KBR: Leading The Industry With Sustainability

Summary

- KBR has become an industry leader through its sustainability initiatives.

- The company's strong history with business growth through acquisitions and mergers gives it a good reputation to continue growing.

- However, the company's high dependency on technological innovation and threat of potential cybersecurity breaches is a risk to the company's growth.

Just_Super

Investment Thesis

KBR, Inc. (NYSE:KBR) is an engineering and technology services company that prides itself over its strong sustainability initiatives, becoming an industry leader in sustainability efforts. In addition, the company’s successful history of mergers and acquisitions gives the company a good edge to continue growing with future mergers. The company still has room to grow and I believe that once KBR is able to capitalize on its growth opportunities, the company will start to see an increase in sales and as a result, increase in company valuation.

Business Overview

KBR provides technology, engineering, and logistic solutions to governments and companies around the world. Their services and capabilities include scientific research, defense systems engineering, operational support, and data analytics. Their business model is targeted towards focus areas: government and sustainable technology.

Government

KBR delivers support solutions to defense, intelligence, and aviation programs for many military and government agencies. Their services in this area include systems engineering, cyber analytics, global supply chain management, and advanced prototyping. Their main customers include the US Army, Navy and Air Force as well as UK agencies such as the London Metropolitan Police and UK Crown Services.

Sustainable Technology

KBR also develops and provides solutions for corporate sustainability. This includes consulting services focused on broad-based energy transition and net-zero carbon emission solutions. Their key customers in this area include commercial and industrial companies.

Industry Overview

The engineering services market is valued at $1095.84 billion as of 2022 and it is expected to reach $1530.82 billion in the next five years, with a compound annual growth rate of 6.2%. Although the growth of this market is not as big as other industries, this industry has become a very stable market with consistent demand in services such as product engineering, process engineering, and financial engineering.

One of the main drivers of growth in this market is the integration of new emerging technologies such as cloud computing, machine learning, and artificial intelligence. The cloud computing industry is valued at $483.98 billion and is expected to grow with a compound annual growth rate of 14.1% from 2023 to 2030 while the machine learning industry is valued at $26.02 billion and is predicted to grow to $255.91 billion by 2030 with a compound annual growth rate of 36.2%. The adoption of these new technologies will help many engineering companies process and analyze lots of data in real time to make better decisions and enhance their service quality, but also allow these companies to maintain a competitive position in the market.

However, government regulations such as changes in laws may have a negative impact on the industry growth and demand for engineering services.

Competitive Advantage

With an industry so big and so valuable, KBR operates in a very competitive environment, with big competitors such as V2X (VVX), Fluor (FLR), AECOM (ACM), SAIC (SAIC). However, I see that KBR is able to differentiate itself based on two main areas: its sustainability initiatives and leadership and its strong record of successful mergers and acquisitions.

Sustainability Initiatives

Sustainability is a fundamental core value to the company’s activities and its mission. As the company puts it, ““We take pride in our role supporting industries, governments and citizens around the world to achieve the greatest advancements economically, socially and environmentally.” The company has proven to be an industry leader in sustainability initiatives with 3 consecutive years of carbon neutrality, 24% of revenues focused on sustainability, and a $1.9 billion environment impact. In addition, not only does the company focus on environmental sustainability, but it also puts an emphasis on sustainability among its workforce. KBR is committed to its Zero Harm culture which prioritizes the safety and well-being of its employees and eliminates any risks that could cause harm in the workplace. The company has achieved 89% Zero Harm Days out of a year, which equals 324 days.

Success In Mergers and Acquisitions

In addition to its strong sustainability leadership, the company also has a successful record of acquisitions, mergers, and joint ventures. Some of its notable ventures include its acquisition of VIMA, which is a leading provider of digital transformation solutions to military and defense clients, and its joint venture with Elbit Systems called Affinity joint venture which operates and maintains aircrafts and aircraft-related assets. These ventures allow KBR to have more flexibility in their services based on the expertise of their partners or acquired companies.

Growth Opportunities

Local Ventures and Collaborations

With KBR being a global company that provides its services to 34 countries, an opportunity arises for the company to explore ventures with the local players. These local companies will bring their local expertise to the table in terms of local strategy and market optimization as well as help KBR to avoid the uncertainty of different government regulations. With the success of mergers and acquisitions, this can be a very lucrative opportunity for KBR to capitalize on.

Defense Spending and Political Instability

One of KBR’s core business segments includes government solutions. In December of 2022, President Biden signed a $1.7 trillion Consolidated Appropriations Act of 2023 which included $858 billion in US defense spending. National security and defense has always been one of, if not the top priority for the US government. The US defense budget includes many measures to improve emerging technologies such as cybersecurity, artificial intelligence, and biotechnologies, many of which KBR provides services for. Also, with the defense budgets driven by political instability and the uncertainty of military conflicts, opportunities will continue to present themselves with the need for governmental solutions that align with the nation’s top priorities.

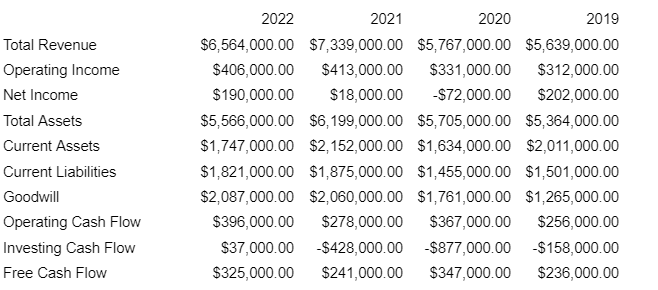

Financials

yahoo finance

The company’s financials are fairly stable with healthy sales and cash flow and the consistent increase in goodwill shows KBR’s success with mergers and acquisitions as well as the company’s growth. However, there are a few things that I would like to point out. The first thing is operating margins. The company seems like it has pretty high operating costs with a margins of only 6.40%. However, when compared with competitors in the industry such as V2X and AECOM with margins of 1% and 5% respectively, the KBR’s operating margins are on the high end. The other thing is the decrease in liquidity of the company over the last four years as the current ratio has dropped from 1.34 in 2019 to 0.96 in 2022. However, I don’t think this will be a very big problem as the company has good positive free cash flow that it can use to help with the expansion of the business.

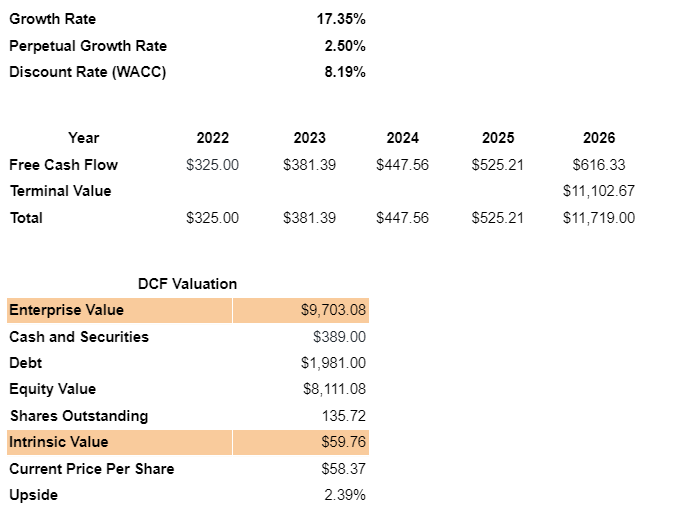

Valuation

I have performed a discounted cash flow analysis below for the valuation of the company. I used the compound annual growth rate of the company for the growth rate in this model and I used a 2.5% perpetual growth rate to match the stable growth of the economy. For the discount rate, I have used the company’s weighted average cost of capital. Currently, the company seems to be fairly valued with a price target of $59.76, but there is still lots of room to grow, especially with the consistent demand from the government caused by the political tensions.

calculations done by author

Risks

High Dependency on Technological Innovation

Although technological innovation and the development of emerging technologies in their services has been one of KBR’s strengths, it is nevertheless as much of their business is dependent on this new technology innovation. The company must continually develop and invest in new technology systems and platforms in order to maintain a competitive position in such a competitive industry. As a result, this will increase the company’s research and development costs, which may explain the company’s slim margins.

Cybersecurity/Privacy Breaches

The nature of the company’s services, especially with its government sectors, deals with a variety of sensitive information, including personal information, protected health information, and financial information. This means that the company is at risk of being exposed to cyber and security threats including computer viruses, phishing attacks, and hacks. This would not only put the company at risk but also its customers at a high risk, which would in turn heavily damage the reputation and brand image of KBR.

Overall Competitive Nature of the Market

The overall engineering and technology services market itself is very competitive both domestically and globally. The company not only competes with larger companies that have more resources and larger market share, but they also must outcompete smaller companies that are able to specialize in certain services and concentrate their resources on particular areas. In addition, the company is also competing against the US government’s own capabilities as it must provide higher quality services in order to give value to the government.

Conclusion

I would rate KBR stock as a hold but keep this stock on your watchlist. The company has shown that it is able to maintain a competitive position among its industry with more room to grow through government spending and local business collaborations. Despite its low margins, KBR’s financials have been pretty stable, with the exception of 2020 during the COVID-19 pandemic, putting the company in a good position to continue growing.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.