United, We Stand: A Great Option For Income-Oriented Investors

Summary

- United Airlines is growing, profitable, and attractively valued.

- Risks to the company are minimal, and the company's liquidity position is solid.

- We wish the company revamped its fleet when borrowing costs were lower; new, higher-cost debt could hamper capital return to shareholders in the medium term.

- As a result, selling put options for income, and a potential stake in the company at a lower price, seems like the most attractive option.

Justin Sullivan/Getty Images News

United Airlines (NASDAQ:UAL), one of the largest players in the commercial airline industry, stands out in its industry due to its quick rebound from the pandemic, robust operating results, and solid management execution. Despite the volatile market conditions of the last few years, the company has consistently demonstrated resilience and an ability to produce free cash flow, cementing its status as an investable business. Currently, the company trades at an attractive valuation, both on a relative basis, but also in comparison to its own pre-pandemic levels. With a hot summer travel season around the corner, UAL is poised to deliver great results and build on the momentum it has gained coming out of the pandemic.

However, rather than buying shares outright, a less risky and potentially more profitable strategy may be in play: selling put options. This strategy can generate immediate income to investors, reduce cost basis in the stock if assigned, and allow investors to profit even if the share price remains stable or decreases moderately.

Financial Results

A look at UAL’s recent financial performance reveals a mix of strengths and weaknesses, although things are trending in the right direction overall.

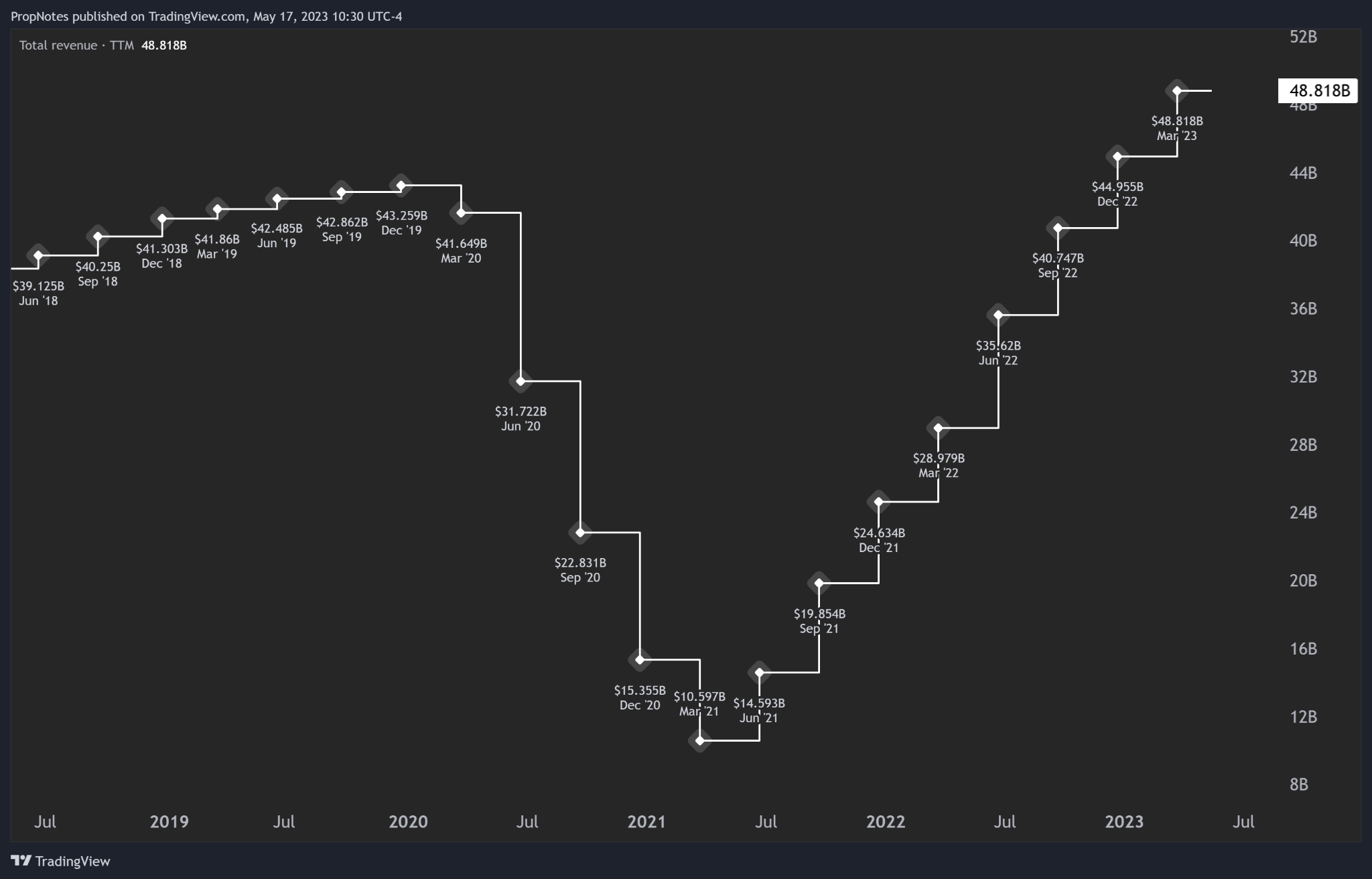

On the positive side, the company has shown strong top-line growth as it has emerged from the pandemic slump, with recent TTM revenue soaring to an all time high at $48.8 billion, a 68% increase year-over-year:

TradingView

This growth appears to be driven by a rebound in load factor post pandemic (more demand for travel), in addition to increased flight capacity of more than 20%. More flights equals more revenue.

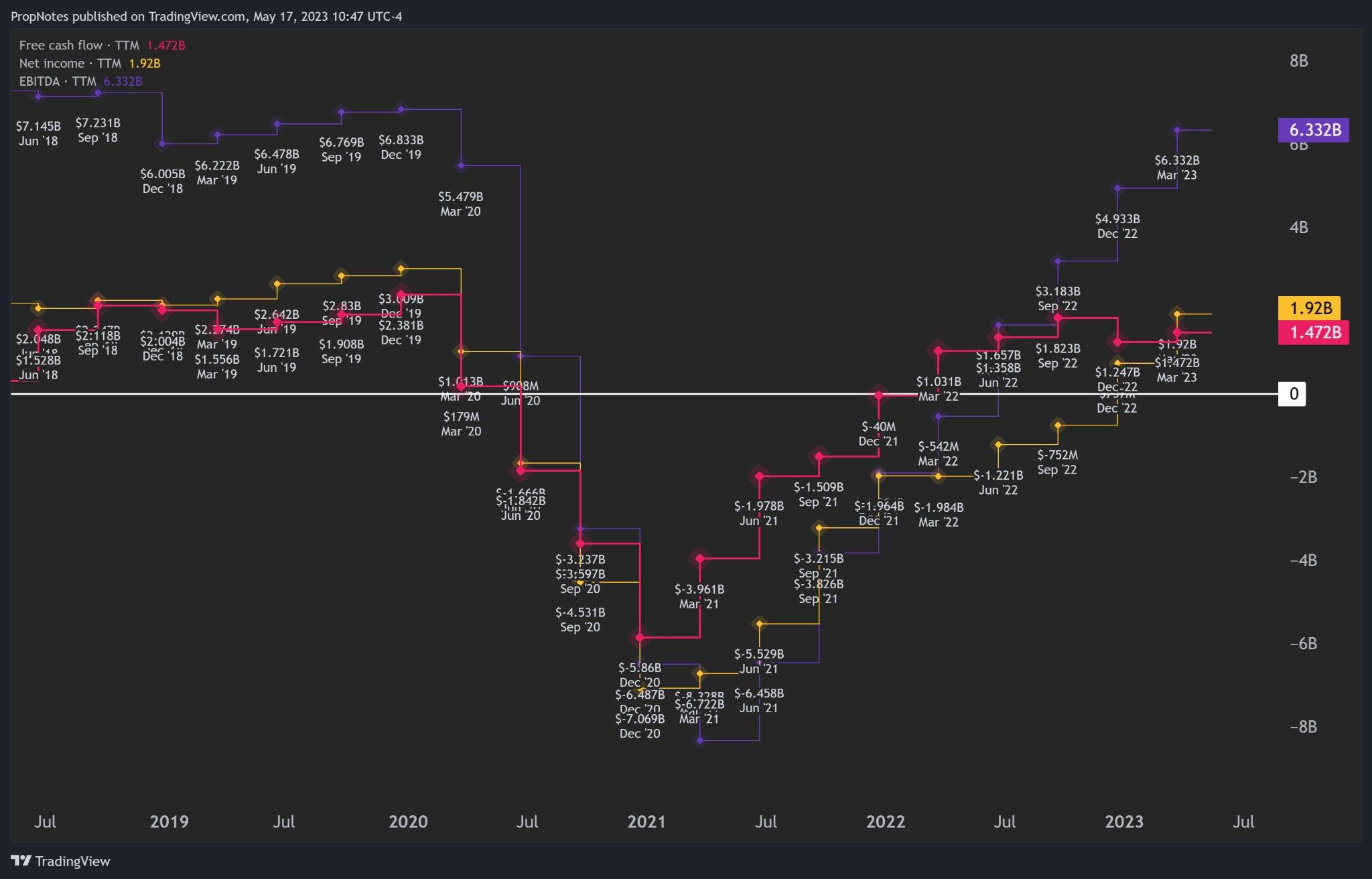

But has this surge in revenue translated to increased profits? Well, yes. Yes, it has:

TradingView

Whether you’re looking at EBITDA, Free Cash Flow, or Net Income, profits have recovered from the pandemic pit of despair. While they haven’t recovered to the degree that revenue has as a result of higher labor and fuel costs, as those pressures ease we should see continued progress on this front.

Additionally, management has been taking steps to reinvigorate the company fleet, through its “United NEXT” plan. This was announced a while ago, but recent orders have materialized, proving that management was serious about executing this revamp. These new planes have more first-class seats (which are rarely discounted), along with significantly improved fuel economy, both of which should contribute to higher profits.

On the liquidity front, the company maintains a solid cash balance of $17 billion, which is more than enough to cover current expenses of $10.5 billion. When it comes to liquidity, we don’t count the $12 billion in “Unearned Revenue” opportunity cost accounting line item. Overall, liquidity is strong.

However, the balance sheet is where we do see some issues for UAL. While assets and solvency are great, the fleet revamp we mentioned is happening at a poor time in the capital cycle. Rates are higher than they have been in a long time, which means that UAL will be adding a LOT of expensive debt to its balance sheet. This hasn’t shown up in levered free cash flow yet, but it may hamper the company’s ability to return capital to shareholders in the medium term. We’ll have to wait and see if the efficiency improvements of the fleet upgrade can counteract the higher debt servicing costs.

All in all, UAL is a solid company, with no near-term issues and growing revenue and profitability.

Valuation

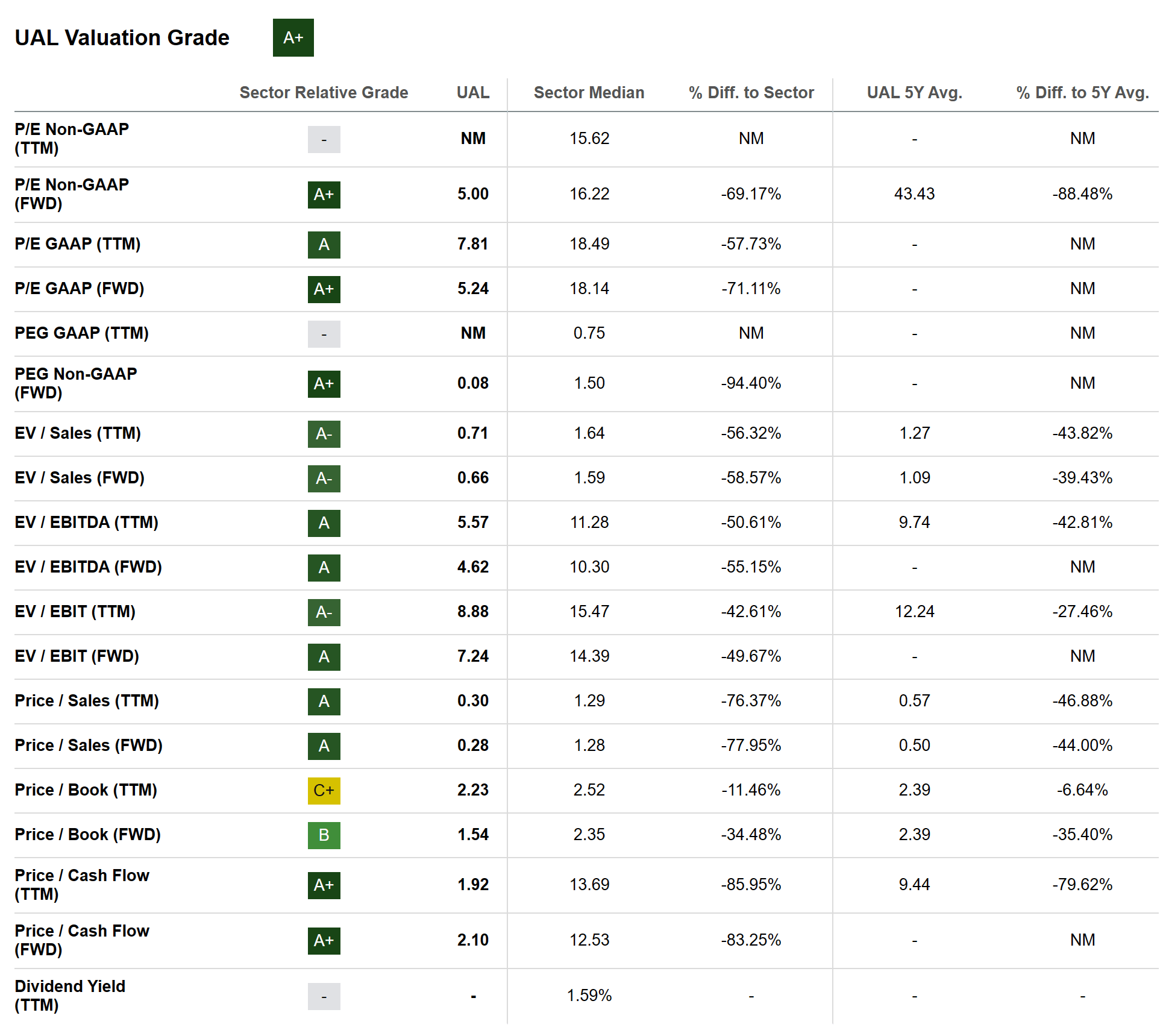

When it comes to UAL, the valuation is what stands out. While the company is on solid financial footing and executing from an operational perspective, the company’s current valuation, at only 5 times forward GAAP earnings, is what really has our mouths watering.

Seeking Alpha’s Quant Rating system grades UAL’s current value at an “A+”, a mark we absolutely agree with:

Seeking Alpha

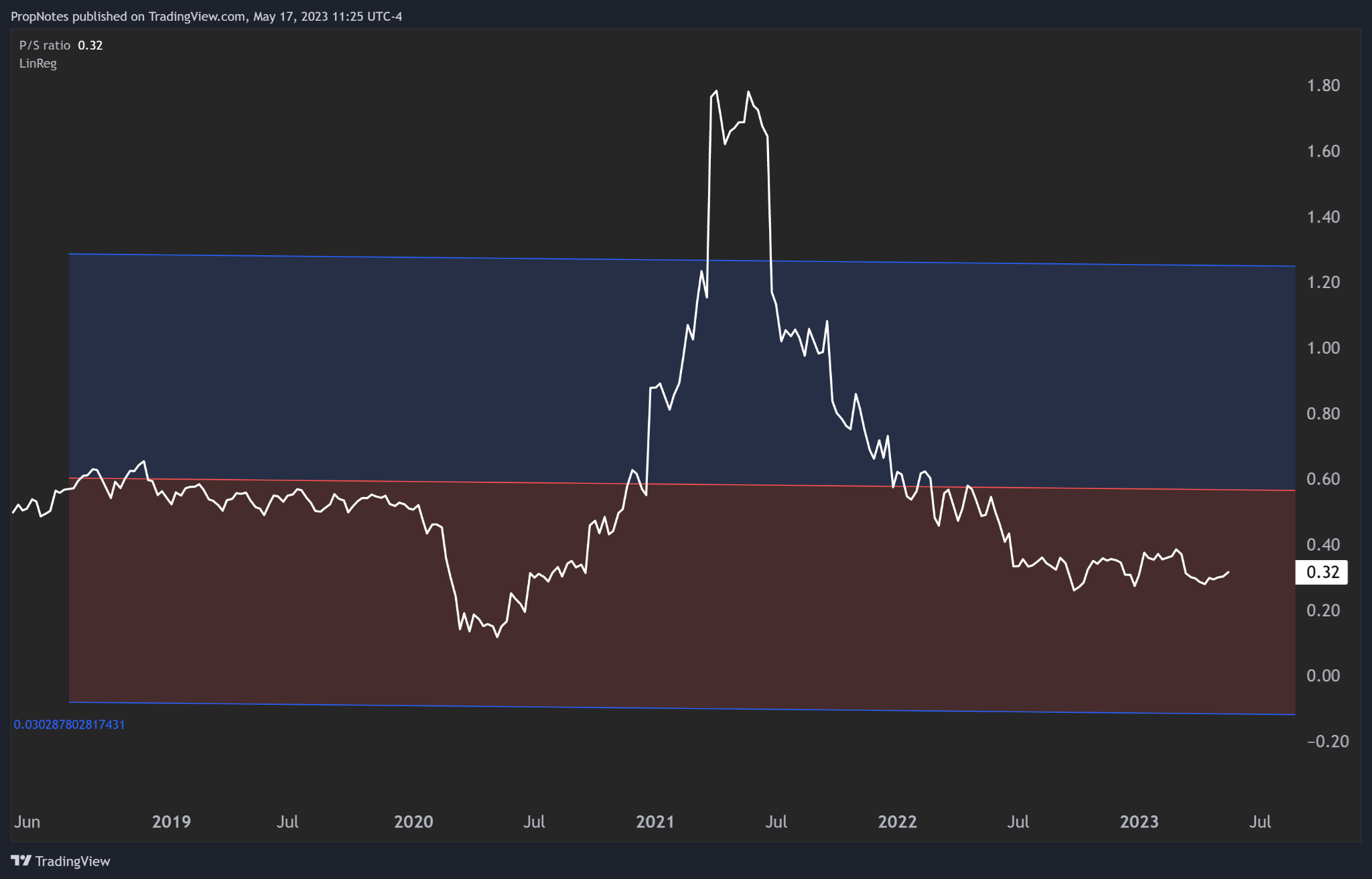

United is currently trading at, in some cases, more than 40% discounts vs. historical revenue and profit multiples. You can see this illustrated here by looking at Price to sales over the last 5 years:

TradingView

One could argue that COVID skews the results here, but even so, it’s still trading firmly below where it was pre-pandemic.

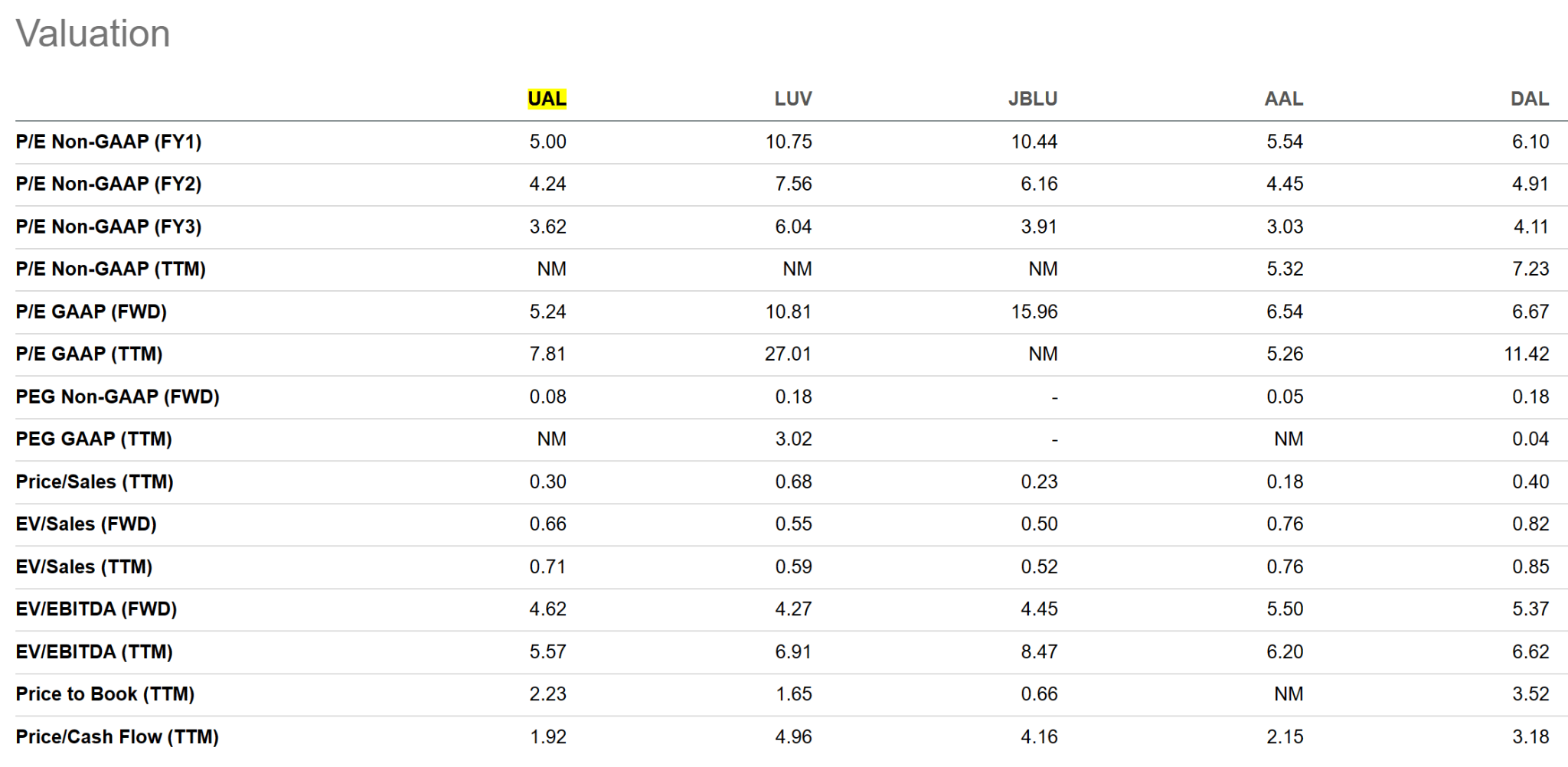

However, it’s not only historically cheap, but also attractively positioned compared to its competitors:

Seeking Alpha

Here, UAL scores the cheapest or second cheapest marks on almost all of the metrics above, including P/E GAAP and non-GAAP, Price/Cash Flow, Price/Sales, PEG, and more.

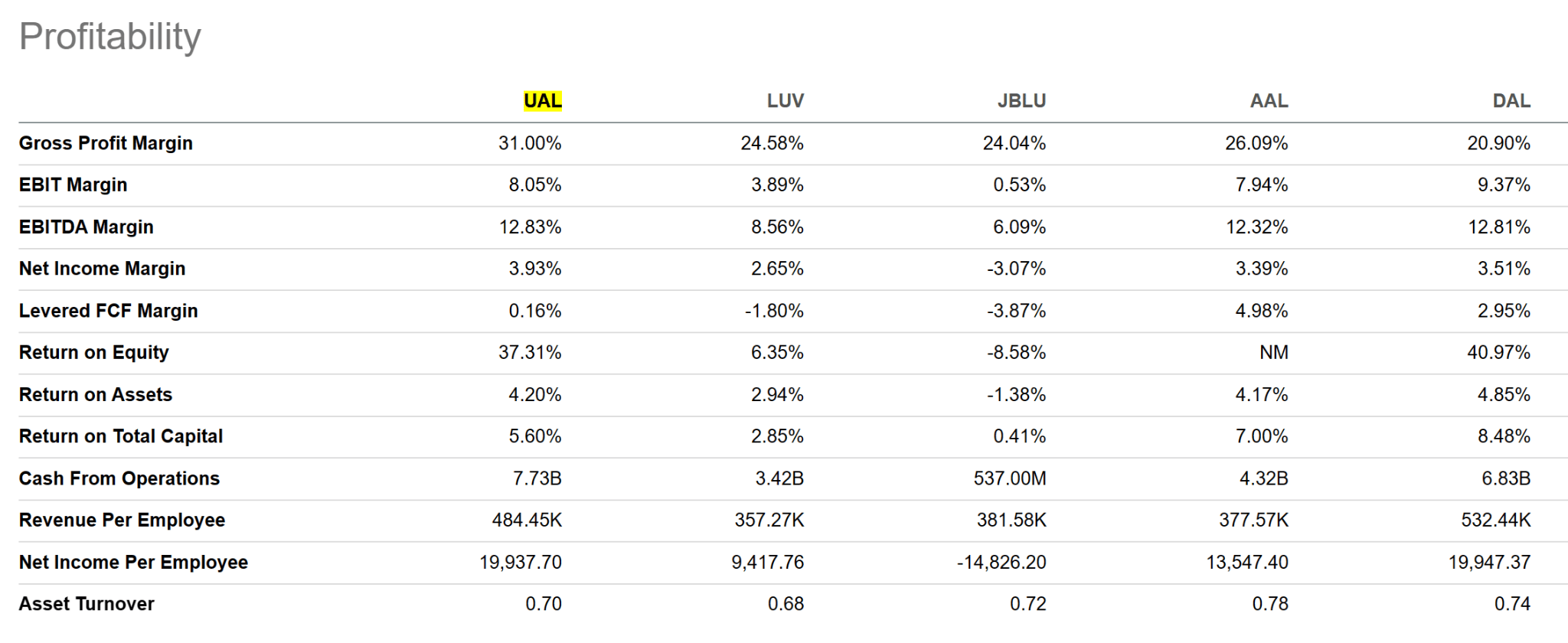

This doesn’t make a lot of sense when you compare the company’s relative profitability, cash from operations, and return on equity, which are all head and shoulders above everyone except for Delta (DAL), who has historically been the profit leader:

Seeking Alpha

Taken together, the company’s solid operations and attractive historical/relative valuation and performance make this a juicy looking setup for investors.

The Trade

What if there was a way to generate income immediately, while still getting portfolio exposure to UAL?

There is! It’s a strategy called put selling, and we think it’s the best way to take advantage of UAL’s stock and underlying operations. Company stability isn’t really in question here, so what we should be asking ourselves is how to get a return on capital as quickly as possible for our risk. Selling puts seems like the best way.

How does selling puts work?

When you sell a put option, you're essentially agreeing to buy the underlying stock at a certain price (the strike price) before a specified date (the expiration date). If the stock price remains above the strike price, the put option will expire worthless, and you keep the premium you received for selling the option. If the stock price falls below the strike price, you will be obligated to buy the stock, effectively at a discount when factoring in the premium received, and vs. today’s fair market value.

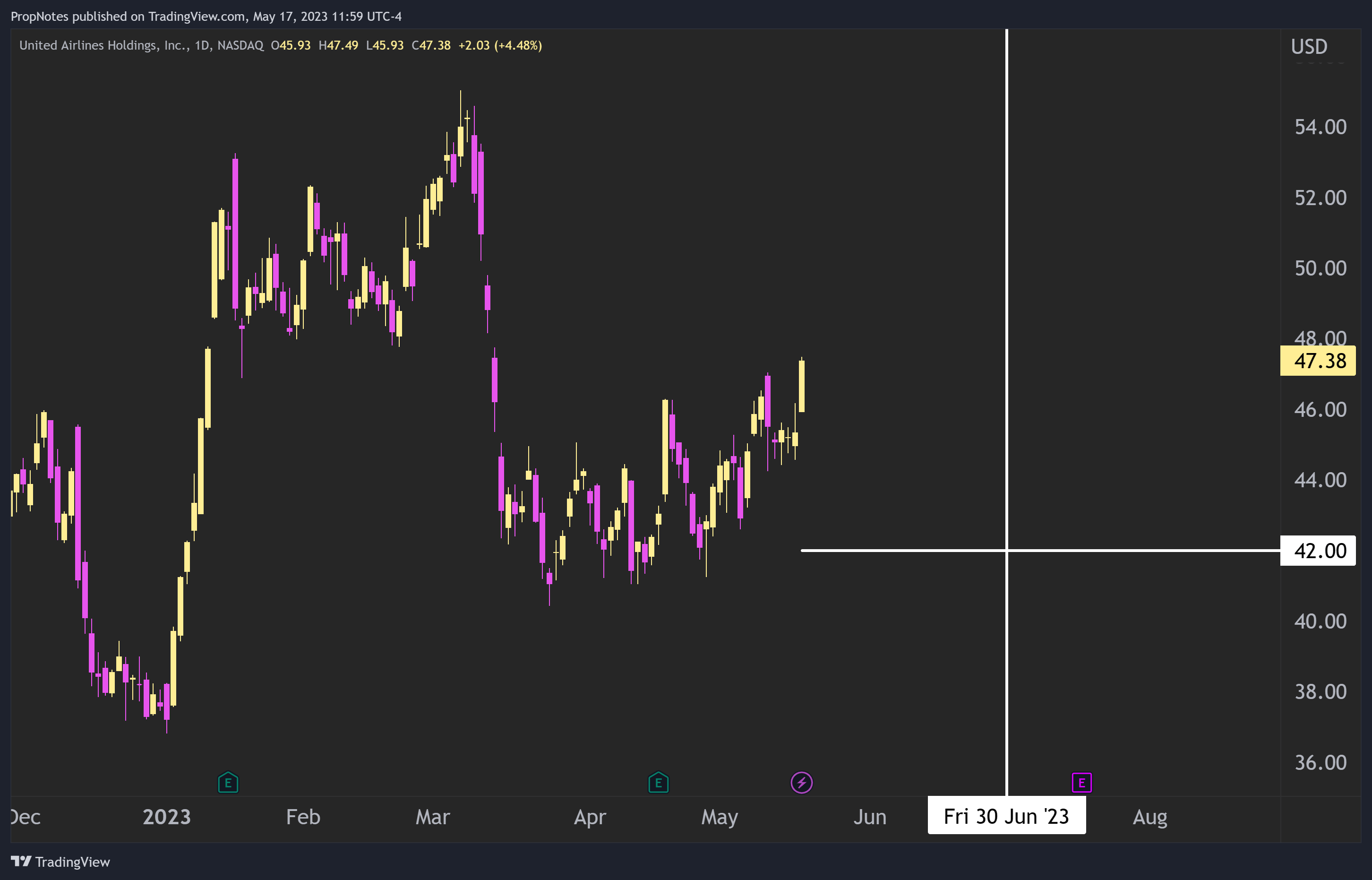

In the case of United, which is currently trading around $47 per share, one might consider selling a put option with a strike price of $42, expiring on June 30th:

Expiration & Strike (TradingView)

Right now, premiums for this option are around $0.76 per share. This means that for every contract you sell, you get $76 in cash immediately. As each contract requires $4,200 in capital to sell, a $76 cash premium earns you 1.84% over the next 44 days, which annualizes to a cool ~15%. This is a great way to generate cash off of United immediately, while still having the opportunity to purchase shares should they drop over the next 6 weeks.

Risks

While the trade idea presents a potential return, there are some risks to think about:

Business Execution: United’s ability to effectively manage its operations and expenses will be crucial in maintaining profitability and growth. Any missteps in these areas could negatively impact the stock price.

Debt: Although United’s debt levels are manageable, any significant deterioration in its financial performance could make servicing debt more challenging and increase the risk of default.

Macro: United is subject to broader macroeconomic risks, including interest rate fluctuations, economic downturns, and changes in government policies that could impact the Airline sector. Downturns could hamper demand, and slow growth.

Commodity-linked: United relies on fuel as a main variable cost of revenue. Volatility in the price of fuel could directly impact the company's profitability and, ultimately, its stock price.

Technical Sentiment: UAL stock is currently overbought according to RSI, which means that it is at a heightened risk of a short to medium term pullback. This could cause option assignment.

Summary

In summary, United Airlines presents a compelling opportunity for investors seeking to capitalize on the benefits of the company’s strong underlying operations and valuation. United’s operational plan, improving financial performance, and adequate liquidity offer a stable platform on which we can sell puts for an attractive yield. If assigned stock, the company presents a great value proposition for long term investors, given the positive characteristics we’ve discussed.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in UAL over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.