SCHH And VNQ: Ratings Upgraded To Buy

Summary

- This is an update to an article we published on the REIT sector about 1 year ago.

- The article uses the Schwab U.S. REIT ETF and the Vanguard Real Estate ETF to represent the REIT sector.

- This update article will upgrade our ratings on both funds from “HOLD” to “BUY”.

- The main factors that motivated the upgrade are the price corrections, improving fundamentals, and the expectation of stable interest rates ahead.

- The valuation is more attractive when the dividends are correctly interpreted by excluding the impacts from capital gains.

- This idea was discussed in more depth with members of my private investing community, Envision Early Retirement. Learn More »

Rmcarvalho/iStock via Getty Images

Thesis and Background

This is an update to an article we published on the REIT sector about 1 year ago (on July 30, 2022, to be exact). In that article, we observed a concerning red flag on our market dashboard and caution readers that:

Many safe-haven sectors such as utilities, REITs, and staples are no longer “safe”. The causes are recent market turbulence and rate hikes. Recent market corrections and rate hikes impacted different sectors differently. The REIT sector now features a negative yield spread relative to its historical averages and also risk-free interest rates.

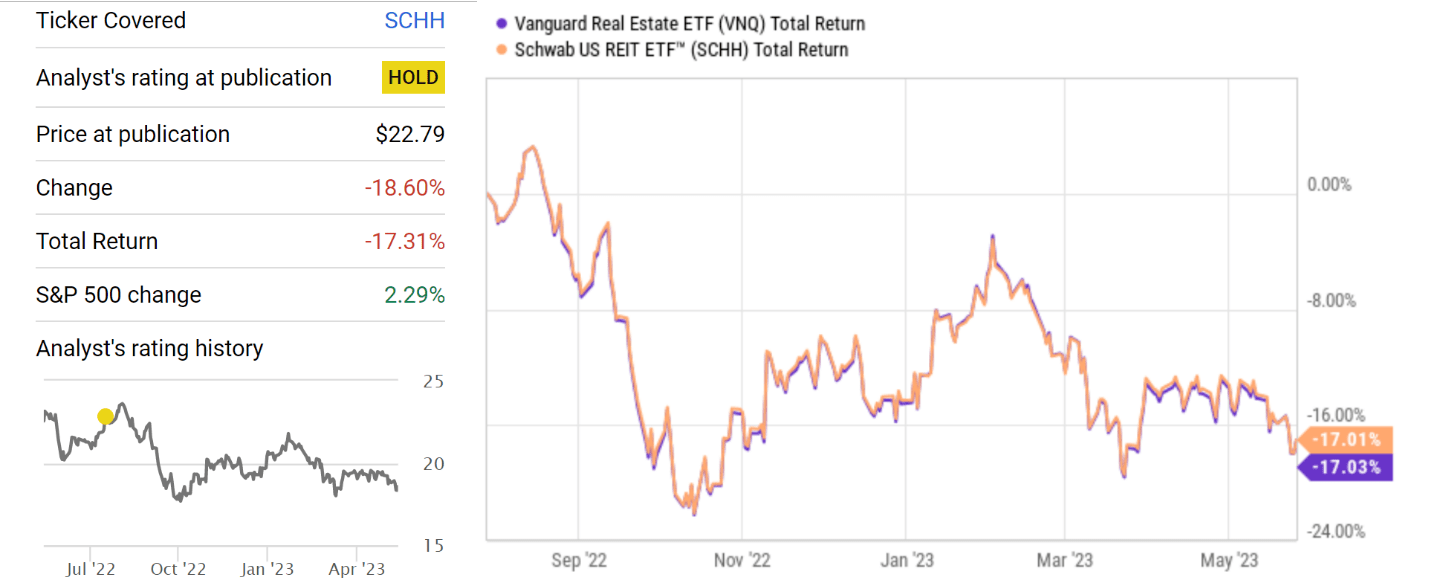

The sector indeed has suffered sizable losses since then and has lagged the broader market by a sizable margin. As seen in the chart below, the Schwab U.S. REIT ETF (NYSEARCA:SCHH) suffered a total loss of more than 17% since the publication of our original article, compared to the S&P 500’s net gain of 2.3%. Another popular REIT ETF, the Vanguard Real Estate ETF (NYSEARCA:VNQ) tracked SCHH closely and suffered the same amount of loss as seen from the right panel in the figure.

The goal of this article is to update our original article. And the thesis is to upgrade our original ratings on both funds from “HOLD” to “BUY”. And in the remainder of this article, I will detail the main factors that triggered this update/upgrade: the price corrections since then, REIT’s improved fundamentals as reflected in their dividend payouts, and the expectation of stable interest rates ahead.

Source: Seeking Alpha

SCHH and VNQ: basic information

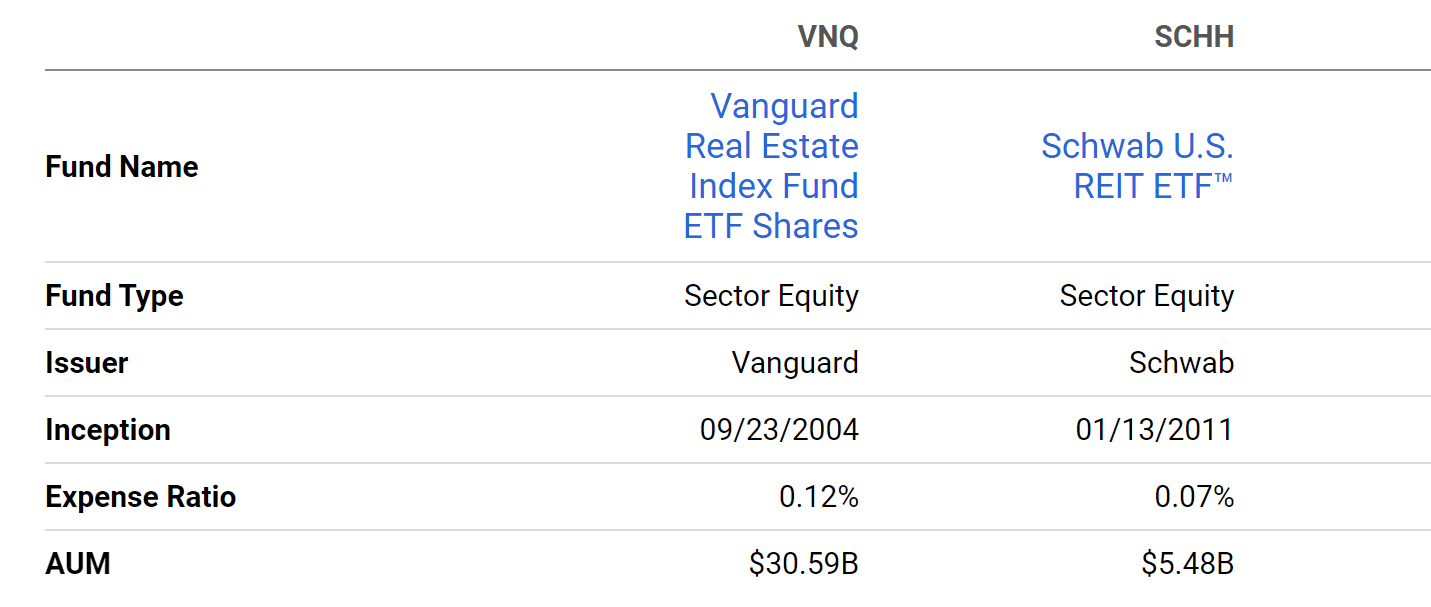

In case there are readers new to either of these ETFs, the following chart summarizes their envelop info. And their detailed indexing methods are quoted below from their web pages. VNQ has a longer history, is a larger fund ($30+ billion AUM), and offers better tradability and liquidity, although charges a higher expense ratio (0.12% compared to SCHH’0.07%). Since both funds are indexed in the U.S. REIT sector, their performance track each other closely as already shown above.

SCHH's fund description: The fund tracks as closely as possible, before fees and expenses, the total return of the Dow Jones Equity All REIT Capped Index, an index composed of U.S. real estate investment trusts classified as equities.

VNQ’s fund description: The fund closely tracks the return of the MSCI US Investable Market Real Estate 25/50 Index. The fund’s goal is to offer high potential for investment income and some growth.

Source: Seeking Alpha

Price and Dividends changes

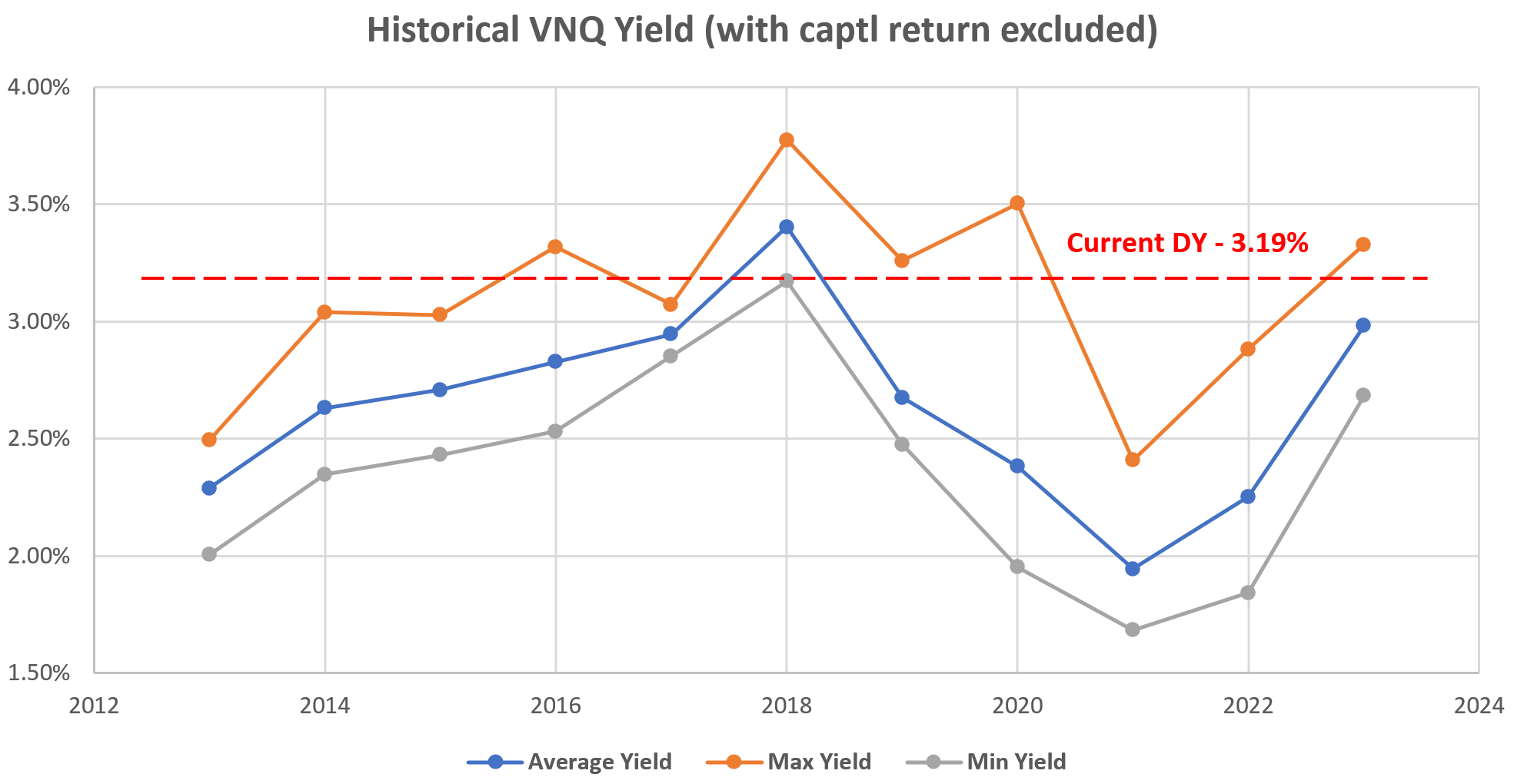

As aforementioned, two of the main factors that triggered this update/upgrade are the price corrections since July 2022 and their improved fundamentals as reflected in their dividend payouts. Due to these effects, their dividend yields are at a much more attractive level now. As seen from the chart below, their current yields are substantially above their historical averages. In the past 4 years, the average dividend yield (“DY”) is 2.61% for SCHH and 3.44% for VNQ. SCHH’s current DY of 3.11% is 19% above this average and VNQ’s current DY of 4.31% is 25 above this average, both signaling a large valuation discount.

Source: Seeking Alpha

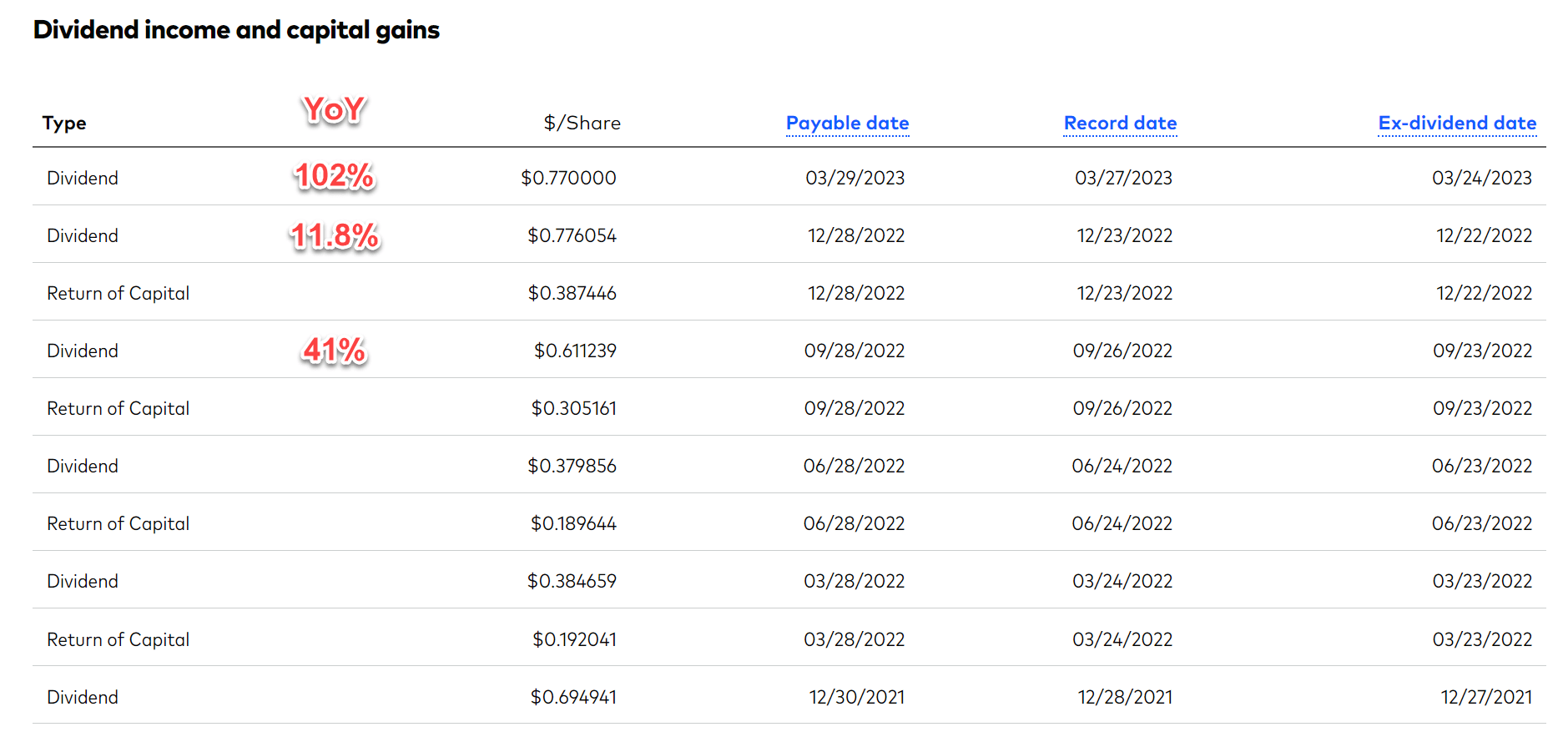

The above attractive DY was driven by both the price correction discussed early on and also more importantly, the sector’s improving fundamentals, as reflected in their dividend payouts. To wit, VNQ’s quarterly payout (excluding capital gain) since my original article has increased YOY by 41% in Sept 2022, 11.8% in Dec 2022, and a whopping 102% in Mar 2023.

Note that here we’ve excluded its return of capital from the dividends just to isolate the fundamentals. For REIT stocks, their dividends provide a good measure of their owners' earnings, but the capital gain from the fund does not. For example, VNQ’s TTM dividend excluding capital gain is $2.53 (not $3.42 as commonly quoted on most websites such as the one shown above). A good tip for you to correctly interpret REIT’s dividend data. Once the capital gain is excluded, the current DY from the REIT sector is even more attractive. Take VNQ as an example, its current “real” DY, i.e., with capital gain excluded, is 3.19%. It is of course lower than 4.31% on the surface with the capital included. But compared to its historical data (as seen in the second chart below), such a DY is near the top level in a decade.

Source: Vanguard.com

Source: author based on Vanguard.com data

Risks-free rates

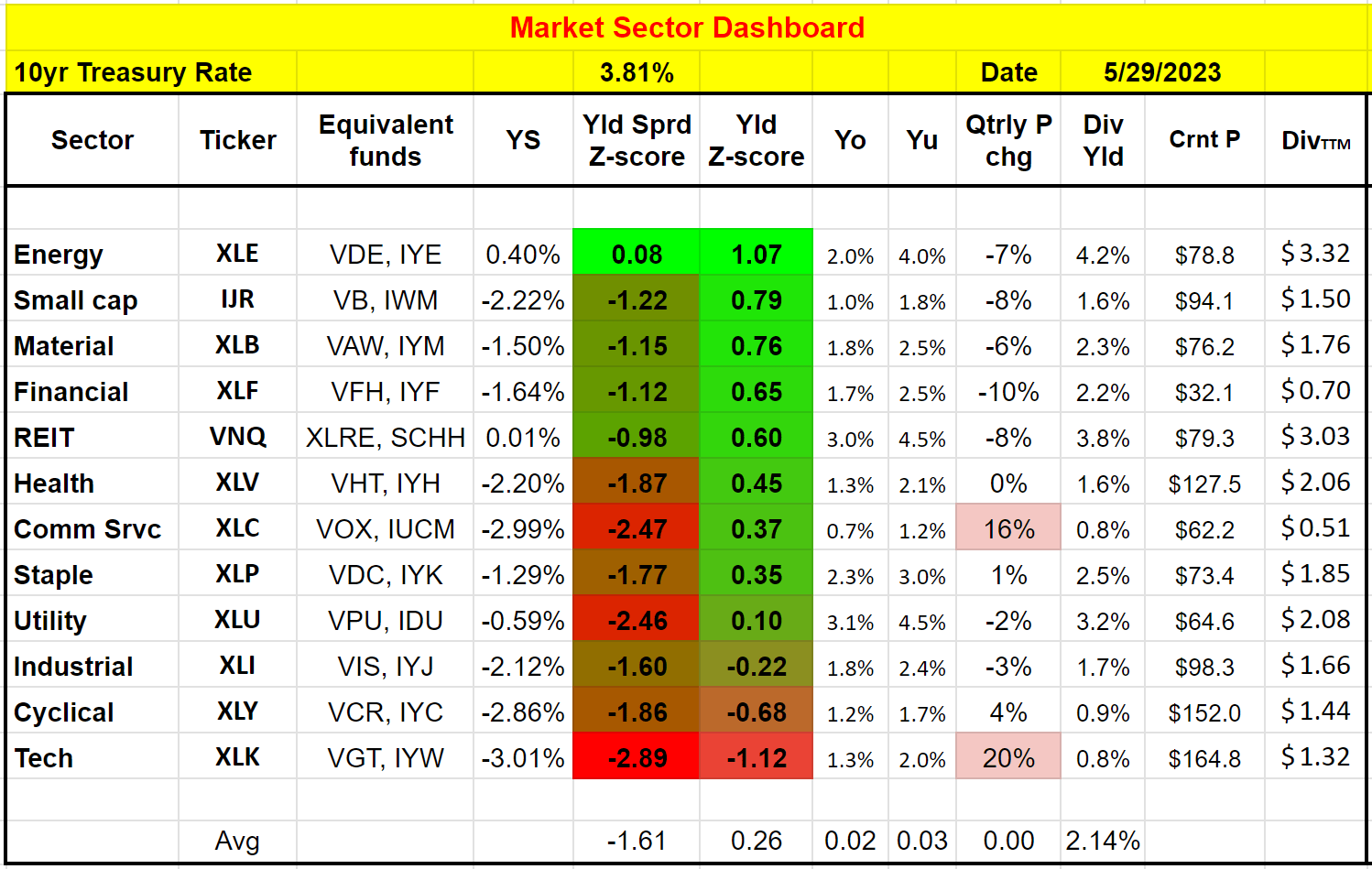

We use the following market dashboard to assess the valuation of different market sectors benchmarked against the risk-free rates. As detailed in our original article:

As top-down investors, we first check the market at a sector level to see the forest and then check a few leading stocks to see the trees. The mechanics of the market dashboard are detailed in our earlier article here and you are welcome to download it here.

The following is what our dashboard shows. As seen, the REIT sector is now in the top 5 of the most attractively valued sectors in terms of its DY. When I wrote my original article last July, it ranked as one of the least attractively valued sectors.

There is also a large improvement in the sector’s risk premium when benchmarked against risk-free rates. To wit, the sector’s yield spread relative to 10-year treasury rates is still in the negative (with a Z-score of -0.98). However, all sectors currently feature a negative YS except the energy sector as seen. And the REIT sector’s YS is the second thickest among all market sectors (again, after the energy sector only), signaling minimal risks premium relative to other market sectors.

Looking forward, I also see the probability of further rate hikes today as much lower than that back in July 2022. As such, I see the pressure from interest rates raises much released now than about 1 year ago to the sector.

Source: Author

Risks and final thoughts

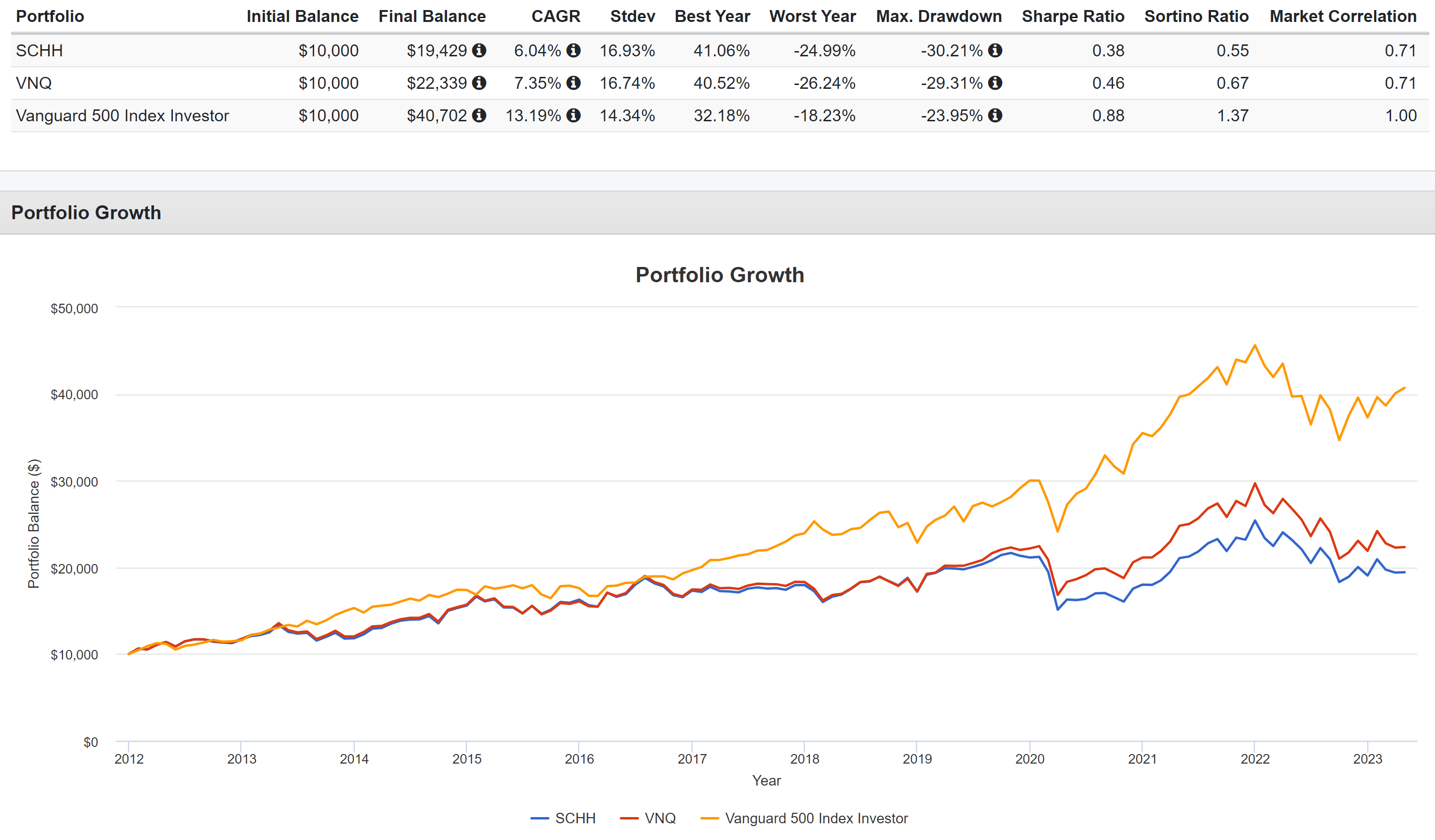

Roth funds entail several risks. First, performance risks. Both SCHH and VNQ have delivered relatively healthy returns in the past. However, both funds lagged the overall market as seen from the chart below. To wit, SCHH’s returned a total return of 6.04% CAGR and VNQ returned 7.35%, both lagging the S&P 500’s 13.2% by a good margin. Second, volatility risks. Even though REITs are widely considered a “safe haven” sector, they actually suffered substantially higher volatilities than the overall market as seen in the chart below. Measured by standard deviation, VNQ, and SCHH’s historical volatility was both on average 17%, almost 20% higher than the overall market’s 14.3%. Measured by maximum drawdowns, both VNQ and SCHH have suffered a maximum drawdown of close to 30%, about 25% worse than the overall market’s 24% since 2012.

However, REITs are indeed “safer” in the sense of their consistent dividend payouts and the hard assets behind the shares. And especially when purchased at times with attractive valuation, they also offer favorable odds for price appreciation. And the goal of this article is to argue that now is such a time. Due to the price corrections and much higher dividends since last July, both VNQ and SCHH now provide very attractive valuations. In terms of yield spread, I also see the pressure from further rate hikes much lower than 1 year ago.

Source: Portfolio Visualizer

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.

This article was written by

** Disclosure: I am associated with Sensor Unlimited.

** Master of Science, 2004, Stanford University, Stanford, CA

Department of Management Science and Engineering, with concentration in quantitative investment

** PhD, 2006, Stanford University, Stanford, CA

Department of Mechanical Engineering, with concentration in advanced and renewable energy solutions

** 15 years of investment management experiences

Since 2006, have been actively analyzing stocks and the overall market, managing various portfolios and accounts and providing investment counseling to many relatives and friends.

** Diverse background and holistic approach

Combined with Sensor Unlimited, we provide more than 3 decades of hands-on experience in high-tech R&D and consulting, housing market, credit market, and actual portfolio management. We monitor several asset classes for tactical opportunities. Examples include less-covered stocks ideas (such as our past holdings like CRUS and FL), the credit and REIT market, short-term and long-term bond trade opportunities, and gold-silver trade opportunities.

I also take a holistic view and watch out on aspects (both dangers and opportunities) often neglected – such as tax considerations (always a large chunk of return), fitness with the rest of holdings (no holding is good or bad until it is examined under the context of what we already hold), and allocation across asset classes.

Above all, like many SA readers and writers, I am a curious investor – I look forward to constantly learn, re-learn, and de-learn with this wonderful community.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.