Build-A-Bear Workshop Q1 Earnings: Thriving With Emotional Customer Connection

Summary

- Mixed report, as Build-A-Bear Workshop, Inc. Q1 2023 results showed modest revenue growth.

- The potential is there for continued revenue growth above inflation in coming years, driven by the rollout of new experience locations.

- Build-A-Bear Workshop's capital allocation includes share repurchases and the potential for special dividends in the future, highlighting the company's value and its cash flow generative nature.

- Build-A-Bear Workshop, Inc. stock is priced around 4x to 5x this year's operating earnings.

- I do much more than just articles at Deep Value Returns: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Adam Bettcher

Investment Thesis

Build-A-Bear Workshop, Inc. (NYSE:BBW) delivered a mixed Q1 report. The negative aspect was that fiscal Q1 2023 reported modest revenue growth.

That being said, I believe that BBW's revenue could continue growing above inflation over the next few years. This is particularly true given its expectation of rolling out up to 30 new experiences locations in the second half of fiscal 2023.

The business has a clean balance sheet and its capital allocation strategy includes share repurchases and the potential for special dividends in the future.

Why Build-A-Bear Workshop? Why Now?

Build-A-Bear Workshop, Inc. has built its success by establishing an emotional connection with its customers.

However, the challenging macro environment has led to price sensitivity among consumers. The shift towards online shopping and reduced foot traffic in malls has further added to the perception of BBW's struggles.

To overcome these challenges, BBW has adopted a digital strategy and focused on securing prime retail locations.

By expanding its digital marketing capabilities, BBW aims to reach a broader consumer base, including teens and adults, who now represent approximately 40% of its end users. BBW's customer base consists of individuals with strong spending power, emphasizing their willingness to pay for an experiential shopping experience.

As BBW's CEO Sharon Price John said,

Over the past quarter century, the Build-A-Bear brand has created a deep emotional bond with our cherished guests, transcending age barriers and extending our reach from children to teenagers and adults alike.

In essence, this is my core argument, BBW does not have a moat. However, it does have tremendous value. BBW creates an emotional bond with guests spanning different age groups. Therein lies the value of this investment thesis and why the stock is less cyclical than many investors realize.

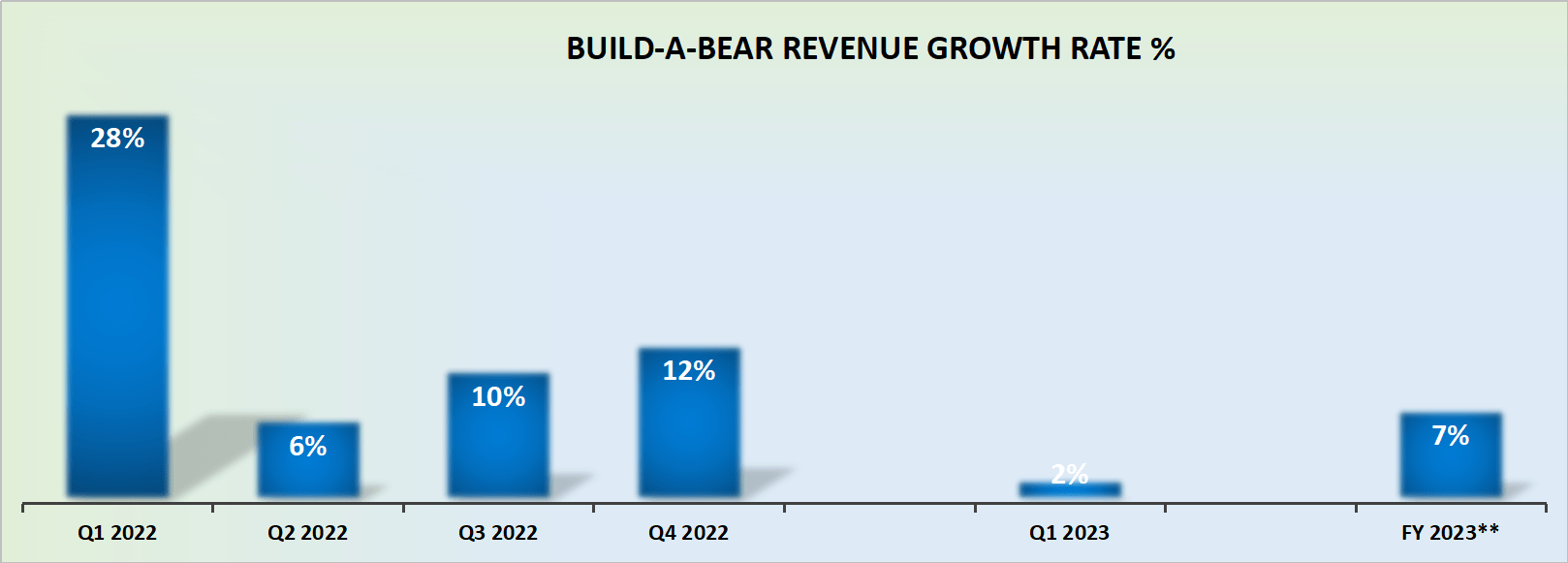

Revenue Growth Rates Continue Ticking Along

BBW revenue growth rates

I won't make the argument that fiscal Q1 2023 was particularly strong. It clearly was not, at 2% y/y growth. That being said, consider the strength of last year's fiscal Q1.

That was always going to be a challenging comparable. In actuality, the investment thesis is that BBW's revenue is growing above inflation and is likely to continue growing at higher than inflation, at least over the next couple of years.

Capital Allocation Strategy Discussed

Build-A-Bear Workshop, Inc. gave a special dividend last quarter and many investors would have probably hoped to see another one on the cards. But that didn't happen.

What did happen is that BBW repurchased a small number of shares. While I won't claim that these share repurchases will move the needle on the bull case, I do believe that they are ''yet another reason'' to consider BBW.

Furthermore, BBW is guiding for around $70 million of operating earnings. This puts the stock priced at somewhere between 4x to 5x operating earnings.

So, to summarize, we have a cheaply valued business, that has excess cash after seeking to open up to 30 experience locations in the second half of this fiscal year, that's clearly highly cash flow generative, being priced at around 4x to 5x operating earnings.

What's more, Build-A-Bear Workshop, Inc. holds more than $20 million of net cash on its balance sheet. This means that after BBW has rolled out and integrated these new shops, perhaps in fiscal 2024, yet another special dividend could be declared.

The Bottom Line

The headline summary is this: Build-A-Bear Workshop, Inc. is really very cheap, to the point that investors would do well to seriously consider it.

The more nuanced summary notes that BBW has established an emotional connection with customers. However, the company faces challenges in a price-sensitive macro environment and shifting consumer behavior towards online shopping.

Ultimately, I believe that at 4x to 5x this year's operating earnings, Build-A-Bear Workshop, Inc. investors are not paying for a story stock. Yes, there's always the concern that retail could be affected by a potential recession. However, I make the case that Build-A-Bear Workshop, Inc. is more recession-resistant than many investors believe.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.

This article was written by

DEEP VALUE RETURNS: The only Marketplace with real performance. No gimmicks. I provide a hand-holding service. Plus regular stock updates.

We are all working together to compound returns.

WARNING: Any stocks that you feel like buying after discussions with me are your responsibility.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.