Huron Consulting Group: A Multi-Year Breakout Stock

Summary

- Huron Consulting Group posted its Q1 FY23 results with significant revenue growth.

- HURN stock has given a multi-year breakout and looks very bullish.

- It has great growth potential, and I believe it can reach $100 in the coming times.

- I assign a buy rating on HURN.

VioletaStoimenova/E+ via Getty Images

Huron Consulting Group (NASDAQ:HURN) is a professional firm that offers consultancy services globally. They work in three segments: Education, Healthcare, and Commercial. In the education segment, they offer colleges and universities digital solutions, analytic-related services, and organizational transformation services. In the healthcare segment, they offer advisory services, care transformation, financial advisory, software products, and long-term care. In the commercial segment, they deliver software products and offer digital services. HURN announced its Q1 FY23 results. I will analyze its quarterly results and talk about its growth potential in this report. The company's share has given a multi-year breakout, and I think it is a great buying opportunity. I assign a buy rating on HURN.

Financial Analysis

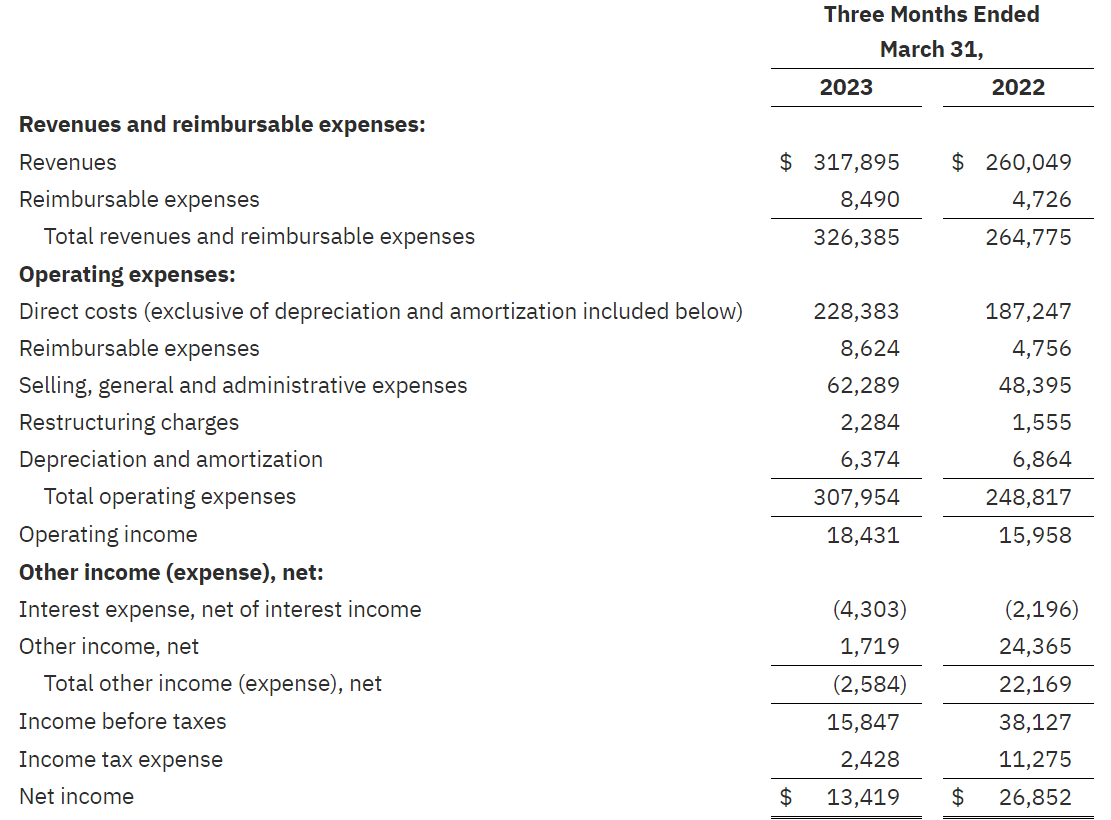

HURN posted its Q1 FY23 results. The revenues for Q1 FY23 were $317.9 million, a rise of 22.2% compared to Q1 FY22. I believe outperformance in all three segments was the major reason behind the revenue increase. Talking about the Healthcare segment: The revenues from the healthcare segment rose by 22% in Q1 FY23 compared to Q1 FY22. I believe strong demand for its digital capabilities and consulting and managed services driven by strong demand for its financial advisory offerings was the major reason behind the rise. The revenues from the education segment rose by 29.1% in Q1 FY23 compared to Q1 FY22. I believe strong growth in its digital offerings in education was the main reason behind the revenue increase in its education segment. Their digital offerings grew by 40% in Q1 FY23 compared to Q1 FY22. Finally, the revenues from the commercial segment rose by 12.5% in Q1 FY23 compared to Q1 FY22, driven by strong demand for its financial and advisory offerings.

HURN's Investor Relations

However, its operating income margin saw a decline. In Q1 FY23, the operating income margin was 5.8% which was 6.1% in Q1 FY22. I believe the drop was mainly due to a decline in operating income margins in the healthcare segment. The healthcare segment accounted for 47% of the company's total sales in Q1 FY23, and the operating margin in the healthcare segment in Q1 FY23 was 21.6% which was 23% in Q1 FY22. I think the decrease was due to the increased contractor expenses. The net income for Q1 FY23 was $13.4 million, which was $26.8 million in Q1 FY22. In Q1 FY22, there was a non-recurring $19.8 million gain, so if we exclude it, then the net income in Q1 FY23 increased by 91.4% compared to Q1 FY22. Their financial performance was impressive; they achieved 22% sales growth, and if we exclude the non-recurring gain, its net income also saw a significant rise; if they can maintain the growth rate in the coming times, then I think we can see a significant upside in the stock price.

Technical Analysis

Trading View

HURN is trading at the $83 level. The stock is looking super bullish; last month, it broke out of its all-time high of $84, which it created in 2008. So the stock has given a breakout after 15 years and is currently consolidating near $84. I am using monthly time frame analysis, which I consider the strongest time frame for making investment decisions. So if there are investors who invest solely based on technical analysis, this can be a great investment opportunity. My target for the stock based on the technical chart is $100.

Should One Invest In HURN?

The healthcare and education sector in which they serve has a great growth potential. Currently, the healthcare and education sectors are facing several challenges, and if the company can capitalize on this opportunity, then it can be quite beneficial for them. Talking about the healthcare sector is facing issues like worsening payer mix, and there is a growing demand for digital solutions in the healthcare sector to improve patient outcomes. The healthcare and education industry is growing rapidly, and I believe this might benefit HURN if they successfully capitalize on the opportunity. In addition, they are expanding their business in India, one of the biggest growing economies in the world, and as per the Bloomberg report, there is a 0% probability of India going into recession. So I think the company's presence in India will surely benefit them with many growth opportunities. The management has provided FY23 revenue guidance of around $1.27 billion, which is 12.3% higher than FY22 revenues. I have a strong belief looking at its growth potential, that it might achieve the revenue targets. In addition, the stock has given a multi-year breakout which is backed by great financials. I personally think it can reach $100 level in the next three months. Hence looking at the several positive indicators, I assign a buy rating on HURN.

Now looking at its valuation. HURN has an EV/Sales (fwd) ratio of 1.54x compared to the sector ratio of 1.6x and has a Price / Sales (fwd) ratio of 1.16x compared to the sector ratio of 1.27x. Although its valuation seems high, generally, high-growth companies trade at a high valuation, and I think HURN has solid growth potential.

Seeking Alpha

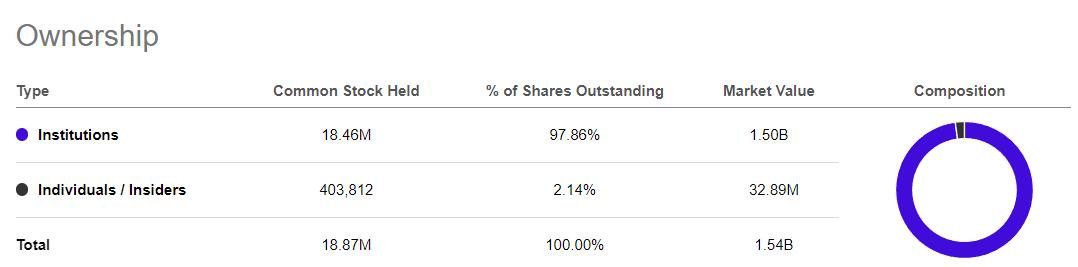

The shareholding pattern of HURN also looks excellent, with institutions owning 97.8% shares in the company. I personally prefer investing in companies where institutions hold at least 60% stake in a company because where institutions hold the majority of the stake, that company is considered safe for investing.

My Target Price

My target price for the stock is $100. Whenever a stock breaks its all-time high, there are no resistance zones or barriers to stop it. With a new breakout, several new buyers get added, and if the breakout comes after a long period, the buying momentum becomes even stronger; in this case, the breakout has come after 15 years. So the probability of the breakout being successful is high in this case, backed by strong fundamentals and low valuation. So I believe, looking at the strong momentum of the stock, it is around $83 with no resistance zone and barriers, so the next logical target for the stock becomes $100, and I believe there is a high probability that it might reach $100 in the coming times. My price target is based on its price action.

Risk

The amended credit agreement includes a senior secured revolving credit facility of $600 million. They have $290.0 million in outstanding debt on their revolving line of credit as of December 31, 2022, which matures on November 15, 2027, and is fully due and unpaid. Depending on how well they perform, they may be able to refinance their debt, pay interest, or make periodic principal payments. If they cannot produce enough cash flow from operations to pay off their current debt and any future debt, they may be forced to take one or more alternatives. These alternatives include selling assets, refinancing their debt, or raising additional equity capital on potentially onerous or dilutive terms. The capital markets and their financial situation at the time will determine their ability to refinance either their present debt or future debt. They might be unable to perform any of these tasks or provide them on favorable terms, which might lead to a default on the existing or upcoming debt.

Bottom Line

The company's share has given a multi-year breakout and looks very bullish. In addition, its sales and income have grown significantly, and I think they have great growth potential. Hence I think it can give significant returns in the long run. So I give a buy rating on HURN.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.