XPeng: Fierce Competition And Macro Headwinds Pose Risks

Summary

- XPeng appears to be under fire in its current price range from both competitors Tesla and BYD, which are currently waging a price war.

- The company's revenue fell significantly in the first quarter and in recent quarters, while margins also came under severe pressure.

- Macroeconomic data also indicate that the Chinese "reopening boom" is much weaker than expected, indicating a tougher environment for consumers and producers.

- We believe XPeng's intrinsic value is lower than at which it is currently trading, while we believe there are still huge opportunities in other Chinese equities.

Robert Way

Investment Thesis

Chinese automaker XPeng (NYSE:XPEV) just announced its earnings results, which were light across the board for both revenues and earnings, while it also announced a weak second quarter with deliveries expected to fall 36.1% to 39.0% year-on-year.

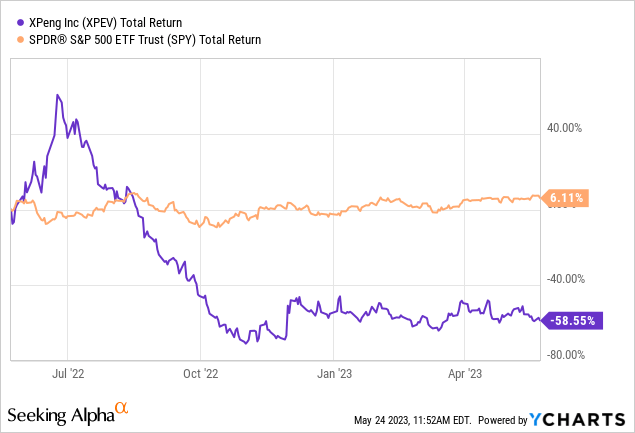

Although XPEV stock has already fallen significantly, we think it is poised to reach lower levels as tough competition from larger competitors BYD (OTCPK:BYDDF) and Tesla (TSLA) will continue, while China faces very difficult macroeconomic times. We downgrade XPeng's rating from "Buy" to "Sell" as we also believe there are much better Chinese equities, in deep value territory, to gain exposure to Chinese innovation.

Demand Concerns

Certain figures released during the first quarter and the last quarters make us wonder if XPeng was mainly suffering from a demand problem, rather than the Chinese economy that was locked down for much of last year and 2021.

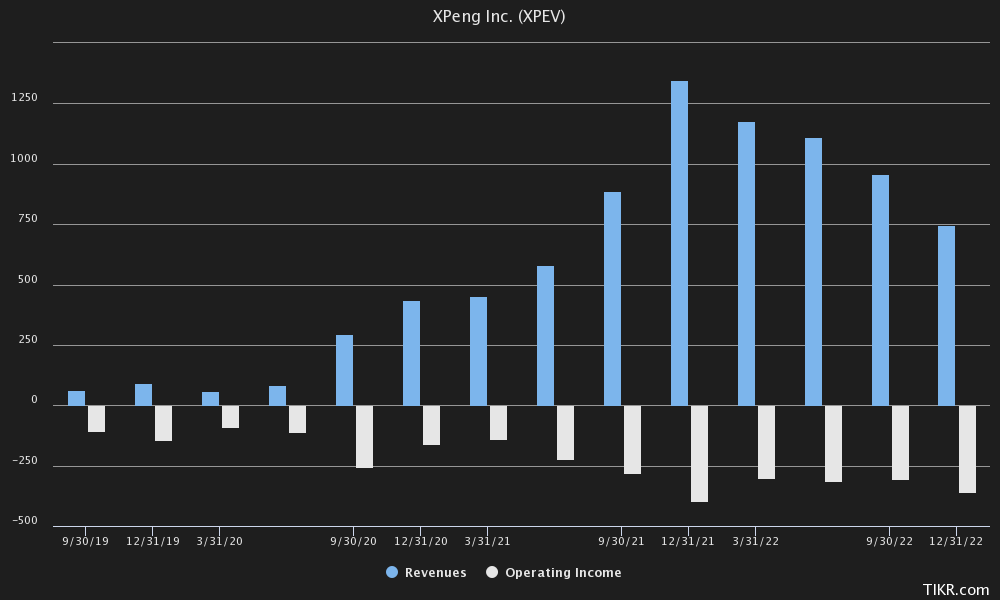

Revenues came in much lower than expected, at $587.31 million versus the expected $712.67 million, causing revenues to fall even further and now stand at -45.9% year-on-year, despite a rebounding economy. Automotive gross margins turned negative for the first time since the second quarter of 2020. In terms of operating income, the company also seems to continue to bleed money, with -$376.46M for the first quarter.

TIKR Terminal

One of the reasons XPeng experienced a weaker-than-usual Q1 than Q4 may be the expiration of some subsidiaries that expired at the end of the year in 2022, thus boosting year-end sales in Q4. Nevertheless, a 10% purchase tax exemption reportedly still runs through the end of 2023, which could further hurt sales when it expires at the end of the year.

We think the main problem for XPeng's demand problems is the environment in which the company operates, where it is in the same price range as Tesla and BYD, which are also currently facing cutthroat competition and drastically lowered their prices earlier this year to meet demand.

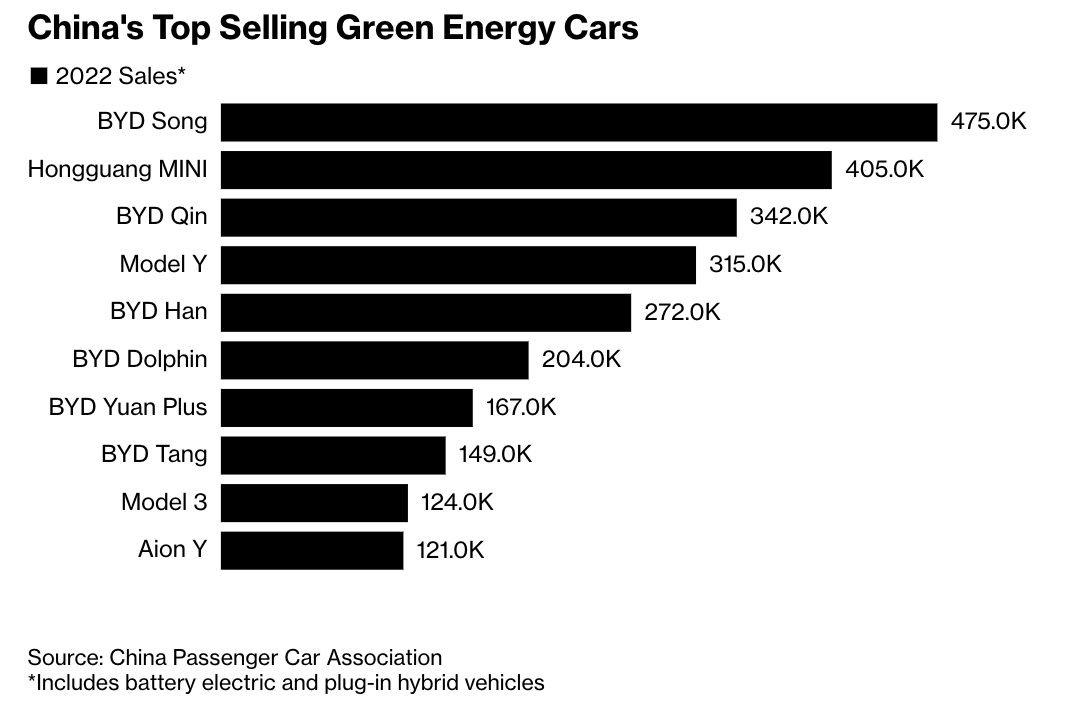

Bloomberg

XPeng's vehicles are priced around 150,000 to 300,000 RMB, which is in the same price range as mass-market vehicles such as BYD, which expects 3 million sales in 2023, and Tesla, which made 710,000 sales in 2022. This is in stark contrast to BYD's 120,757 sales in 2022.

But back to the price range of RMB 150,000 to RMB 300,000, XPeng's vehicles are currently priced very similarly to its competitors. A Tesla Model 3 currently starts at RMB 231,900 and a Model Y at RMB 311,900. And that's for premium-priced vehicles, which are still seen as luxury items, even in the United States. Compared to BYD's more affordable options, XPeng has it even more up against BYD, which recently began delivering its Seagull EVs starting at a staggering RMB 73,800.

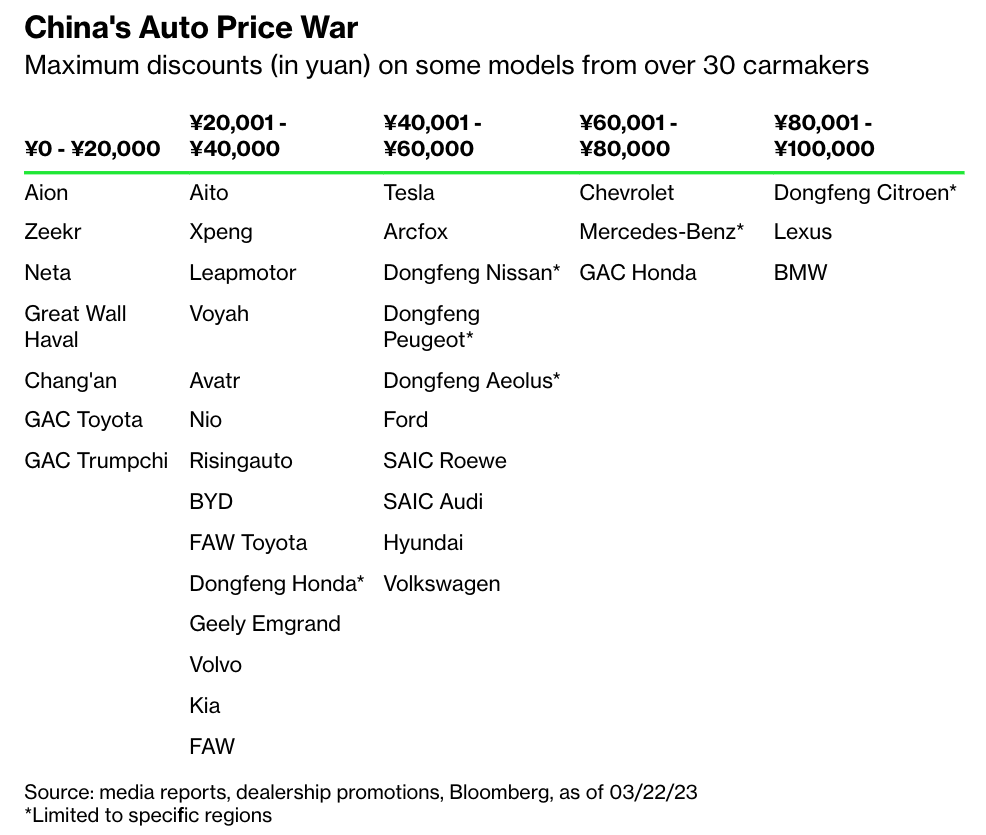

While BYD and Tesla are already igniting a price war, this comes as a blow to XPeng, which is not even profitable yet and needs to lower its prices even further and face even greater cash flow drain to meet demand and scale up production.

Bloomberg

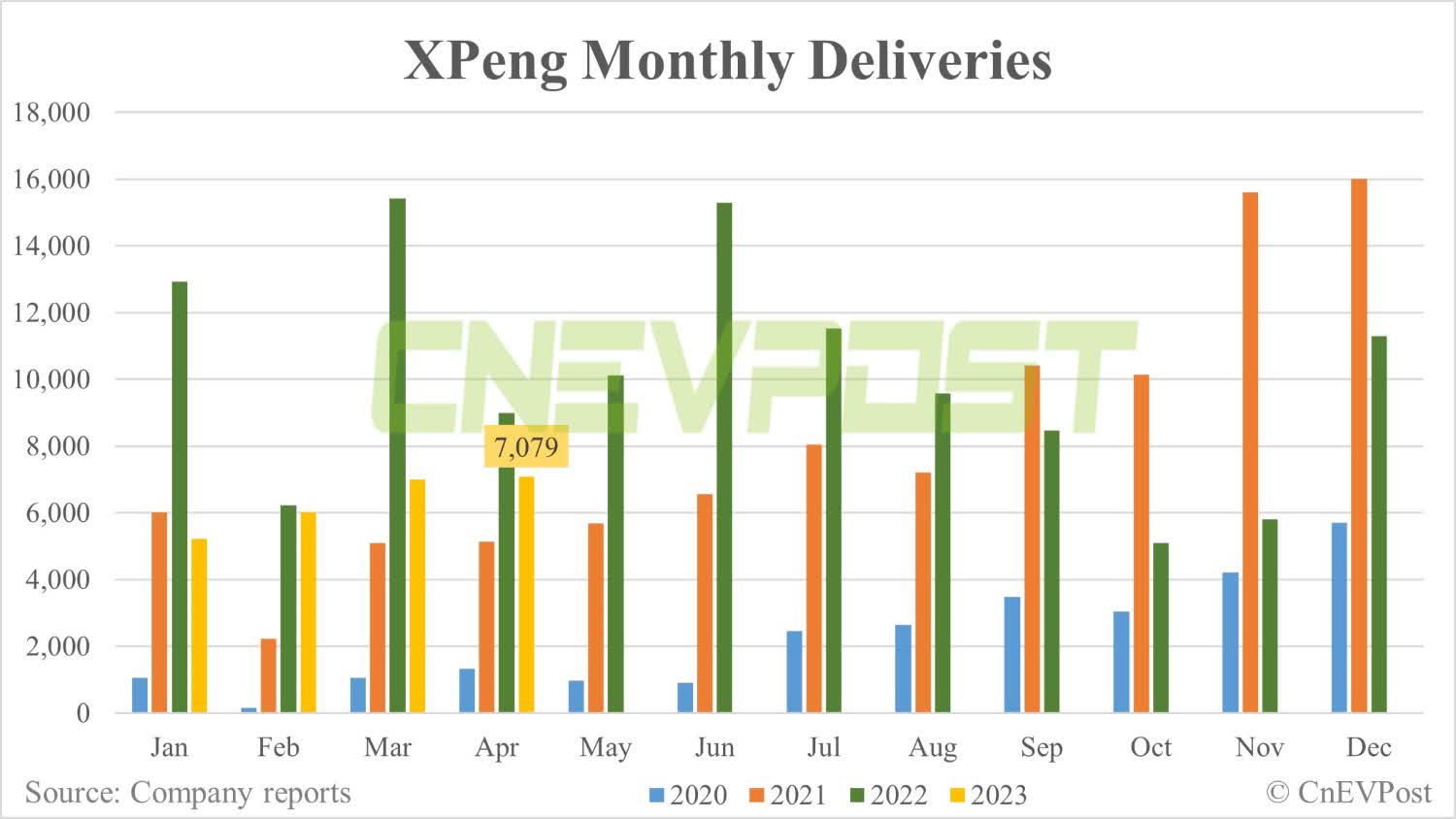

Deliveries are only expected to come in between 21,000 and 22,000, meaning that deliveries in the coming months are likely to remain flat from the approximately 7,000 deliveries in April. This is much lower than deliveries in 2022, and not far from deliveries in 2021 and by the end of 2020.

CnEVPost

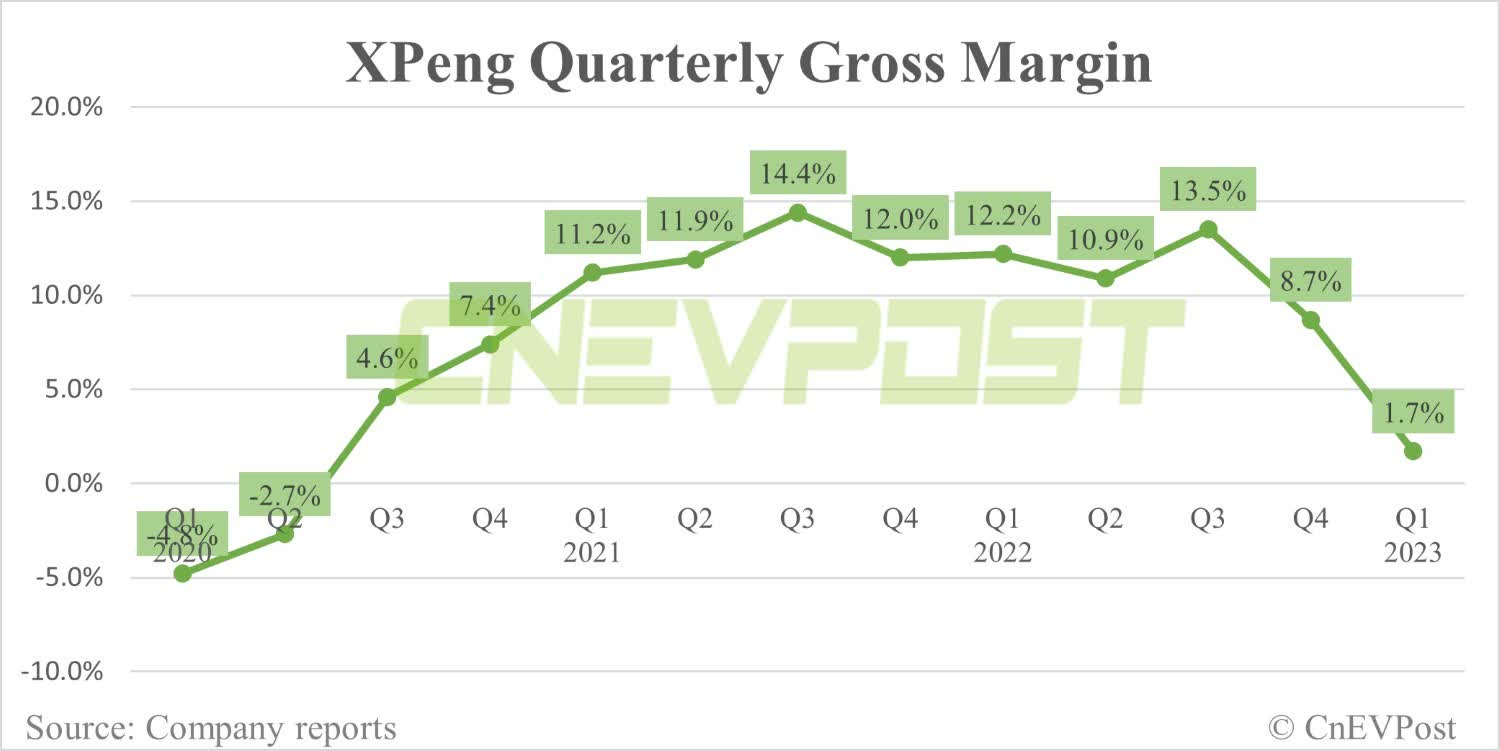

But even leaving deliveries aside, these macroeconomic pressures, which we will talk about in a moment, combined with expiring EV credits and a price war between BYD and Tesla have also apparently erased XPeng's gross margins, which currently stand at just 1.7%. These are the worst margins since 2020, and it means XPeng only grossed $9.76 million in the first quarter, not even speaking about the $390.60 million in OpEx.

CnEVPost

On its balance sheet, XPeng has US$4.97 billion in cash and short-term investments, which can be seen as a large buffer to further downward pressure on the stock. Contrast this with the current operating loss of $376.46 million, XPeng has just over 13 quarters of runway left.

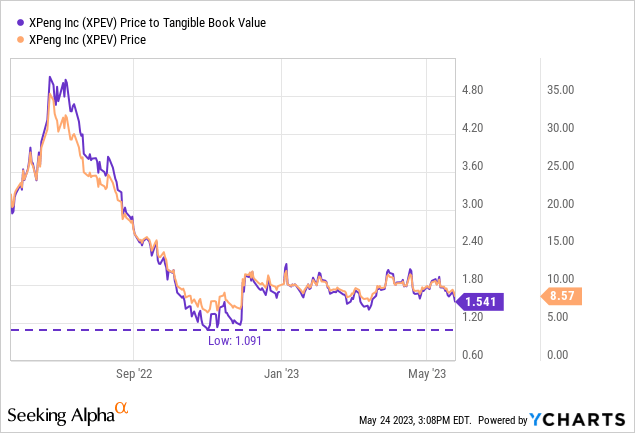

However, if we look at the tangible book value, this might provide some protection against downside risk: in the fourth quarter, the tangible book value per share was $5.58, not far from the $8.55 we are trading at now. We think this could mean a bottom around $5-6 for XPeng, or close to the previous lows around $6 for a better entry point.

Since XPeng is not yet profitable, nor has it produced a positive figure at the operating income level, we will mainly look at the aforementioned Price/Tangible Book Value and P/S multiples.

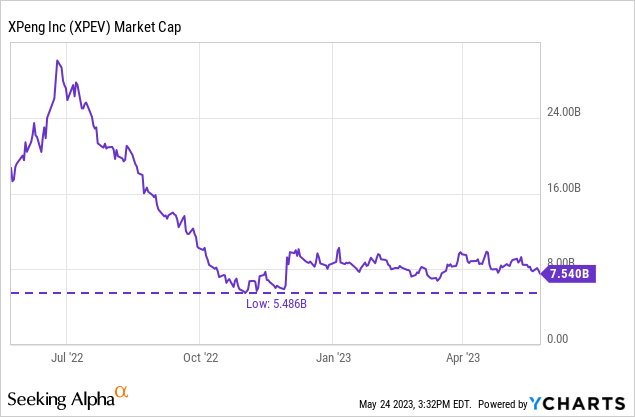

For example, if we look at BYD, one of XPeng's rivals, as they also currently sell almost all Chinese EVs/PHEVs, it has RMB 468.13 billion in revenue on a TTM basis. The stock is currently trading at RMB 723.42BN, meaning it has a P/S ratio of 1.54x. At the same P/S ratio, XPeng would trade at $5.25BN on a TTM basis with revenues of $3.40BN, which is much lower than the $7.54BN it is currently trading for. And that figure seems rather generous to us, given that BYD is currently producing significant positive free cash flow, along with 17.7% gross margins as of the first quarter.

Therefore, we think the fair value for XPeng is closer to its previous lows, around $6, or a market capitalization closer to $5.25BN.

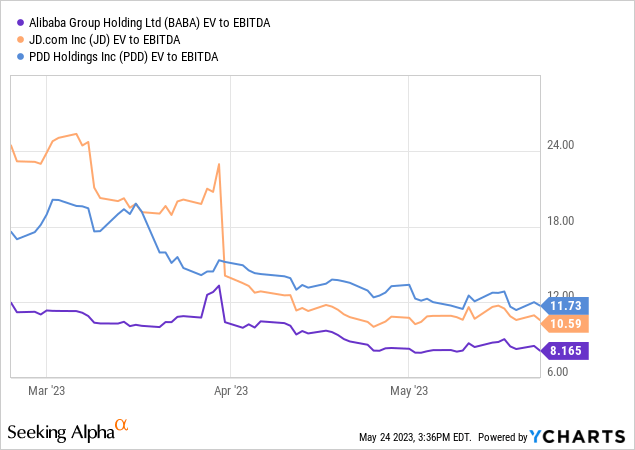

Even if we compare it to other companies in which investors can invest to gain exposure to China and Chinese innovation, we believe there are much greater opportunities. Currently, companies like Alibaba (BABA), JD.com (JD) and Pinduoduo (PDD), which we wrote about recently, are arguably in "deep value" territory compared to XPeng, which is currently burning cash hand over fist and seeing its revenues decline.

Tough Macroeconomics

Even on a macroeconomic basis, we think XPeng is facing significant headwinds, which will further hurt its demand problems, profitability issues and declining growth.

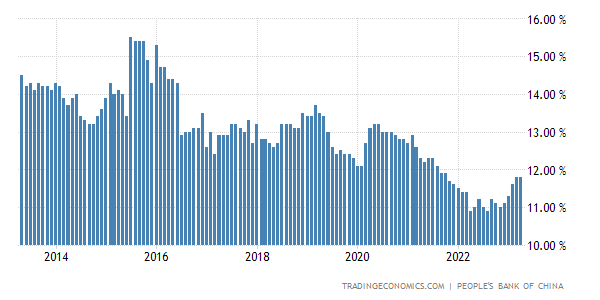

Many expected the Chinese economy to rebound, following the reopening after more than 2 years of lower growth, as the economy was locked down. However, recent data show that this optimism may have been misplaced. If we look at the growth rate of Yuan Loans, which is very important for a growing economy, we see that it is currently around 11.8%, which at first glance seems like a lot. But it is actually almost the lowest rate in the past 20 years.

Trading Economics

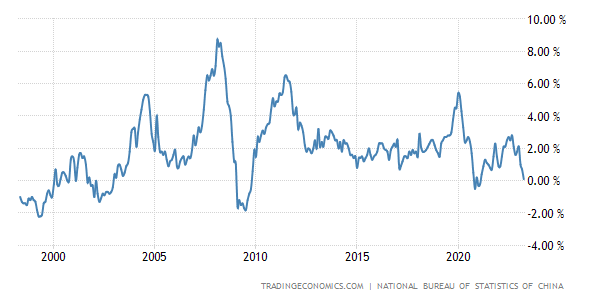

Chinese CPI is also quite different from the United States, where inflation approached double digits last year. This year, however, China has to worry about the opposite: deflation. Inflation is currently headed for one of its lowest levels over the past 20 years and seems to be heading even more south, similar to 2000 and 2008. An economy can usually handle some inflation, but the "debt deflation" scenario, is an ugly scenario that usually occurs during economic depressions such as 1929 and 2008.

Trading Economics

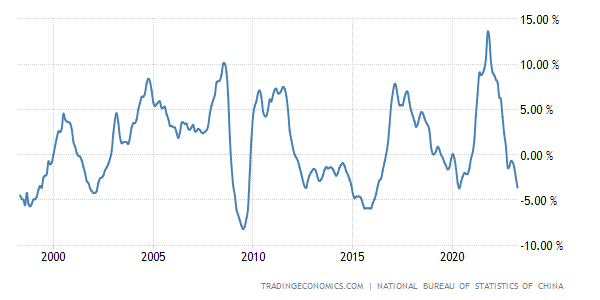

Another metric, the producer price index, has also plunged and is heading into deep negative territory. A negative PPI could also have further consequences, as it could lead to lower consumer spending and the postponement of purchases in anticipation of further price declines.

Trading Economics

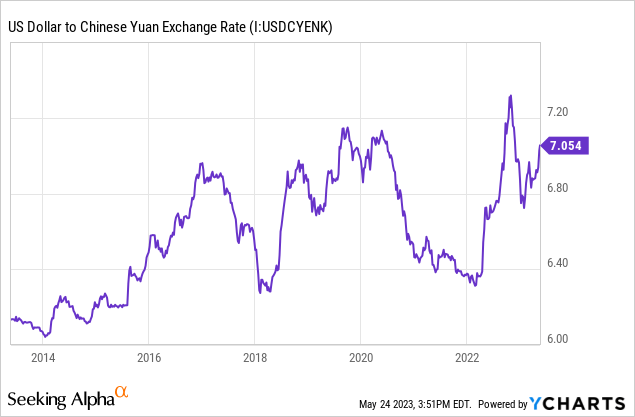

The Chinese yuan is also weakening against the U.S. dollar, which is currently fairly cheap at 7.06 RMB against USD, as it has broken through the 7:1 level. All these signals lead us to believe that the Chinese economy and consumer are not experiencing a "reopening boom," and are in worse shape than expected.

The Bottom Line

XPeng is operating in an extremely difficult environment, with Tesla waging a price war against BYD, with both manufacturers significantly cutting prices and seeing lower margins as a result. We think one of the first casualties of this price war will be XPeng, with significantly weaker demand and an inability to scale further unless it comes at the expense of gross margins.

For us, it is currently unclear how XPeng can get to escape velocity and scale up its production, while competing with BYD and Tesla, which arguably have a much greater value proposition at the moment, due to their size and the length of time they have been active in the EV sector. On top of all these headwinds, it does not appear that the Chinese macroeconomy will improve anytime soon. On a relative valuation basis and looking at tangible book value, we think XPeng's fair value is closer to $6 per share. However, we believe there are other great equities, such as Alibaba, Pinduoduo and JD.com, that are trading at dirt-cheap valuations and also offer exposure to the Chinese consumer and innovation.

We would wait for further signals, such as improving margins or stronger demand that may indicate further improvement in profitability, as XPeng currently remains too speculative, losing more than $376 million per quarter, as of Q1.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of JD,BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.