Alibaba: Deep Value With IPOs Ready To Launch

Summary

- Reports indicate the CV19 lockdowns in China are easing, which I believe will benefit China's largest local commerce segment, which is weighing down the business' growth.

- I admire managements rapid response and the laying out of timelines for various IPO's from its AI enhanced Cloud to its logistics business.

- In April 2023, Alibaba launched its AI large language Model (LLM) and aims to integrate it into all business applications across Alibaba's business and then roll it out to enterprises.

- I believe we are at an inflection point for Alibaba and its spread between price and value has now become enticing, according to my sum of parts model.

maybefalse/iStock Unreleased via Getty Images

Alibaba (NYSE:BABA) is often referred to as the "Amazon of China" and has to be one of the most controversial and newsworthy stocks on the planet. From becoming an e-commerce powerhouse over the past decade to being slapped with a $2.8 billion fine in a landmark antitrust suit in 2021. A positive is it looks as though we are now close to a rebound for Alibaba and its spread between price and value has widened greatly. This has been further enhanced by the planned spin-off of multiple segments. Even together, Alibaba beat its earnings expectations for the March quarter of 2023 and management has outlined a timeline for IPOs which is fantastic. The business has also repurchased approximately $10.9 billion of stock (44% of free cash flow) throughout the fiscal year of 2023, which is a strong positive for existing shareholders. In this post I'm going to break down the company's March Quarter results before revising my sum of parts valuation for the stock, let's dive in.

The Covid Storm is Easing

Alibaba reported mixed financial results for the March Quarter of 2023. Its revenue was $29.59 billion which declined by 5.8% year over year but still increased by 5.98% over a two-year period.

On a constant currency basis, Alibaba's revenue actually increased by 2% year over year. This result was driven by its largest segment China Commerce, which reported RMB 136 billion ($19.4 billion), falling by 3% year over year.

On the face of things, it looks as though Alibaba has reported mediocre top-line results. However, I believe this has been mainly driven by macro conditions, as China's hard lockdown policy, choked e-commerce revenue. However, I have discovered a variety of positive announcements related to China that indicate an easing of this policy. In mid-April 2023, China's Disease and Control Authority clarified that masks were no longer mandatory on public transport. On April 1st 2023, the high-speed rail link between China's largest economic hubs Shanghai and Hong Kong reopened.

On the travel front, on April 29th, 2023, China removed the need for a PCR test 48 hours before boarding. In addition, China's passenger aviation industry has recovered to 82.3% of levels reported in 2019.

Now of course, these news updates are not all directly related to Alibaba, but they are a major sign of potential tailwinds to come and no doubt will improve consumer psychology. In fact, Fitch has recently raised its GDP forecast for China from 4.1% to a solid 5% for 2023. A solid figure given U.S GDP forecasts indicates just 0.7% growth, a snail's pace if investors are lucky.

Specifically to Alibaba, the reports about positive improvements with regards to travel, have already begun to show up in Alibaba's Fliggy travel app, which reported a 70% increase in domestic hotel bookings since 2019.

This result laddered up to driving its Local Consumer revenue up by 17% year over year to RMB12.5 billion or $1.78 billion. This was also driven by continued order growth in (Ele.me) Alibaba's online food delivery segment, which I believe has actually been has benefited from the hard lockdown policy.

Alibaba has started to introduce many new features into its Taobao e-commerce app. A highlight in April was its interface improvement which gave increased exposure to live-streaming e-commerce. According to one study, 40% of Chinese Citizens were using live-stream shopping in 2021 and by 2023 the market is expected to be worth a staggering $720 billion.

Its Taobao Deals platform has also continued to be popular as users were attracted by value, given the macro backdrop. Fresh food is also a popular trend that is growing in China and Alibaba's Taocaicai community marketplace reported 62% of its active customers were first-time buyers in the trailing 12 months.

Another positive for Alibaba is its International Commerce segment reported a solid 29% year over year RMB 18.5 billion ($2.6 billion). With strong growth in AliExpress and Lazada (Philippines) which is one of the largest e-commerce operations in South East Asia, a thriving emerging market. Its fast fashion brand Trendyl has also been generating strong results and my estimates (SimilarWeb data) indicate 153 million website visits in April 2023, up from 138 million in February 2023.

In my previous post on Amazon, I discussed that the clothing category is one of the greenfield opportunities still ripe for e-commerce penetration with around 39.4% reported globally. If I compare this to Media, at 78.2% there is huge potential ahead.

Its Cainiao Logistics segment is one of Alibaba's competitive advantages in my mind as its vast network of warehouses and fulfillment centers is interlinking and optimized with data to drive customer satisfaction. This segment grew its revenue by 15% year-over-year to $2.75 Billion (RMB18.915 billion).

Huge Cloud and AI Opportunity

Alibaba has a huge opportunity in the Cloud given it is estimated to be the market leader in China, with ~37% market share. A forecast by McKinsey, also suggests the cloud industry will grow from $32 billion in 2021 to close to $90 billion by 2025. China's legacy manufacturing sector is still fairly antiquated when it comes to the cloud and thus there is major potential.

I believe Alibaba can also take inspiration from Amazon, of whose AWS cloud is its fastest-growing and most profitable segment.

In the March quarter of 2023, Its Cloud segment reported $3.58 billion in revenue which dipped by 3% year over year. Management put this dip down to "delays" relating to cloud project delivery, driven by CV19 hard lockdowns. As I discussed earlier I believe this is a temporary issue and all signs put to an easing in restrictions.

AI has also been a hot topic and Alibaba is poised to benefit from this vast and growing industry.

In April 2023, Alibaba launched its large language Model (Tongyi Qianwen) and aims to integrate it into all business applications across Alibaba's business and then roll it out to enterprises.

This effectively means Alibaba is poised to replicate what Microsoft (MSFT) is aiming to accomplish in the West with its generative AI models, after a $10 billion investment into Open AI.

Microsoft CEO Satya Nadella stated in a recent interview that "every app will become an AI app" and I believe will be correct and Alibaba is in a prime position to accelerate this philosophy in China.

Since the model launch in April 2023, Alibaba has already received over 200,000 bet testing requests from enterprises.

Alibaba's Cloud AI has also announced integration with its DingTalk workplace application platform. This enables users to activate AI capabilities simply by using the slash symbol. Examples include blog post generation, image generation etc.

IPO's Ready to Launch

Alibaba's Cloud aims to be listed publicly in the next 12 months. Interestingly enough in a past post I stated "Amazon should Spin off AWS", It now it looks as though Alibaba has executed to the equivalent. I would love to invest into AWS individually and although Alibaba's Cloud is not the same, it has a vast amount of potential.

In my previous post on Alibaba, I discussed in detail the benefits of a split into multiple segments including faster decision-making, capital raising, and ultimately an unlock of shareholder value is likely.

Alibaba's board has also approved Freshippo's plan to IPO within the next 6 to 12 months and its Cainiao logistics segment is expected to explore an IPO within the next 12 to 18 months.

Alibaba's Digital Commerce Group is also exploring the raising of external capital which could be lucrative.

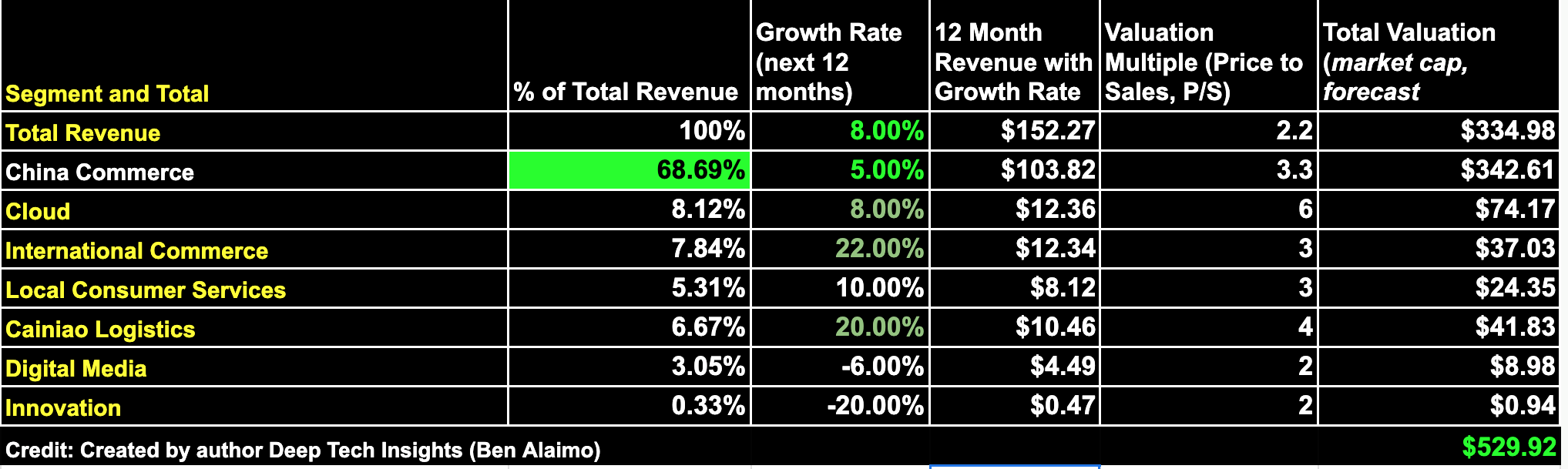

Sum of Parts Valuation - Updated

In my previous post, I did a detailed Sum of Parts valuation which I believe hasn't changed much, but there are a few changes I will point out.

Firstly, I have revised up its cloud revenue growth from 6% estimated to 8% growth within the next 12 months. The extra 2% I have attributed to Artificial Intelligence and upsells from its enterprise AI offering.

Its International commerce segment performed much better than I expected in the March quarter of 2023 with 29% year-over-year growth. Therefore I have revised my estimate up from my 19% growth rate to 22%, for the next four quarters.

Alibaba Sum of Parts (Q1,23)

Its Local Consumer segment also did better than I had expected and thus I have revised my growth rate up by 2% to 10% year over year.

Its Cainiao logistics segment generated solid 17% growth but this was much lower than my expected result which was driven by a strong holiday usage quarter I believe. Therefore I have revised my growth estimate downwards 20% from 28%, which is still higher than the recent quarter but not by as much.

Given I have kept my 5% growth rate the same for its largest segment (China e-commerce segment), the changes look to have kept my fair value estimate relatively the same.

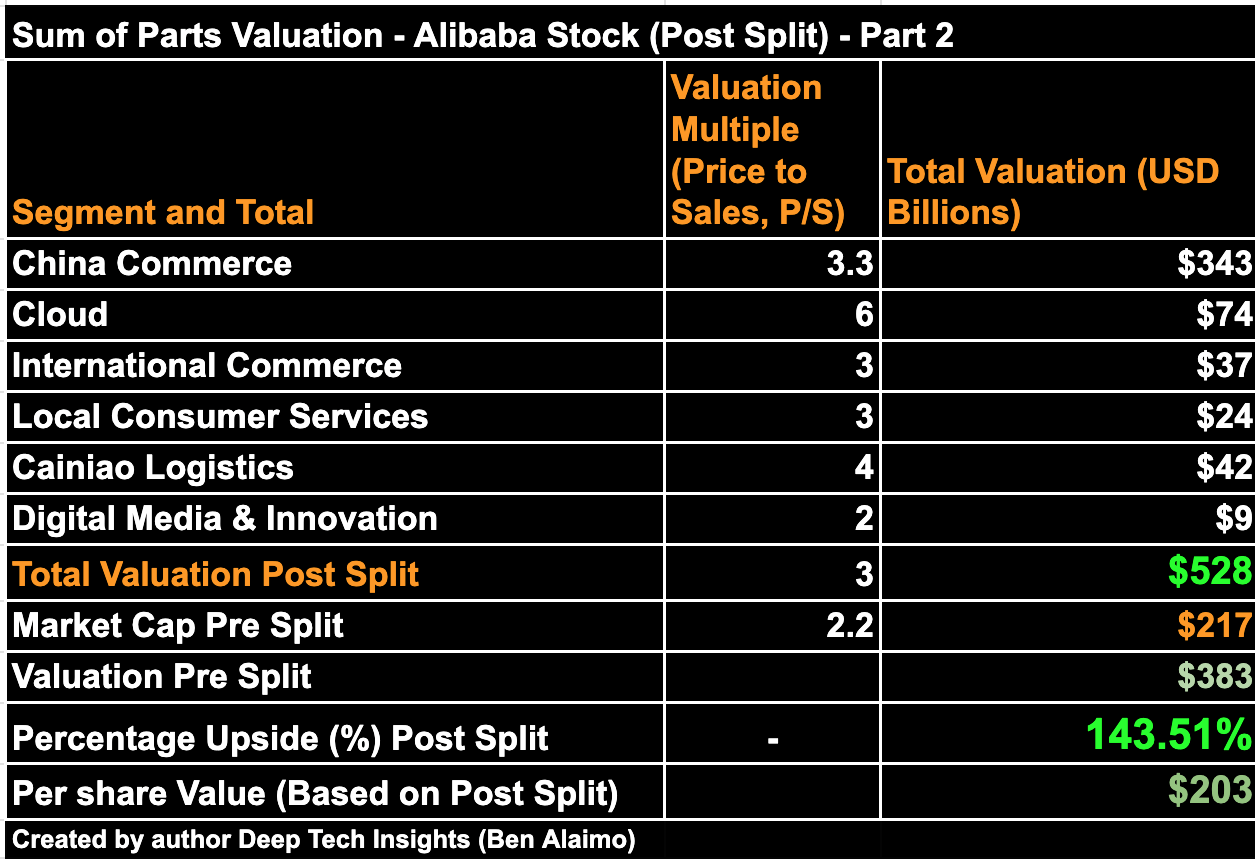

On the table below, you can see I have added various pricing multiple estimates which I would expect when the company IPO's a segment. For example, I have given a higher price to Sales multiple (6) for its Cloud segment due to it likely receiving a "tech" valuation and also an AI tailwind. However, I have given a lower multiple to some of the other "less exciting" and more traditional segments. I outlined further justification for these multiples in my prior posts.

Alibaba Sum of Parts 2 (Q1,23)

Given these factors, I get a fair valuation post-split of $528 billion. This is similar to my prior estimate (when rounded). However, as Alibaba's share price has declined the gap between price and value is now even greater. Alibaba now has an upside of approximately 143.5%, up from "just" 94% in my prior post. For reference, I have also included my standard DCF valuation figure which also indicates the stock is undervalued also the extent is not as great.

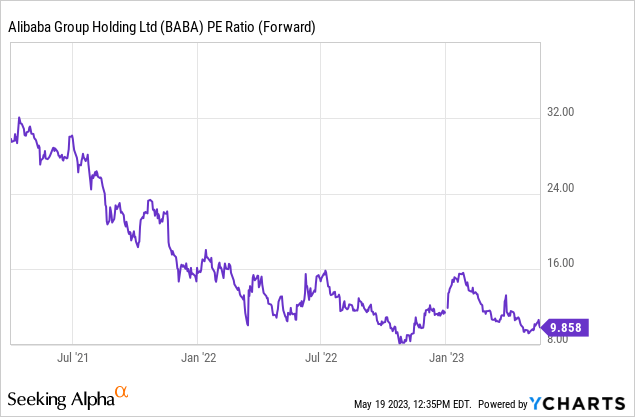

For completeness, Alibaba trades at a forward price to earnings (P/E) ratio equal to 9.8x, which is ~60% cheaper than its 5-year average.

Risks

Fierce Competition

Alibaba faces fierce competition from rivals such as JD.com (JD), PDD Holdings (PDD) and many more. This is more intense than ever and Pinduoduo is especially generating strong growth in both its domestic and international services.

Final Thoughts

Alibaba's largest segment is still its traditional domestic commerce and thus even when the smaller segments do well this doesn't move the needle on the top line. Therefore I believe a split of the businesses is welcome not just from a mechanical perspective but from a psychological perspective. The stock looks to be undervalued deeply via multiple methods from a Sum of Parts to a traditional DCF. Given management's rapid timeline announcements, I forecast a strong rebound for Alibaba in the near future. Given the majority of the west has a recession forecasted, China looks to be one of the few places where growth is possible.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.