A customer counts 2,000 rupee banknotes at a grocery store in New Delhi, India, on Tuesday, May 23, 2023. India withdrawing its highest value currency notes from circulation may push some consumers to buy precious metals and real estate, giving a temporary boost to Asia's third-largest economy. Photographer: Prakash Singh/Bloomberg

India’s rupee is set to bounce back from near an all-time low as the central bank slows its dollar purchases, according to Citigroup Inc.

The currency may rebound to as strong as 80 per dollar as easing crude prices and rising services exports also help narrow the nation’s current-account deficit, said Aditya Bagree, head of markets for India and South Asia at the bank in Mumbai.

“We are constructive on the rupee in the short term,” said Bagree, who has spent over a decade at Citibank, speaking in an interview last week in his Mumbai office. “There are almost 11 months of import cover, and hence from here, the Reserve Bank of India may slow the pace of accumulation.”

India’s currency has weakened about 0.9% this month, closing at 82.5713 per dollar last week as the prospect of higher US interest rates boosted the dollar. That put the rupee less than 1% away from its all-time low of 83.2912 set in October.

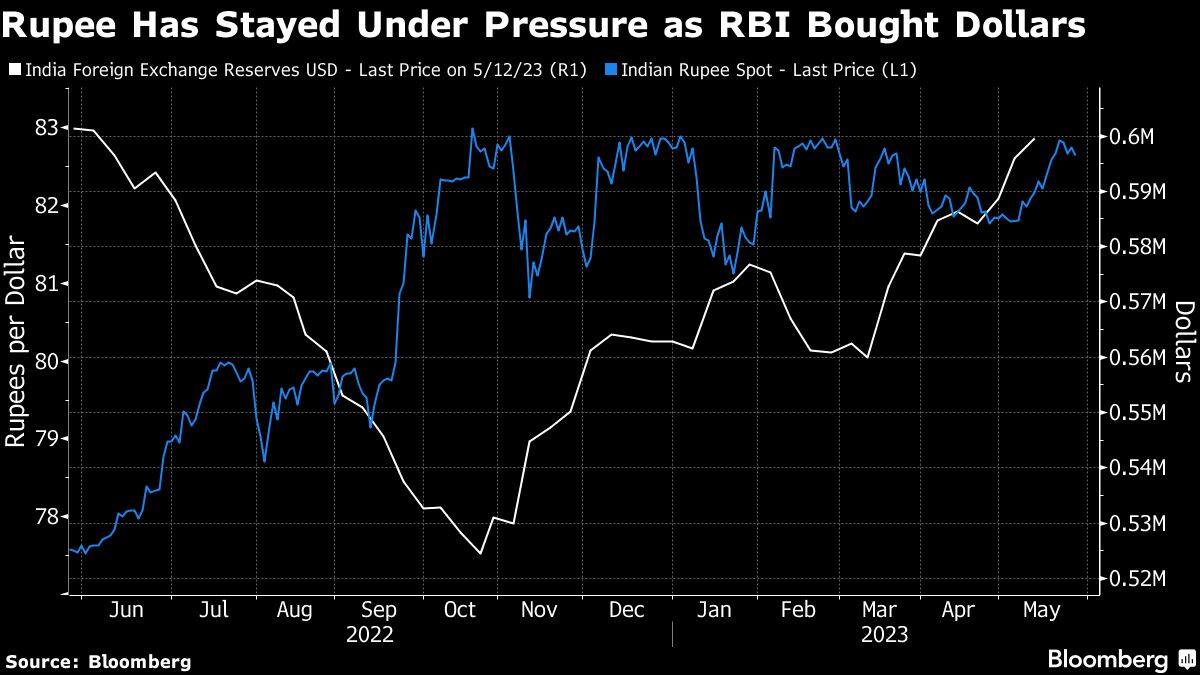

One reason that has kept the rupee under pressure has been the RBI’s steady accumulation of dollars. The central bank boosted its foreign-exchange stockpile to $600 billion by the middle of May, according to the latest central-bank data, up from a low of $525 million in October.

The rupee hasn’t been alone in weakening versus the greenback. All except two of 12 Asian currencies tracked by Bloomberg have dropped against the dollar over the past 12 months.

Shrinking Deficit

India’s current-account deficit is expected to narrow to about 1.4% of the nation’s gross domestic product in the fiscal year to March 31, Citibank’s Bagree said. That compares with an expected shortfall of 2.2% for the previous fiscal year, based on a Bloomberg survey of economists.

India’s services exports meanwhile climbed to $323 billion in the fiscal year ended March, up 27% from a year earlier, central-bank data show.