issuers would benefit from calling their bonds now to issue new ones.

blackrock.com Call schedule

Top holdings

BlackRock apparently does not like to divulge recent holdings in detail. The last full listing is from 1/31/23. Also, no data on biggest Issuers was provided.

blackrock.com

MUC distribution review

seekingalpha.com MUC DVDs

MUC has almost 34% leverage factor and I suspect the declining payouts are a result of the cost of using that leverage has climbed faster than MUC increased its coupon income. As of the end of March, the 3-month average coverage ratio was 104%, so hopefully investors won't see another cut. The Forward rate quoted assumes the current payout level will not change.

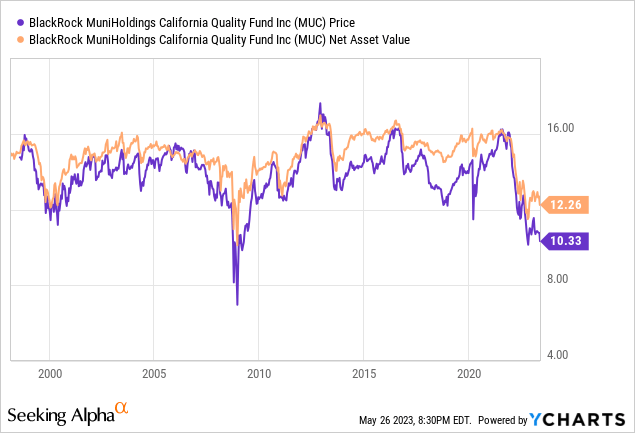

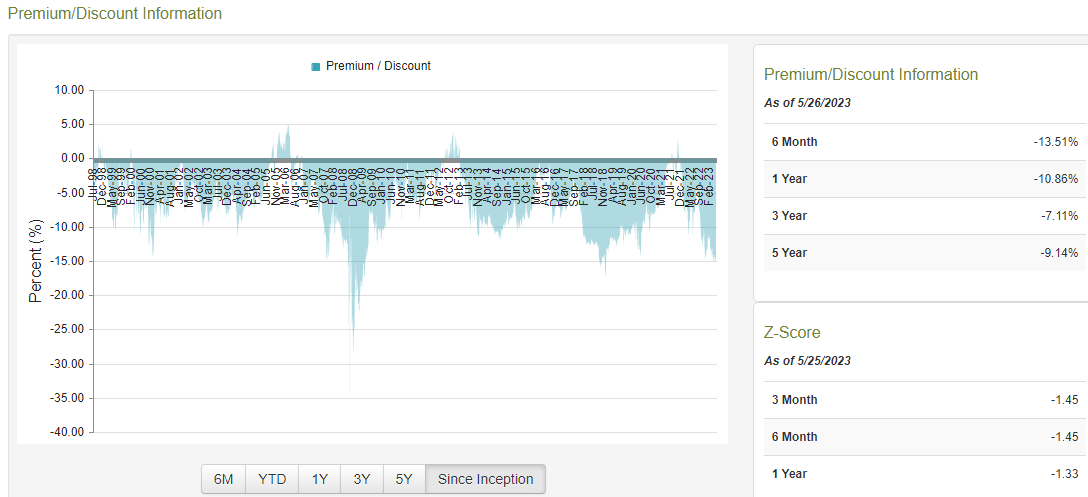

MUC price and NAV review

The NAV has been more stable than the price, resulting in deep discounts for investors to pounce on.

CEFConnect.com

MUC has seldom sold at a premium but the current discount at over 15% is one of the best investors have seen with MUC since 2018. Investors might be discounting this CEF for the issues facing the state: budget deficit, shrinking population, and climate issues. If that is true, the other fund should be showing the same results.

Nuveen California Quality Municipal Income Fund review

Seeking Alpha describes this CEF as:

The Nuveen California Quality Municipal Income Fund invests in undervalued municipal securities and other related investments that are exempt from regular federal and California income taxes. It primarily invests in securities that are rated Baa or BBB or better. The Fund will primarily invest in municipal securities with long-term maturities in order to maintain a weighted average maturity of at least 15 years. NAC started in 1998.

Source: seekingalpha.com NAC

NAC has $1.79b in AUM and shows a Forward Yield of 4.15%. As of the end of April, fees have climbed to 307bps from these costs:

- Manager fees: 94bps

- Other expenses: 5bps

- Interest fees: 208bps

The leverage ratio is around 40% and the last report leveraging cost is 4%. That could indicate the fees for MUC are out-of-date.

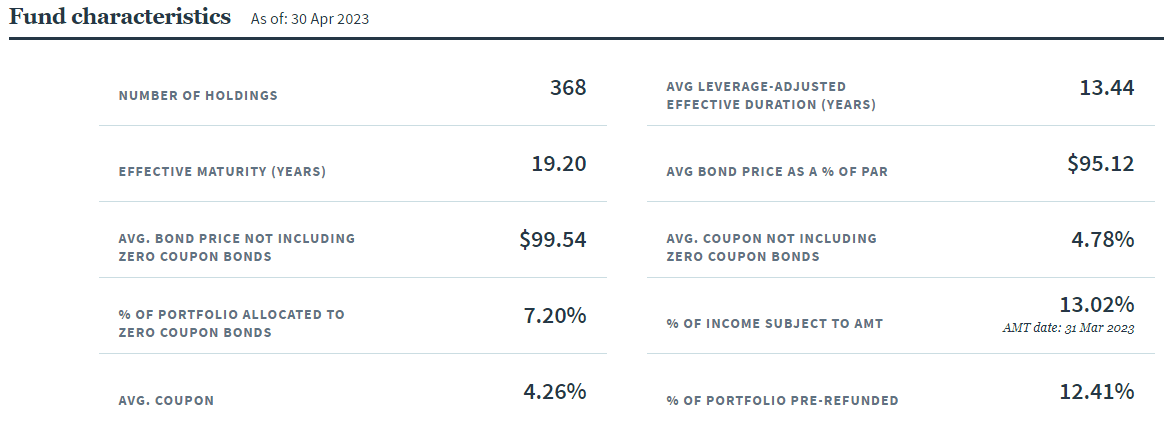

NAC holdings review

Nuveen provides some basic data around the fund's portfolio.

nuveen.com

The fact each manager can decide how to define their fund's holdings makes some comparison harder: sectors is one of them in this case.

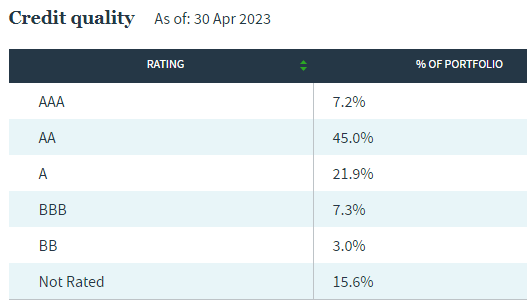

nuveen.com Sectors nuveen.com Ratings

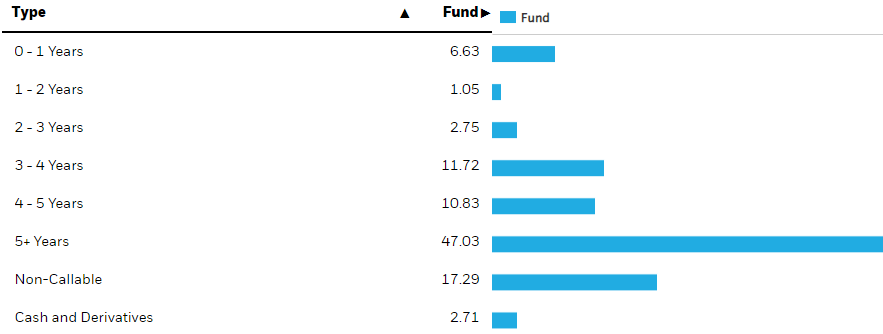

NAC's quality is overall below MUC's, with only 52% in the top two latter groupings. The maturity allocation results in slightly short duration and WAM values.

nuveen.com Maturities

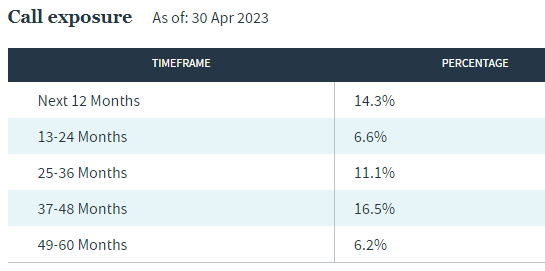

While 14% could be called over the next year, again the odds are against many happening.

nuveen.com Call schedule

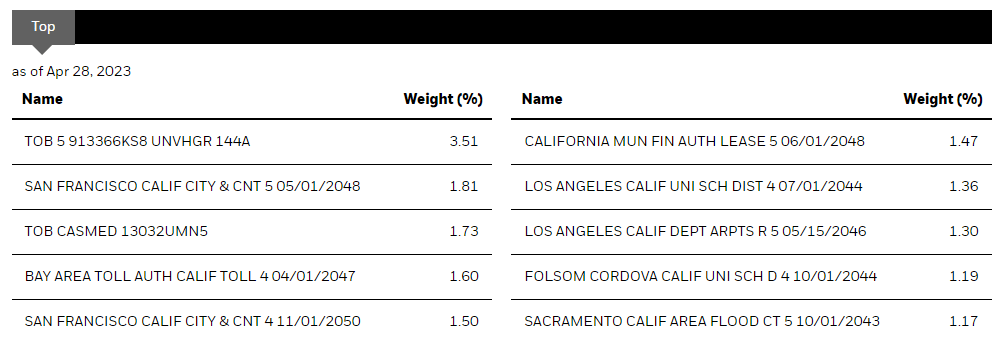

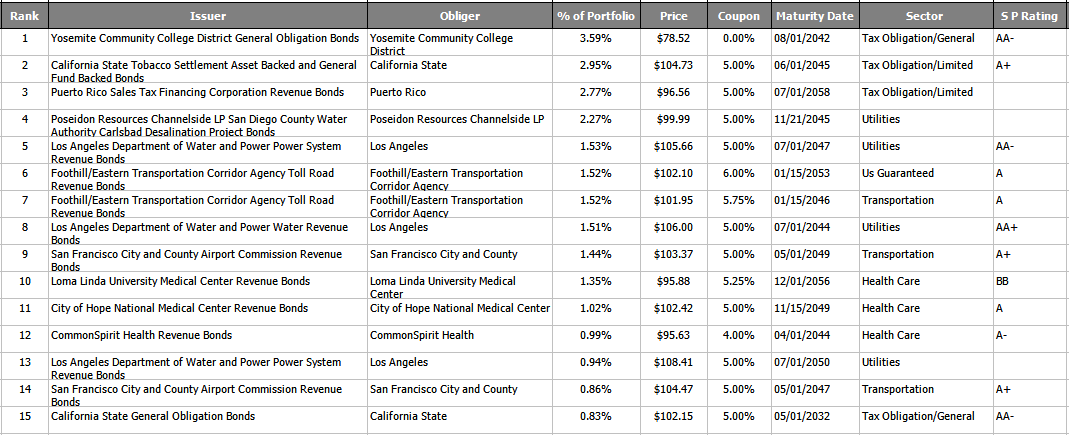

With access to the complete holdings and extra fields, I was able to calculate the Top 10 Obligors.

nuveen.com; compiled by Author

Top holdings

nuveen.com; compiled by Author

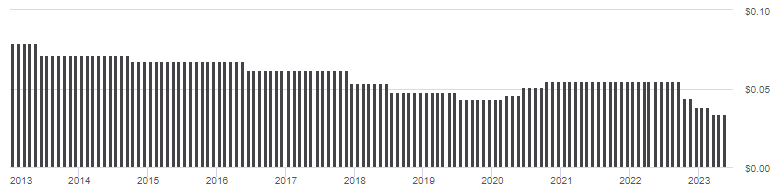

NAC distribution review

Nuveen also provides some basic data around the fund's distributions.

nuveen.com seekingalpha.com NAC DVDs

NAC's payouts are showing the same trend as the MUC fund; dropping even as rates are climbing. Not surprising really as there is little portfolio turnover and the cost of leveraging is the highest in a decade.

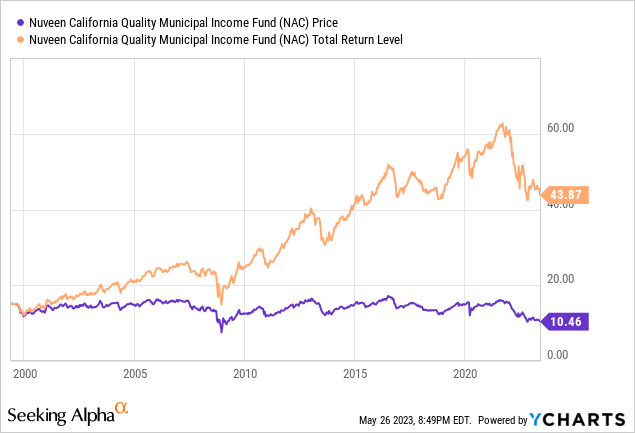

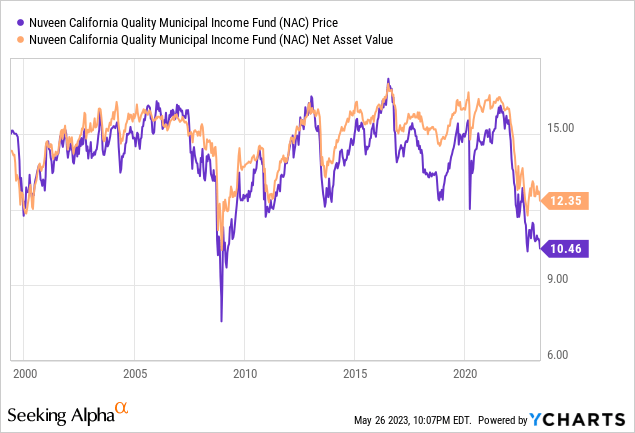

NAC price and NAV review

Like with MUC, the NAV hasn't been this challenged since the GFC back in 2008-09, which proved to be a great buying opportunity.

CEFConnect.com

Except for the discounts available during the GFC, NAC is also at levels not usually seen. It has also shown the ability to greatly reduce the discount from current levels, which isn't the case for some CEFs. Z-score data was not shown.

Comparing CEFs

| Factor | MUC CEF | NAC CEF |

| AUM | $1.19b | $1.79b |

| Fees | 175bps | 307bps |

| Forward Yield | 3.87% | 4.15% |

| Payout coverage | 104% | 109% |

| Average bond rating | AA- | A+ |

| Duration/Maturity | 15.28/29.36 | 13.44/19.20 |

| WAC | 4.06% | 4.78% |

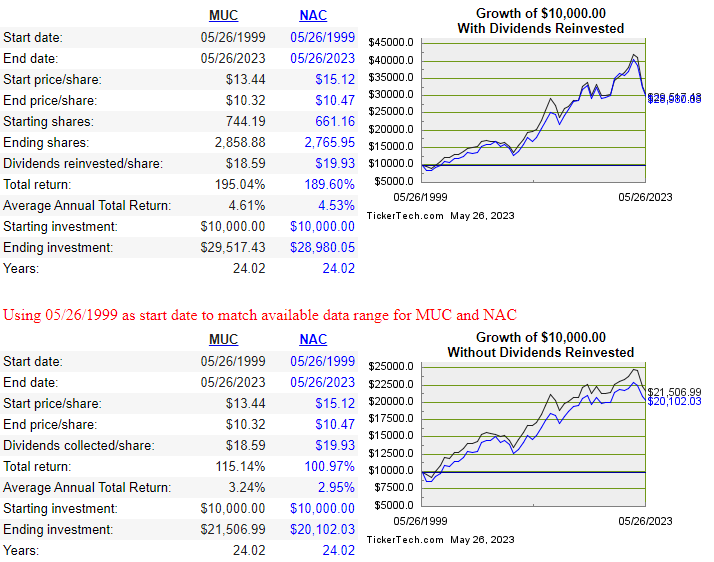

The next data shows how both CEFs performed based on whether the payouts were reinvested or not.

divdendchannel.com

The difference in Total return favors MUC in both strategies, but it is very small.

Portfolio strategy

Between these two CEFs, my preference would by MUC with its better return and currently much lower fees, though as I said earlier, those fees might not be fully reflecting the higher leverage cost.

As promised, I will now add the Nuveen Quality Municipal Income Fund (NAD), to try to see if California investors would have done better with a national Municipal Bond CEF even though taxes would be higher. Just over 7% of NAD is invested in California bonds.

PortfolioVisualizer.com

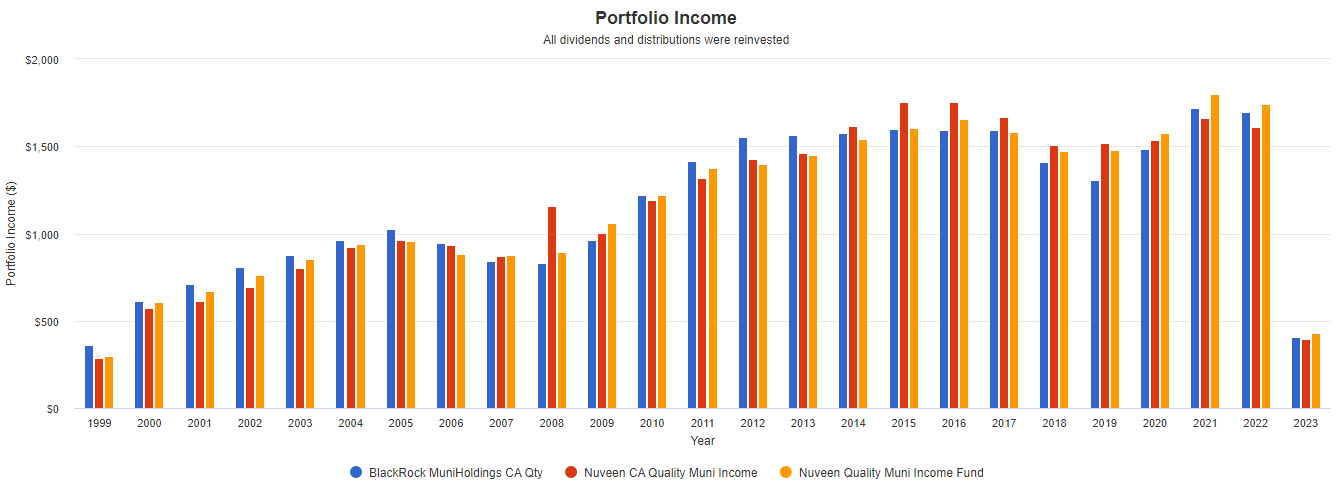

Income generated for each CEF was:

PortfolioVisualizer.com

Using the DividendChannel.com as a common source, we see dividends paid of $18.59 for MUC, $19.93 for NAC, and $19.91 for NAD. While the first two avoid CA taxes, about 93% of NAD probably does not, resulting in a post-tax level closer to $17.50 for a top-bracket tax payer. That's is about $.077 less than MUC annually; $.17 less than NAC. Using an average price of $10, NAD's tax-adjusted return appears close to what each of the other CEFs provided investors. This doesn't consider if local income taxes are also avoided, which would favor both MUC and NAC over NAD. From the "back of the envelope" analysis, the higher your California income, the more those investors should stay "home".

Final thoughts

From what I found, California investors, especially those in the upper brackets, should consider owning MUC over NAC or a national municipal bond CEF.

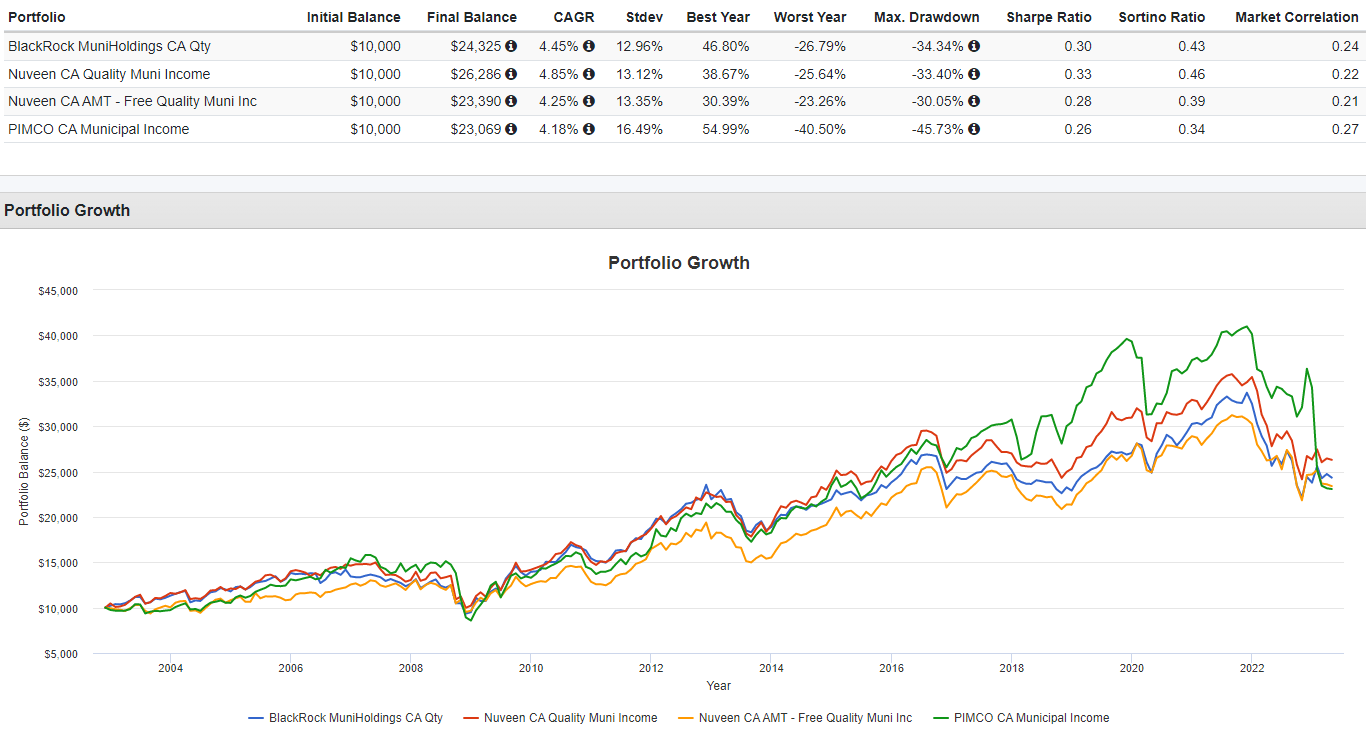

There are other California Municipal Bond CEFs to consider, two of which I covered in my NKX Vs. PCQ: Comparing CA-Only Muni CEFs article. These are good for investors subject to the AMT. Here is how they compare to MUC and NAC.

PortfolioVisualizer.com

Since 2002, trying to avoid the AMT system has not been a good strategy. Also, both MUC and NAC hold low levels of bonds subject to the AMT process.

I ‘m proud to have asked to be one of the original Seeking Alpha Contributors to the 11/21 launch of the Hoya Capital Income Builder Market Place.

This is how HCIB sees its place in the investment universe:

Whether your focus is high yield or dividend growth, we’ve got you covered with high-quality, actionable investment research and an all-encompassing suite of tools and models to help build portfolios that fit your unique investment objectives. Subscribers receive complete access to our investment research - including reports that are never published elsewhere - across our areas of expertise including Equity REITs, Mortgage REITs, Homebuilders, ETFs, Closed-End-Funds, and Preferreds.

This article was written by

I have both a BS and MBA in Finance. I have been individual investor since the early 1980s and have a seven-figure portfolio. I was a data analyst for a pension manager for thirty years until I retired July of 2019. My initial articles related to my experience in prepping for and being in retirement. Now I will comment on our holdings in our various accounts. Most holdings are in CEFs, ETFs, some BDCs and a few REITs. I write Put options for income generation. Contributing author for Hoya Capital Income Builder.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.