Six Flags Entertainment: Attendance Drop On Price Increases

Summary

- Six Flags took significant price increases in 2022, causing a 26% drop in attendance YOY.

- Management acknowledged the aggressive pricing approach in the Q4 2022 call and plans to adopt a more relaxed strategy in the upcoming year to address the situation.

- Despite a 5% decline in attendance in Q1 2023 (attributed to bad weather), adjusted for weather, attendance would have been up by 6%.

- The valuation of Six Flags remains attractive, with the market cap at 8 times 2019 AFCF and 12 times the 2022 AFCF. Management expects a double-digit growth in attendance in 2023.

skynesher/E+ via Getty Images

Introduction

I review each position in my portfolio on a yearly basis and now it’s time for Six Flags Entertainment (NYSE:SIX). In my last article, I went into more detail on the thesis for Six Flags linked here. In summary, the company appears to be undervalued when considering its profitability before the COVID-19 pandemic. Moreover, the new management team has taken a new approach by implementing price increases and making improvements to the parks. To make it easier to track my investments, I’ve been finding four metrics for all my investments. For SIX stock, the four metrics are attendance, AEBIT, AFCF, and revenue.

Highlights

My thesis for Six Flags was that they'd return to pre-covid profitability and reinstate the dividend to pre-covid levels and then re-rate to 16-20 times FCF like they were trading pre-covid. With this in mind, I opted to monitor the adjusted earnings before interest and taxes (AEBIT) and adjusted free cash flow (AFCF) metrics to track profitability.

For attendance and revenue, new management announced significant announcements including substantial price increases. I agreed with the price increases as Six Flags seemed underpriced compared to peers. I assumed that Six Flags had some price inelasticity, suggesting that they would be capable of maintaining attendance levels and expanding revenue significantly. Hence, I selected attendance and revenue as the two metrics to track for evaluating these aspects of Six Flags' performance.

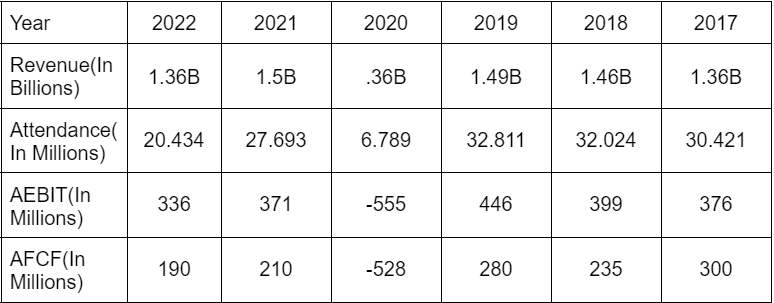

Source: Author created table data from Six Flags 10-K’s

- AFCF=OCF-ΔWC-D&A

AEBIT=OCF-ΔWC-D&A+Interest+Taxes

The year 2022 didn't turn out to be a great one for Six Flags. They made significant price hikes, and as a result, guest spending per capita now matches that of their competitor, Cedar Fair. Guest spending per capita reached $64, reflecting a substantial 22% increase compared to the previous year. However, the downside was that attendance dropped by a staggering 26%, reaching only 62% of the 2019 levels.

Now, I'm not ready to admit that my assumption about Six Flags' price inelasticity was entirely off the mark just yet. I believe the decline in attendance can be mostly attributed to customers being taken aback by the sudden price increase and the removal of many discounts and the meal plan. In fact, after watching some YouTube reviews, it's clear that people are not thrilled about these changes.

It's worth noting that the decrease in attendance is partially intentional. As I mentioned in my previous article, the parks were overcrowded, and management has been aiming to address that issue. However, I don't think the attendance was intended to be this low, considering that in the Q4 call, management stated that their target for attendance is around the same level as 2021 or slightly higher.

Management in the Q4 2022 call acknowledged that they might have implemented price increases too aggressively. As a result, they plan to take a more relaxed approach this year. In the Q1 2023 call management said they are expecting double-digit attendance growth with most of the uplift coming in Q3. Attendance in Q1 2023 was down 5% however this was due to bad weather and if adjusting for the weather it would have been up 6%. This bad weather was confirmed in both Cedar Fair (FUN) and SeaWorld (SEAS) Q1 2023 conference calls.

Park Improvements

New management also promised back in their Q4 2021 call to introduce new and better food options and modernize the parks with technology. In terms of food I found a number of articles and guest experiences highlighting the new food options linked here and the guest experiences seem positive.

- New Jersey Park

- Boston Park

- Six Flags America

- Six Flags over Georgia

In terms of technology,

- Q1 2022 call, started installing digital screens to display wait times for rides.

- Q1 2023 call, implemented wristband technology to allow payments without credit cards.

- Q1 2023 call, a new mobile app will be rolled out in June.

- Q4 2022 call, Apple and Google pay options soon to be added.

Overall I’m happy with the tech and food progress.

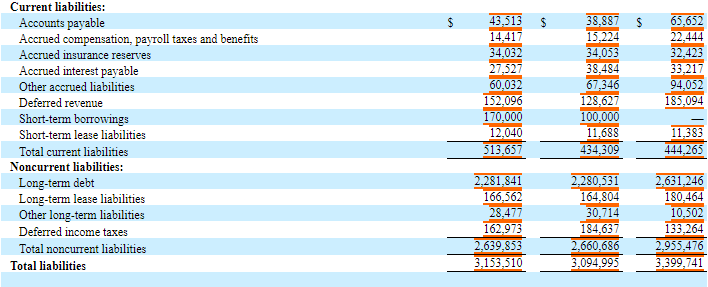

Debt

Another promise of management was to reduce the debt, which they have. Total liabilities went from 3.4B at the end of 2021 to 3.15B as of Q1 2023.

Source: Q1 2023 10-Q Six Flags

Six Flags also took care of their 2024 debt maturity rolling it over with a 800m note due in 2031. The one downside being that the interest rate went up to 7.25% from 4.875%. The 2024 maturity was their largest at $1B. The next maturity is in 2025 with 365M needing to be rolled over or repaid. Higher interest expenses will be a headwind for FCF.

Random Fact

For whatever reason Six Flags is adding a bunch of gaming PCs to some of their parks. This is to host live esports events. This is weird for two reasons. One, in the new CEO’s first earnings call he said he wanted to appeal more to families and not teenagers. I don’t know many families that are into esports tournaments. Two, they are sponsored by Coca-Cola. Anyway, I only mention it because at face value it seems ridiculous.

Source: Six Flags 2023 Press Release

Valuation

Six Flags is still trading at an attractive valuation with a market cap of 2.2B which is 8 times 2019 AFCF and 12 times 2022 AFCF. Six Flags management is expecting 10% attendance growth in 2023 with about the same level of pricing, which would be about 1.44B in Revenue and 202M in AFCF. To get back to 2019 levels of AFCF Six Flags would need 95% of their attendance in 2021 assuming no price increases. I think this is attainable within 4 years. And with a 16 multiple, the target share price would be $53 a share with over a 10% shareholder yield at the current price.

In my previous article, I also touched upon the topic of dividend reinstatement. However, thus far, Six Flags has not taken that step. Instead, they have engaged in approximately $100 million worth of share buybacks. This is a far cry from the capital distribution in 2019 of 278M. Although I anticipate that the capital distribution will eventually reach similar levels, I believe that for the next couple of years, the company may choose to retain earnings to prioritize debt reduction though.

Conclusion

In summary, Six Flags has been making progress in executing its 2021 plan. However, the aggressive price increases had a larger impact on attendance than initially anticipated. Nevertheless, I anticipate that attendance will begin to recover this year, especially as the parks continue to undergo improvements. I believe that over the coming years, attendance will show positive growth and reach around 2021 levels.

If attendance isn't at least positive this year, I may need to rethink my investment. However, I am inclined to give the investment a minimum of 5 years to unfold, considering the potential for returns.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SIX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.