Fox Factory Holding: A Reassessment Given Current Conditions

Summary

- Fox Factory Holding Corp is doing quite well, though the firm's bottom line has suffered as of late.

- Fortunately, management has a positive outlook for the company for this year, but this doesn't make it a great prospect.

- Given how shares are priced and considering current market conditions, additional caution is not a bad idea.

- Looking for a helping hand in the market? Members of Crude Value Insights get exclusive ideas and guidance to navigate any climate. Learn More »

nicolamargaret/E+ via Getty Images

As an investor, it's important to remain flexible in your thinking. You should never be ashamed to change your stance on an investment prospect if the data calls for it. I used to struggle with this a lot when I first got into the investment industry. But as time progressed, self-reflection became easier. And while I wish I never needed to change my stance, I do so more readily now than ever before. This article is about one such instance. And that involves a business called Fox Factory Holding Corp. (NASDAQ:FOXF). For those who don't know, Fox Factory engages in the production of products and systems that are used in equipment such as bikes, on-road vehicles, trucks, snowmobiles, and more. Recently, financial performance for the company has been a bit mixed, but management remains optimistic about the future. Even so, this, combined with how shares are priced and combined with changing market conditions, has led me to take a more cautious approach to the firm. The end result here has been my decision to downgrade FOXF stock from a ‘buy’ to a ‘hold’ to reflect my view that its return prospects for the foreseeable future should be more or less in line with what the broader market should experience.

Assessing recent weakness

Back in early November of last year, I found myself revisiting Fox Factory to see whether or not it made sense to keep the company rated a ‘hold’. Despite volatility leading up to that point, I felt as though the fundamentals of the company were strong enough to upgrade the company to a ‘buy’. So far, that call has not worked out exactly as I had hoped. While the S&P 500 is up 10.2% since the publication of that article, shares of Fox Factory have seen downside of 0.1%.

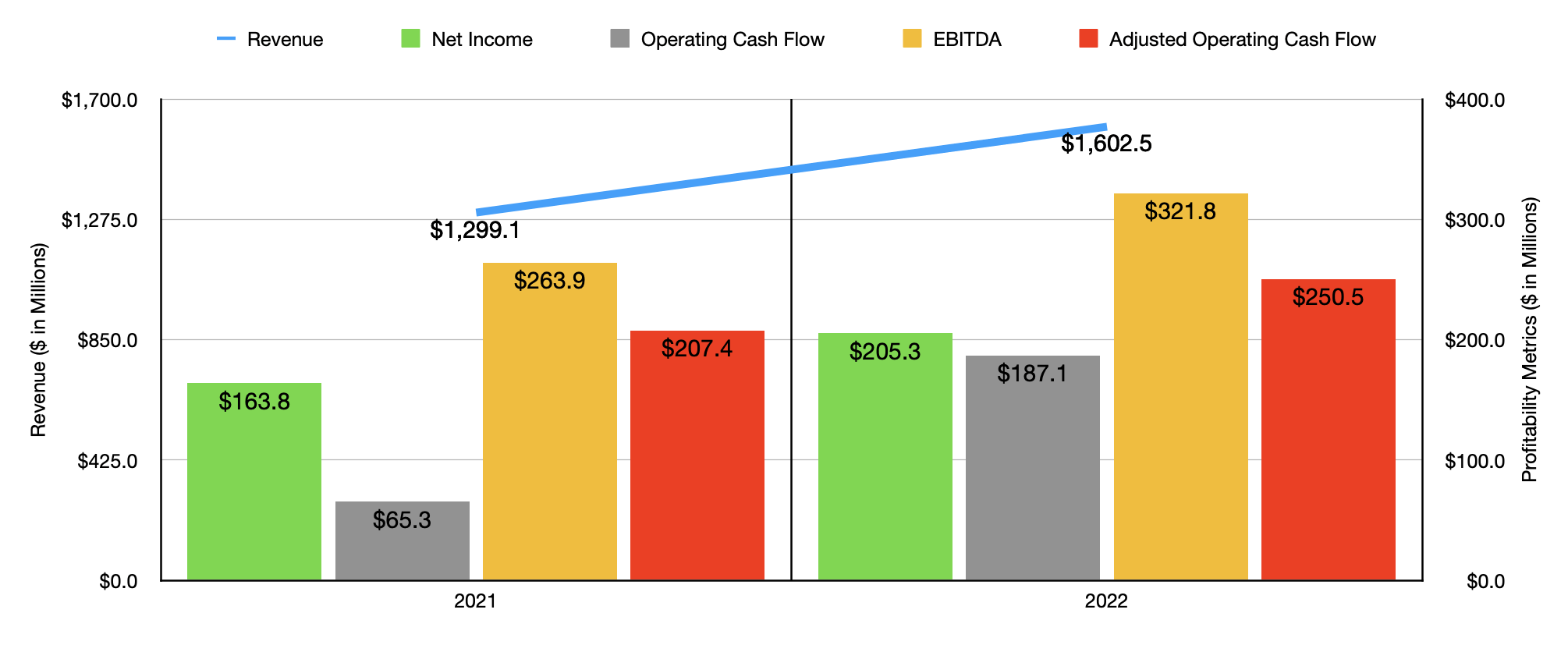

Author - SEC EDGAR Data

This return disparity may seem odd to those who look at just the annual data reported by management. Consider, for instance, the chart above. During 2022, revenue for the company came in at $1.60 billion. That's 23.4% above the nearly $1.30 billion reported one year earlier. Profits during this time increased nicely, popping up from $163.8 million to $205.3 million. And all other profitability metrics followed suit as the chart demonstrates.

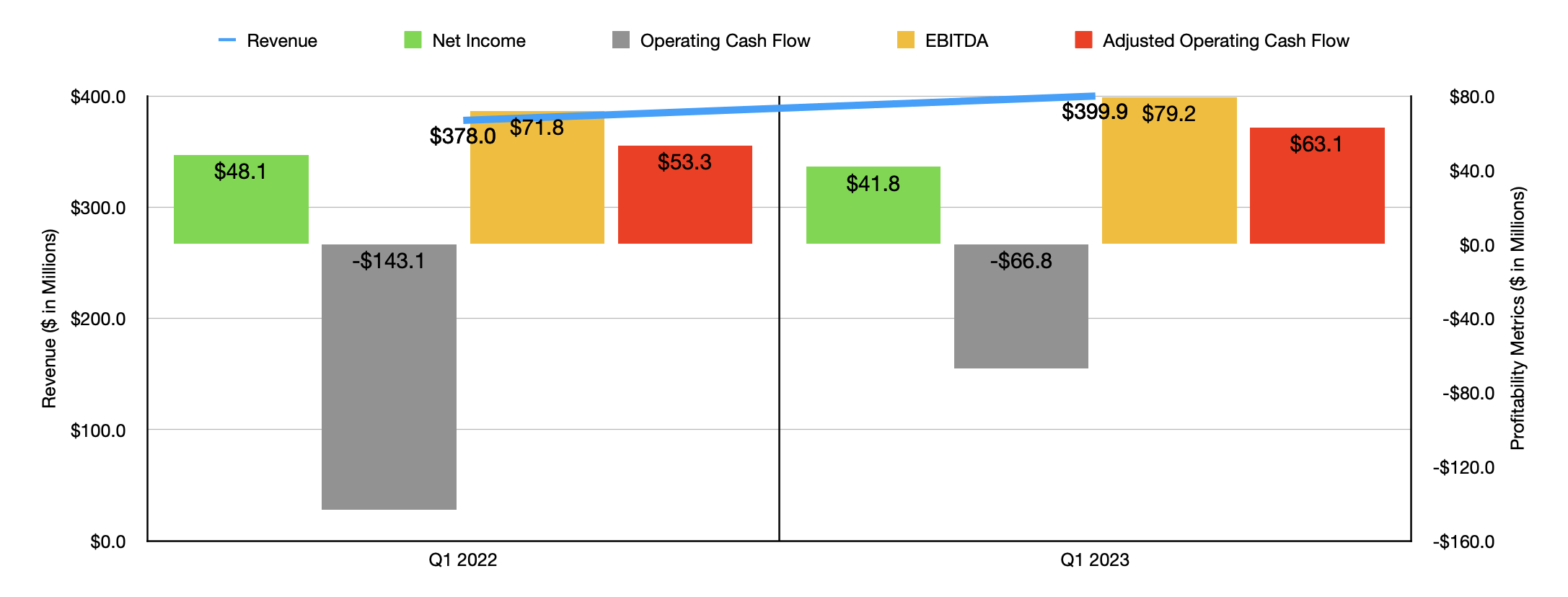

Author - SEC EDGAR Data

But when you start looking at more recent data, the picture is not quite as positive. During the first quarter of 2023, sales came in at $399.9 million. That translated to a sizable increase of 5.8% over the $378 million the company reported one year earlier. Interestingly, this rise in revenue came even as sales associated with the company’s Specialty Sports products plunged 30% from $169.9 million to $118.9 million. That drop, according to management, was driven by a return to seasonality and pre pandemic market conditions. Clearly, during the pandemic, customers invested heavily in these types of offerings. Fortunately, this drop was more than offset by a 35% surge in revenue associated with the company’s Powered Vehicle products. This brought sales up from $208.1 million to $281 million. Even though the company reported a decrease in demand associated with its OEM customers, it experienced strong performance in its upfitting product lines.

The revenue is not exactly the problem though. The bigger issue is the volatility the company experienced on its bottom line. Consider net income. During the first quarter of the year, Fox Factory reported net profits of $41.8 million. This was down from the $48.1 million reported one year earlier. This decline came even as the company's gross profit margin improved from 31.8% to 33.3%. The bigger problem came from increases elsewhere. One of these investors should be completely fine with. And this is research and development. This grew from 3.3% of sales to 3.8%. I rarely have a problem with higher research and development costs since, in theory, it is essentially an investment in the company's future. However, at the same time as this, general and administrative costs expanded from 6.8% of sales to 8.4%. This rise, according to management, was driven by higher employee headcount and benefit related costs, an increase in legal and professional fees, and higher insurance and facilities costs.

Although net profits worsened during this time, overall cash flows for the company were better off. Operating cash flow, for instance, went from negative $143.1 million to negative $66.8 million. If we adjust for changes in working capital, we would see this number improve from $53.3 million to $63.1 million. And finally, EBITDA for the enterprise expanded from $71.8 million to $79.2 million.

Despite the troubles on the bottom line so far, management has high hopes for the future. For 2023 as a whole, revenue is expected to come in at between $1.67 billion and $1.70 billion. Some of this increase over the $1.60 billion reported for 2022 will likely be chalked up to the acquisition of Custom Wheel House that the company announced in February of this year. That enterprise came at a total cost to the company of $131.6 million. That's fairly small, but it should add to the firm's top line. On the bottom line, the expectation is for earnings per share of between $5 and $5.30. At the midpoint, that would translate to net income of $218.9 million. That's a decent increase over the $205.3 million reported for last year. Unfortunately, we don't have any guidance when it comes to other profitability metrics. But if we assume that they will increase at the same rate that net income is forecasted to, we should anticipate adjusted operating cash flow of $267.1 million and EBITDA of $343.1 million.

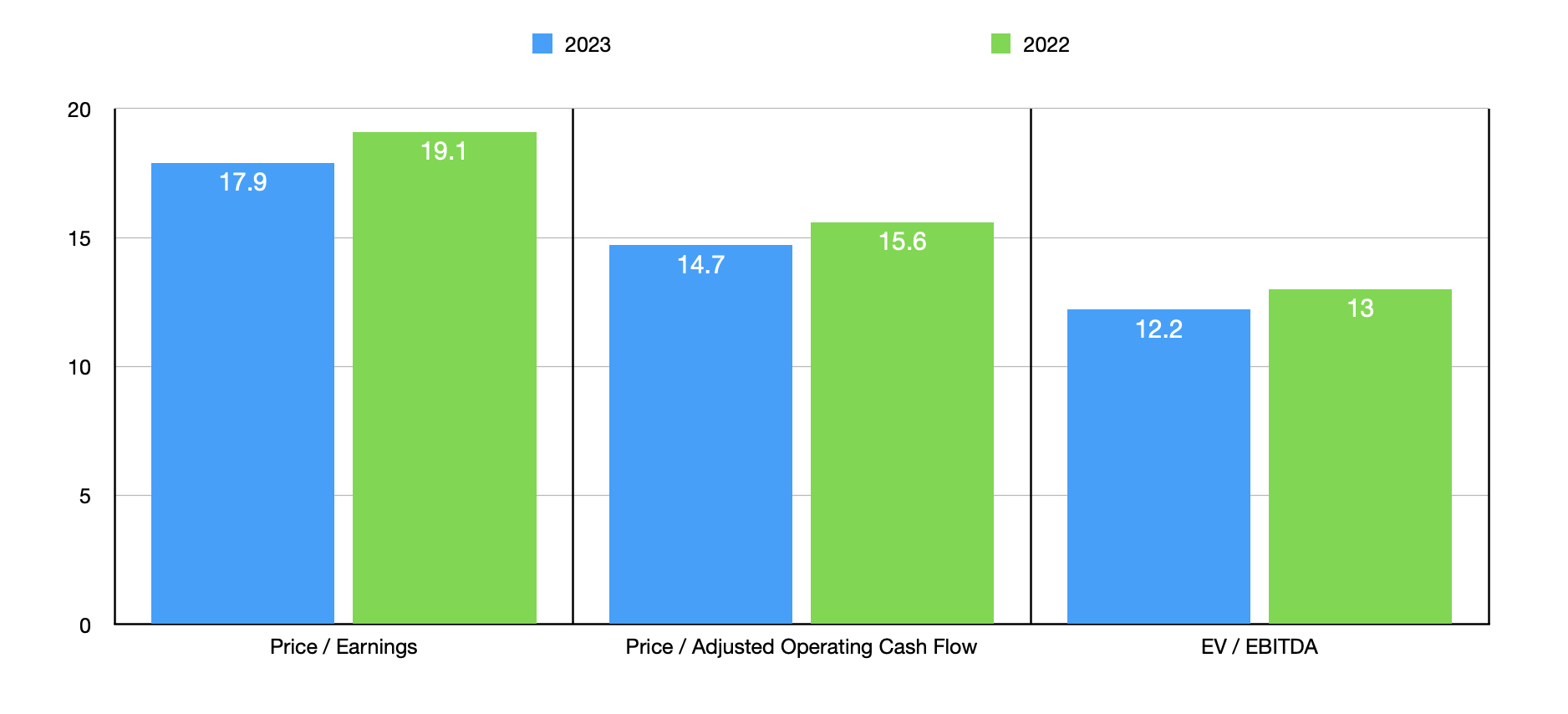

Author - SEC EDGAR Data

As you can see in the chart above, I took these estimated figures and priced the company on a forward basis. I also priced the company using data from 2022. As part of my analysis, I also, in the table below, compared the company to five similar firms. On a price to earnings basis, I found that two of the five firms were cheaper than Fox Factory. When it comes to the price to operating cash flow approach, three were cheaper. And when it comes to the EV to EBITDA approach, four ended up being cheaper.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Fox Factory Holding Corp. | 17.9 | 14.7 | 12.2 |

| Modine Manufacturing (MOD) | 9.9 | 13.9 | 8.6 |

| Dorman Products (DORM) | 30.2 | 62.1 | 17.8 |

| LCI Industries (LCII) | 13.6 | 5.2 | 8.9 |

| Adient (ADNT) | 267.0 | 7.7 | 7.5 |

| Visteon (VC) | 29.0 | 23.2 | 12.0 |

Takeaway

In the grand scheme of things, the picture facing Fox Factory is still fundamentally decent. This year should be better than last year if management is correct. However, in the light of changing market conditions, I am taking a more cautious stance on investments in general. Given how shares are priced, the company is not exactly the cheapest opportunity on the market. This is true on both an absolute basis and relative to similar firms. When you combine that with the bit of pain that the company saw on its bottom line and my overall cautious approach in this market, I believe that a more appropriate rating for the company at this time is a ‘hold’.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!

This article was written by

Daniel is an avid and active professional investor. He runs Crude Value Insights, a value-oriented newsletter aimed at analyzing the cash flows and assessing the value of companies in the oil and gas space. His primary focus is on finding businesses that are trading at a significant discount to their intrinsic value by employing a combination of Benjamin Graham's investment philosophy and a contrarian approach to the market and the securities therein.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.