Mercury Systems Stock: A Silicon Valley Defense Buy On Acquisition?

Summary

- Mercury Systems is facing some temporary headwinds in FY2023.

- Product line and company strategy are extremely attractive as data and microelectronics demand for defense rise.

- Company offers value as a standalone business with possibilities of shareholder value creation to accelerate via acquisition.

- Looking for a helping hand in the market? Members of The Aerospace Forum get exclusive ideas and guidance to navigate any climate. Learn More »

DigtialStorm/iStock via Getty Images

Merger and acquisition in the aerospace industry is challenging for the simple reason that governments want to have access to affordable defense solutions. One company that seemingly has put itself up for sale is Mercury Systems (NASDAQ:MRCY). In this report, I will be having a look at what makes Mercury Systems attractive for investors but also for other aerospace companies.

About Mercury Systems: Silicon To Systems

Mercury Systems is a technology company serving the global aerospace and defense industry. The company provides sensor and processing technologies for mission-critical applications. Processing technologies that comprise its platform include signal solutions, display, software applications, networking, storage, and secure processing. It manufactures components, products, modules and subsystems for defense prime contractors, the US government, and original equipment manufacturers (OEM) commercial aerospace companies. Its products include embedded processing modules and subsystems, mission computers, rack-mount servers, safety-critical avionics, radio frequency components, multi-function assemblies, subsystems, and trusted custom microelectronics. Its mission critical solutions are deployed by its customers for a variety of applications, including command, control, communications, computers, intelligence, surveillance and reconnaissance (C4ISR), and electronic intelligence.

Mercury Systems: Attractive Business Positioning And Strategy

What makes Mercury Systems attractive is not just the generic bull thesis you can write about aerospace companies. That generic case is that with expanding defense budgets, there's the potential for higher sales for defense companies.

What makes Mercury Systems attractive on top of that is that they're involved in roughly 300 programs and they have a telling one-liner, namely: From data to decision, silicon to systems. Defense systems are becoming more and more advanced with data, data analysis and sensor packages. The core for that are micro-electronics to process everything and that's what Mercury Systems provides. Hensoldt, which I covered in an earlier piece, also has highlighted the growing component share of electronics and that's the way that Mercury Systems can ride. The company has a product program approach where it develops a product and subsequently implements it in multiple platforms as applicable. That's a great way to optimize the value of developed products.

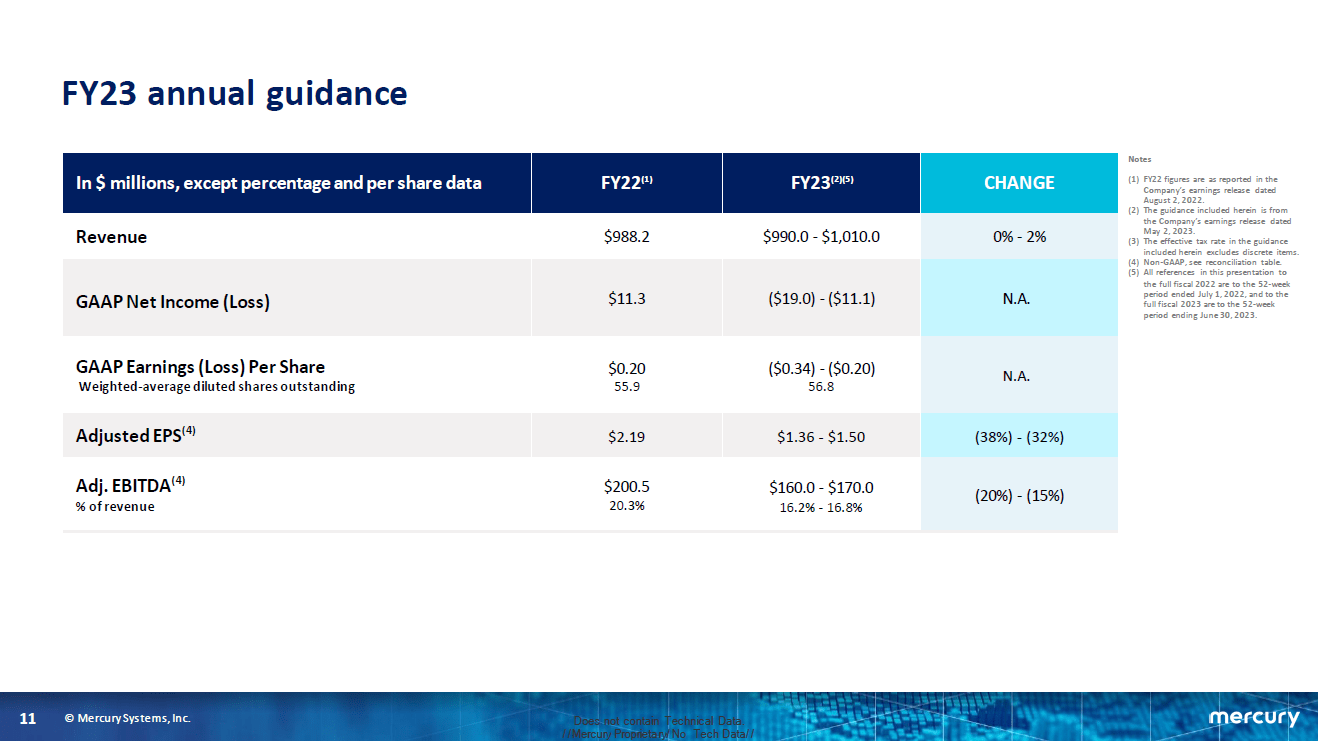

Short Term Pressures For Mercury Systems

Mercury Systems

If you look at the guidance for FY23 ending June 2023, we can see that while Mercury Systems has an attractive strategy its outlook for 2023 apart from low single-digit revenue growth shows decline. There are several things that are hurting Mercury Systems. Like for many companies higher interest costs provide a damper on income but also its EBITDA shows pressures. There are two primary reasons for that, the first is that supply chain issues in the aerospace industry are still very prevalent and secondly the company is having a higher share of development programs relative to its production programs at the moment and those are suffering from some delays and already have lower margins. So, all of that is making look Mercury Systems look less attractive relative to its prospects and strategic strength.

Mercury Systems As An Acquisition Target

Earlier this year, it became clear that Mercury Systems was considering opportunities to enhance shareholder value including a potential sale. The company does not provide details in the process as is usual and only noted there was progress. The previous aerospace acquisition that I closely followed was the acquisition of Aerojet Rocketdyne (AJRD). It took four months to go from public rumors to a deal being announced. Mercury Systems announced to explore strategic alternatives by the end of January. Adding four months from there gives around the end of May for some news to come. News actually came earlier. By mid-May, the sales process seems to have entered its second phase. I wouldn’t that second phase to be finished any time soon but I would expect something before the start of the fourth quarter.

Among the parties seemingly interested in Mercury Systems are Veritas Capital and Cobham, which both are private companies. Veritas Capital is a private equity fund that in the past has acquired various segment of defense companies. In 2005 it acquired Athena Innovative Solutions before selling it to CACI (CACI), it later acquired a business of Lockheed Martin (LMT) and acquired the services businesses of QinetiQ (OTCPK:QNTQF) in North America and acquired the IT services department of Harris Corporation, now L3Harris Technologies (LHX), renaming it Peraton which it has been growing through an acquisition of a Northrop Grumman (NOC) business and a cybersecurity acquisition in 2021.

So, Veritas Capital does have experience acquiring defense business though the most notable acquisitions in recent years were focused on government/defense IT Services. Cobham was the first name that popped up as a potential acquirer and that makes a lot of sense. Cobham runs charter services through its Aviation Services business in Australia but its two other segments namely Cobham Advanced Electronic Solutions and Cobham Communications and Connectivity fit very well with the micro-electronics solutions as well as the C4ISR and electronics intelligence solutions that Mercury provide. So, an acquisition by Cobham makes a lot of sense.

None of the companies I mentioned are unfamiliar to me. Mercury Systems, Peraton, L3Harris Technologies, Northrop Grumman, CACI and Cobham all are included in the evoX Defense Monitor where we track their contract awards. In 2022, Mercury Systems was awarded a total of $509.25 million in various contract vehicles by the Department of Defense.

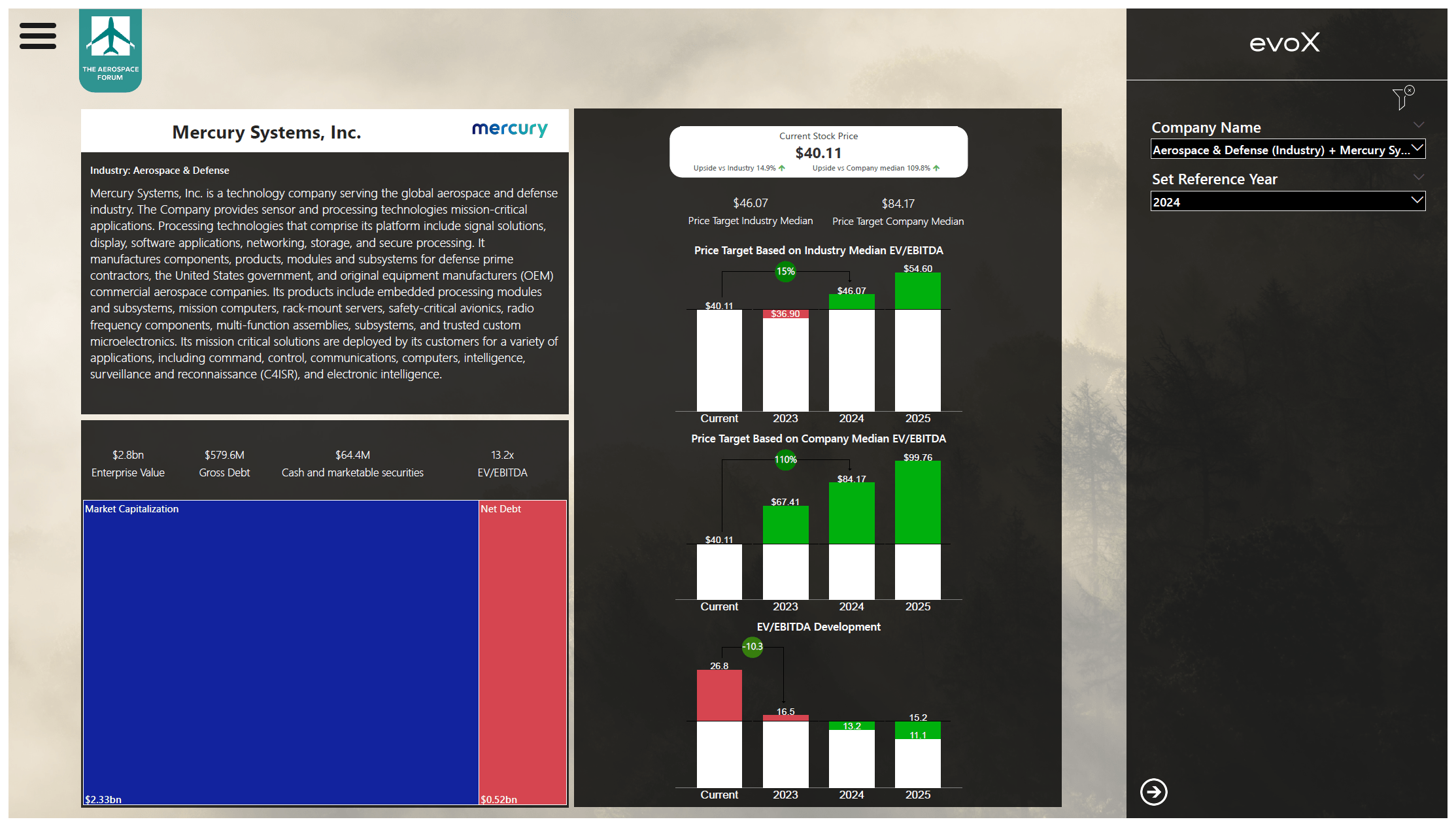

What's The Right Price For Mercury Systems Stock?

The Aerospace Forum by evoX

Valuing Mercury Systems is challenging because we can either value it as a standalone company, which would show 15% upside compared to the current stock price and even 110% upside when we consider that Mercury Systems tends to trade on expanded EV/EBITDA multiples.

For takeovers, I apply a premium of 30% to 40%, which would bring the price target to the $52-$56 range. The Wall Street Journal reported earlier this year that a sale could fetch $3.5 billion which would indicate a 50% premium from current prices but it should also be noted that back then, the market capitalization was around $2.8 billion which would put the premium at only 25%. So, ideally I'm looking at something in the range of $52 to $56 with $50 as the bare minimum.

When filling in the numbers for 2023-2025 in our valuation tool for subscribers of The Aerospace Forum, we find that while according to industry median multiples Mercury does not have a lot to offer with FY2023 numbers in mind it should get significantly better beyond that. This also provides support for a good acquisition price.

Conclusion: Mercury Systems A Buy On Defense Momentum And M&A

I wouldn’t solely recommend Mercury Systems because it's a potential takeover candidate for the simple reason that in the case no transaction takes place, I want investors to be invested in a quality name. I believe that's the case with Mercury Systems, which is going through a negative revenue and margin mix this year but its overall business strategy and product line is extremely well positioned to take advantage of the continued evolution of defense systems with higher electronic components share. This makes the company attractive for investors but also for potential takeovers.

If you want full access to all our reports, data and investing ideas, join The Aerospace Forum for the #1 aerospace, defense and airline investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.

This article was written by

His reports have been cited by CNBC, the Puget Sound Business Journal, the Wichita Business Journal and National Public Radio. His expertise is also leveraged in Luchtvaartnieuws Magazine, the biggest aviation magazine in the Benelux.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.