FedEx Corporation is a dominant player in the global logistics and transportation industry.

E-commerce boom and global expansion fuel FedEx's growth.

Technological innovations drive operational efficiency and customer experience.

FedEx's sustainability initiatives align with the growing focus on environmental responsibility.

Strong financial performance and resilience are expected to continue. Based on my assumptions outlined below, FedEx stock's intrinsic value is $253 and is currently trading at $224, representing a 13% upside opportunity.

Joe Raedle

Background on FedEx:FedEx Corporation (NYSE: FDX) is a leading multinational courier delivery services company headquartered in the United States. FedEx's history spans several decades and the company has established itself as a dominant player in the global logistics and transportation industry. The company's strong market position, innovative solutions, and expanding e-commerce sector present a compelling investment opportunity. FedEx has kept up with technological innovations, continued to expand globally, and is a beneficiary of the E-Commerce boom.

Based on my assumptions which I will outline below, FedEx Corporation stock is currently 13% undervalued, with my discounted cash flow ("DCF") model suggesting a fair value of $253 for the stock.

Firstly, I will outline some of the key factors that are/have been driving FedEx's growth.

FedEx Growth Drivers

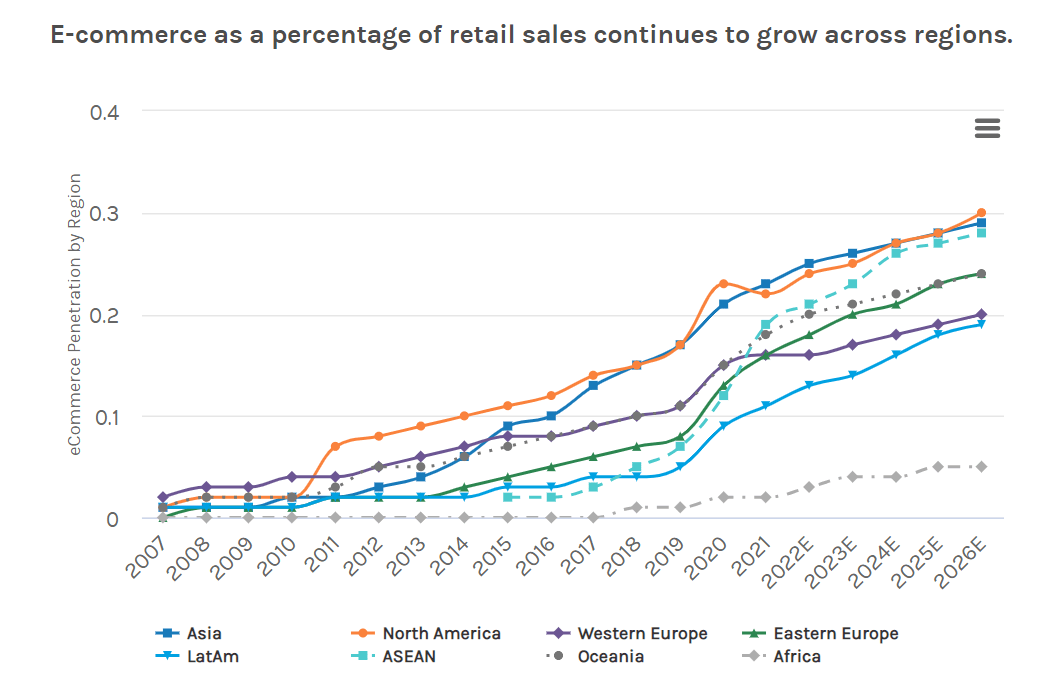

E-commerce Boom: The rapid growth of e-commerce has transformed the logistics landscape, creating a significant demand for efficient and timely delivery services. FedEx has successfully adapted to this changing landscape by investing in advanced technology and expanding its infrastructure to handle the surge in online shopping. The company's integrated network, comprising air, ground, and sea transportation, enables it to provide end-to-end solutions and cater to the evolving needs of e-commerce businesses.

Euromonitor, National Data Sources, Morgan Stanley Research estimates

Global Expansion: FedEx has a strong international presence, allowing it to capture opportunities in both developed and emerging markets. With the globalization of trade, the company's extensive network and strategic partnerships provide a competitive edge. As cross-border e-commerce continues to grow, FedEx's global reach positions it to benefit from the increasing demand for efficient international shipping and customs clearance services.

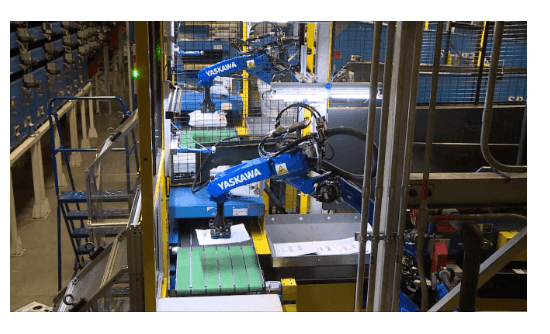

Technological Innovations: FedEx has consistently embraced technological advancements to enhance its operational efficiency and customer experience. The company has invested in automation, robotics, artificial intelligence, and data analytics to optimize its supply chain and delivery processes. The image below comes directly from FedEx's website along with commentary explaining the company's policy on AI and automation:

At FedEx, we see automation as an opportunity to enhance our team members’ jobs within our system, make them more comfortable and easy, and above all, as safe as possible. We’ve progressed our work with robots and automation, and will continue to do so moving forward. FedEx Ground has recently undergone a transformation, investing in highly-advanced technology and innovations that have resulted in one of the most automated networks in the industry. They continue to test a number of new and emerging technologies within their operations to help maintain this position.

FedEx Website

The innovation journey FedEx is embarking on includes faster order processing, route optimization, real-time tracking, and improved customer communication. By leveraging these technologies, FedEx can deliver superior service and gain a competitive advantage within the industry.

Sustainable Practices: FedEx has demonstrated a strong commitment to sustainability and environmental responsibility. The company aims to achieve carbon-neutral operations by 2040 through various initiatives, including investing in electric vehicles, adopting renewable energy sources, and implementing efficient packaging solutions. As the global focus on sustainability intensifies, FedEx's proactive approach positions it as a preferred partner for environmentally conscious businesses.

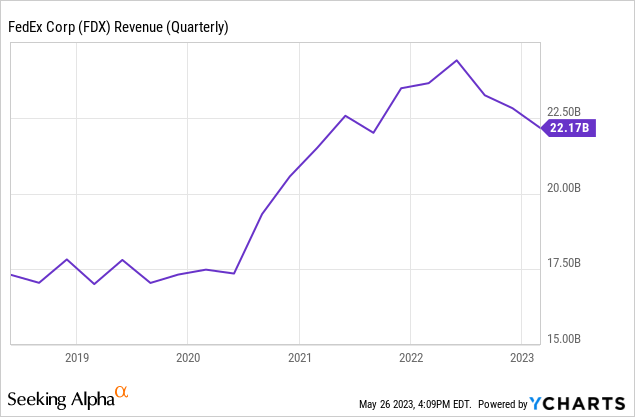

Strong Financial Performance: FedEx has consistently delivered strong financial results, reflecting its ability to generate sustainable revenue growth and profitability. Despite the challenges posed by the COVID-19 pandemic, the company demonstrated resilience and adaptability by quickly adjusting its operations to meet changing customer demands.

As you can see, despite the recent blip in revenue growth, the company has managed to grow quarterly revenue from 17.5B in 2020 to 22.17B as of its most recent quarter.

Forecasts

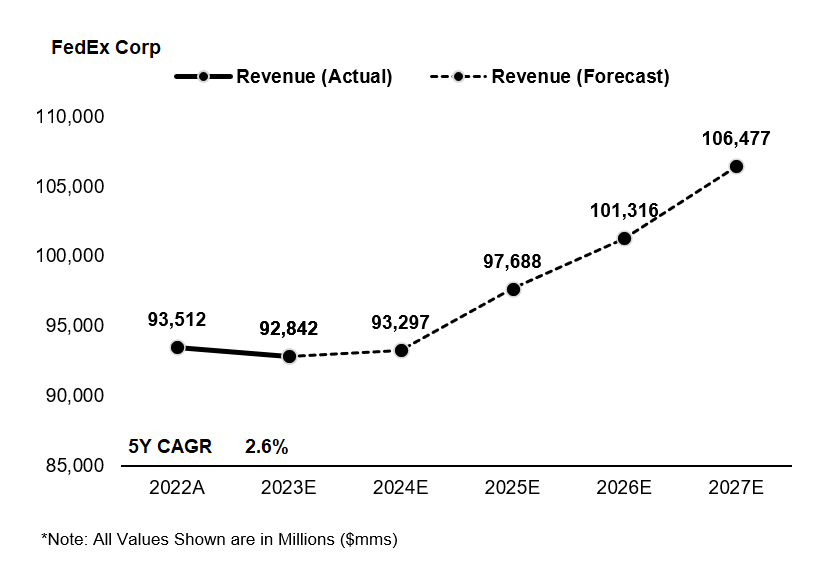

My revenue forecast for FedEx hinge on its continued dominance within the global logistics industry and continued capitalization on e-commerce trends. I forecast a 2.6% CAGR for FedEx's revenue over the next five years.

The Black Sheep, Company Filings

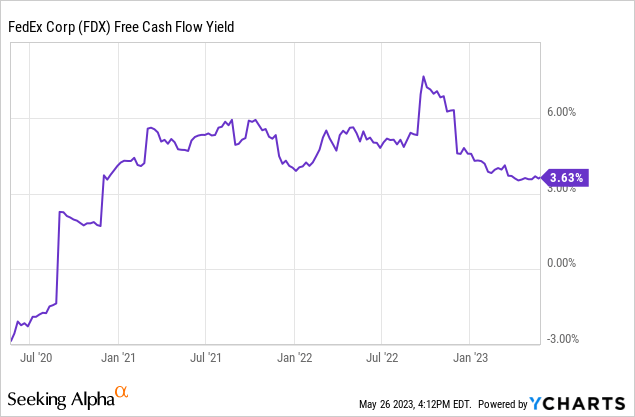

I expect this revenue to translate to free cash flow as well, especially considering the company's historical track record at maintaining a free cash flow yield around 3-5%.

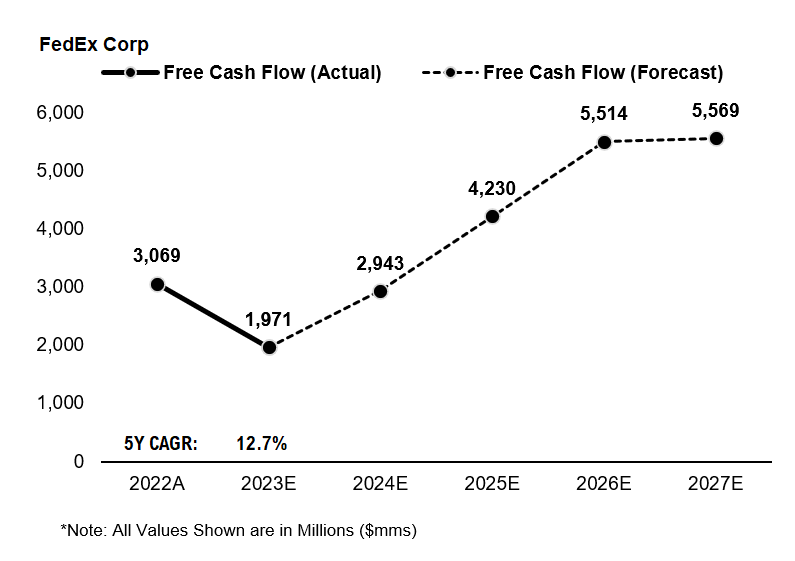

My forecast for free cash flow is charted below. I see free cash flow taking a slight hit in 2023, but rebounding sharply by 2027.

The Black Sheep, Company Filings

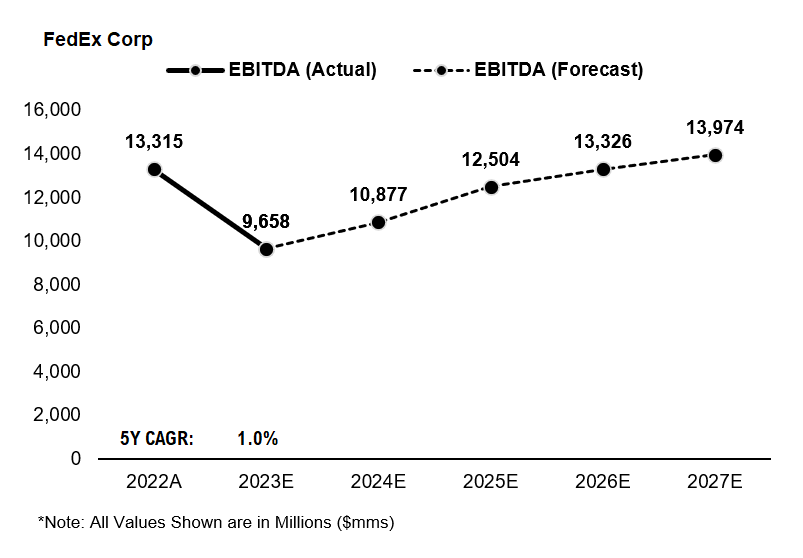

I believe FedEx will grow EBITDA over the next 5 years (through 2027), albeit at a slower pace. The conservative estimate shown for EBITDA is reflective of my concern that prices of materials and labor may increase due to lingering inflationary impacts.

The Black Sheep, Company Filings

Valuation:

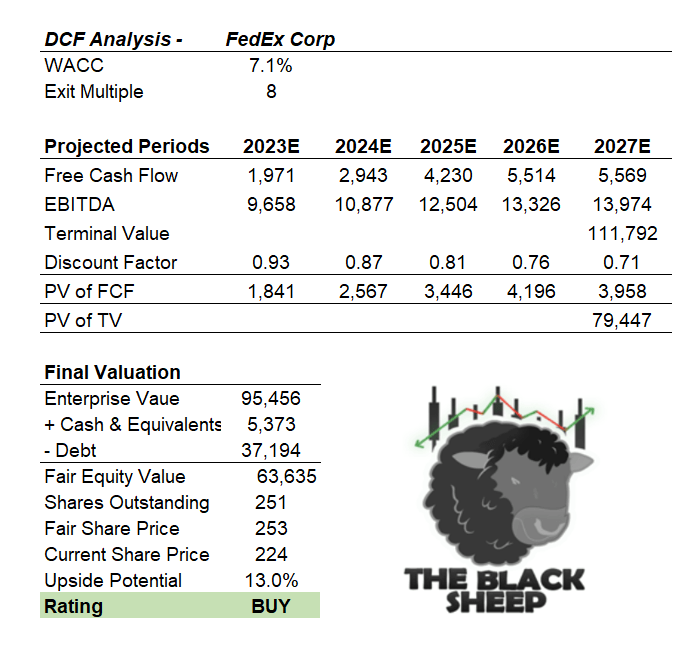

Below is my DCF model, which reflects all of the assumptions I've outlined above. I also assume a WACC of 7.1% and exit multiple of 8x (conservative given industry average is 8.3x).

The Black Sheep, Company Filings

Given these estimates, my model suggests 13% further upside for FedEx, as the company benefits from continued growth, profitability, and capitalizes on emerging E-commerce trends.

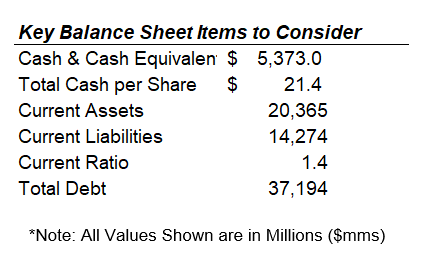

Financial Position/Balance Sheet

Take a look at some of the key balance sheet items for FedEx below.

The Black Sheep, Company Filings

The main takeaway for me is that the company has a current ratio >1 which means it has the ability to service its short-term liabilities and cash per share of $21.4. This large cash position is a strong sign that the company is prepared for any sort of cyclical downturn in the economy and will be able to weather an impending recessionary storm.

Potential Risks to Consider

Competitive Landscape: The logistics industry is highly competitive, with several major players vying for market share. FedEx faces competition from established competitors like United Parcel Service, Inc. (UPS) and Amazon.com, Inc. (AMZN), as well as emerging startups disrupting the industry with innovative solutions. To maintain its position, FedEx must continue to invest in technology, expand its service portfolio, and differentiate itself through superior customer service.

Global Economic Factors: FedEx's performance is closely tied to macroeconomic conditions and global trade patterns and many are calling for recession in 2023. While I do believe the concerns are overblown on recession (I will not get into now, but it is definitely an assumption in my outlook here that we will have a soft landing), it is still something to keep an eye on.

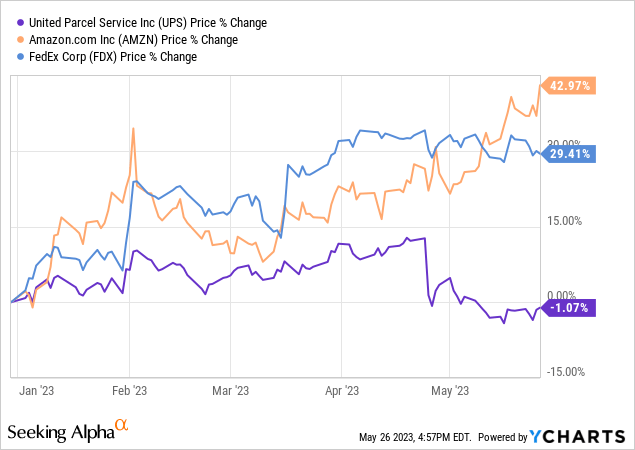

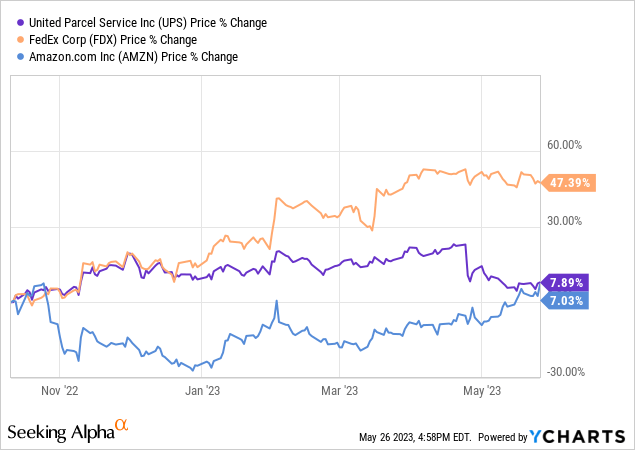

Price Performance

Below is a price chart of FedEx and these competitors.

While Amazon has had a blowout year in terms of price performance, if we zoom out and take a look since the October 2022 S&P 500 Index (SP500) low, FedEx is actually outperforming its competitors nearly 7X

FedEx Corporation stock is a compelling investment opportunity in the evolving global logistics industry. The company's strong market position, global network, technological innovations, and commitment to sustainability position it for long-term growth. Based on my assumptions, I believe FedEx Corporation stock is a buy at current levels and assign a fair share price of $253, representing 13% further upside for the stock.

Avid investor. Extensive experience in valuation and financial modeling. Previously conducted single stock research for a fund manager with >$170M of single stock holdings, often employing contrarian strategies to increase returns.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.