Upstart: This Optimism May Not Survive The Downturn

Summary

- Prudence has worked well for UPST, as evidenced by the moderation of its loan origination and operating expenses by the latest quarter.

- Combined with the secured $2B funding despite the recent banking meltdown, we may see the AI fintech demonstrate its proof of concept at a time of AI boom.

- These naturally led to UPST's exemplary FQ2'23 guidance, with sustained top-line growth and break-even adj. EBITDA, despite the uncertain macroeconomic outlook.

- Meanwhile, with the massive short cover, the stock has also climbed over-optimistically, suggesting an excellent time to take some gains here.

alexsl

The UPST Investment Thesis Just Got A Lot More Interesting

Upstart Holdings (NASDAQ:UPST) appears to have bottomed by FQ1'23, significantly aided by the recent banking meltdown in March 2023, with the April CPI similarly indicating a decelerating inflation trend ahead.

The fintech has also executed well during the elevated interest rate environment by tightening its loan originations to $997M by the latest quarter (-35.3% QoQ/ -78% YoY), effectively reducing its conversion rate to 8% at the same time (-3 points QoQ/ -13 YoY).

Thanks to the Fed's continuous rate hike thus far, UPST reported a drastic increase in its interest income to $38.18M in FQ1'23 as well (+9.7% QoQ/ +169.2% YoY), prior to any fair value adjustments of -$52.39M (-49.3% QoQ/ +190.7% YoY).

In addition, the fintech moderated its total operating expenses to $234.76M (+29.3% QoQ/ -14.7% YoY), with the QoQ increase only attributed to the one-time restructuring costs of $40M arising from headcount reduction and cancellation of a stock-based compensation award.

As a result, UPST's FQ1'23 operating expenses may have very well come in at approximately $195M instead (-5% QoQ/ 16.9% YoY), suggesting an impressive cost optimization after the two rounds of layoffs.

This cadence has naturally improved its contribution margin to 58% (+5 points QoQ/ +11 YoY), implying the efficacy of its AI-led lending platform at a time of peak recessionary fears.

The UPST management has strategically demonstrated the "elasticity" and performance of its platform as well, attributed to the strategic repricing of its newer loans to include the elevated default premiums, temporarily elevating the borrower's standard for creditworthiness.

Most importantly, the AI-led fintech is able to sustainably generate alpha on its tightened loans during these uncertain periods, as opposed to the higher-volume-lower-margin loans during the recent hyper-pandemic demand and steady-state economy.

In addition, UPST has guided exemplary FQ2'23 numbers, with revenues of $135M (+31.1% QoQ/ -40.8% YoY) and adj EPS of -$0.08 (+82.9% QoQ/ -900% YoY), suggesting a tremendous expansion QoQ. The projected Fed terminal rate of 5.25% may have led to its improved guidance of net interest income of approximately $5M (likely after accounting for adjustments).

Combined with the guided expansion in its revenue from platform/ referral/ servicing fees to $130M (+11.1% QoQ/ -16.4% YoY) for the next quarter, it appears that the AI-led platform boasts well-diversified top-line contributors compared to an interest rate spread only.

As a result, we believe UPST may easily achieve its optimistic guidance of adj. EBITDA break-even in FQ2'23, a feat well-celebrated by its investors, as partly evidenced by the skyrocketing share prices.

This is on top of the fintech's expanded funding agreements of over $2B through the next twelve months. This is an impressive vote of confidence in our opinion, since most banks have tightened their lending standards after the recent banking meltdown.

This optimistic development may then allow UPST to sustainably grow its loan originations while maintaining peak loans held on the balance sheet at approximately $1B, compared to the current $0.98B reported in FQ1'23 (-2.9% QoQ/ +63.3% YoY).

So, Is UPST Stock A Buy, Sell, or Hold?

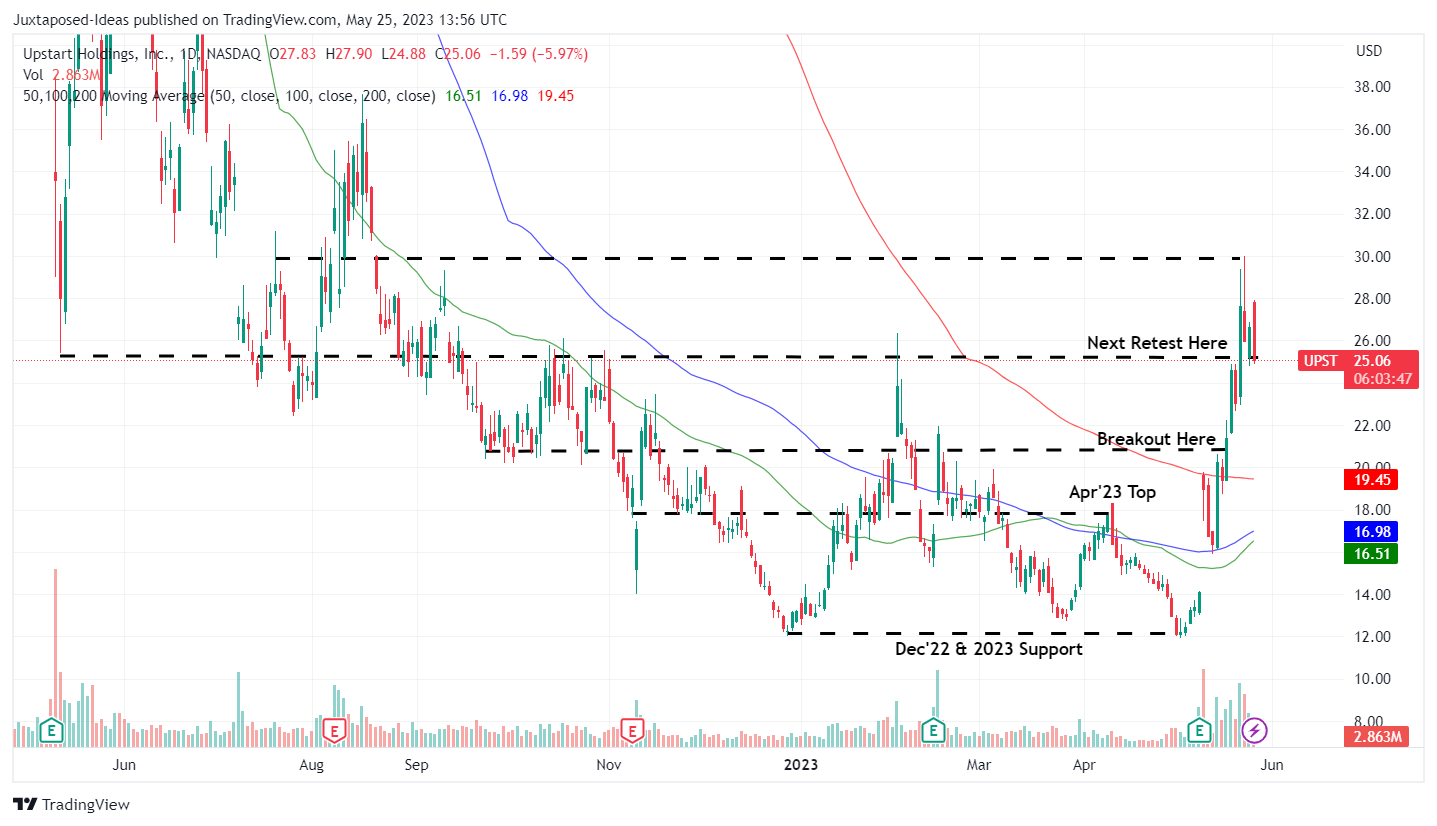

UPST 1Y Stock Price

Trading View

Then again, the high short interest has also tremendously driven up UPST post-earnings call, with the stock already recording an +79.7% rally at the time of writing. We do not expect these optimistic levels to hold in the intermediate term, with the stock likely to recalibrate to the April 2023 top of $17s.

Therefore, while we continue to rate the stock as a Hold for long-term investors, traders may consider taking some gains off the table here. There is no harm in doing so, since the economic downturn may only lift by 2024, if not 2025, triggering further downward pressure on its stock prices.

Meanwhile, we are turning cautiously confident about UPST's execution in the long term, as evidenced by the optimistic developments thus far. For so long that it maintains a steady pool of funding partners, loan originations may remain decent through the next few quarters, before taking off once the market sentiments lift and the Fed pivots.

For now, UPST has convinced us of its growing moat in the lending market, one that naturally expands its market share, based on the ambitious Total Addressable Market of up to $4T in annual loan originations across Personal, Auto, Home, and Small Business end markets. Considering that the management has had to navigate an overwhelmingly challenging three and a half years, the execution thus far has been more than commendable indeed.

Therefore, we may consider adding the stock over the next few quarters, though sized appropriately due to its volatility and the fintech's lack of GAAP profitability thus far. For now, we prefer to wait and see.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The analysis is provided exclusively for informational purposes and should not be considered professional investment advice. Before investing, please conduct personal in-depth research and utmost due diligence, as there are many risks associated with the trade, including capital loss.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.