Wix.com Q1 Earnings: Upward Revision All Around

Summary

- Wix.com delivers a pleasing Q1 report, where its non-GAAP EPS figure ended at 91 cents compared with negative 72 cents in the same period a year ago.

- Wix.com's outlook for 2023 points to improving free cash flows as the business exits this year.

- Wix.com's share price is down massively from its all time highs, but it's not trading particularly cheaply.

- Looking for a helping hand in the market? Members of Deep Value Returns get exclusive ideas and guidance to navigate any climate. Learn More »

milindri/iStock via Getty Images

Investment Thesis

Wix.com (NASDAQ:WIX) reports fiscal Q1 2023 results that delight investors. Management guides for improvements in outlook from the top of its income statement all the way down to its improving free cash flow margins.

Furthermore, Wix once again reiterated its ambition of reaching the "Rule of 40" in 2025. Presently, Wix's ''Rule of 40'' reaches around 25%. Meaning that Wix has its work cut out in 2024 if indeed it will succeed in making such significant progress in delivering significantly improved free cash flow margins.

Why Wix? Why Now?

Wix is a website development platform for users to create their own websites cheaply. Wix's value proposition is that it can be seen as a cost-effective solution for SMBs who want to create and manage their own websites without having to be proficient coders. Essentially, Wix's product is a low-cost and simple solution for individuals and small businesses.

Part of the appeal to get involved with its shares has to be the fact that Wix's share price is down more than 75% from its all-time highs. Meaning that all the premium that investors had been willing to pay for its stock at one point has now washed out.

That being said, I caution investors into thinking that just because something is down from its highs, it's undervalued. There's a lot of nuance needed, even at this entry point.

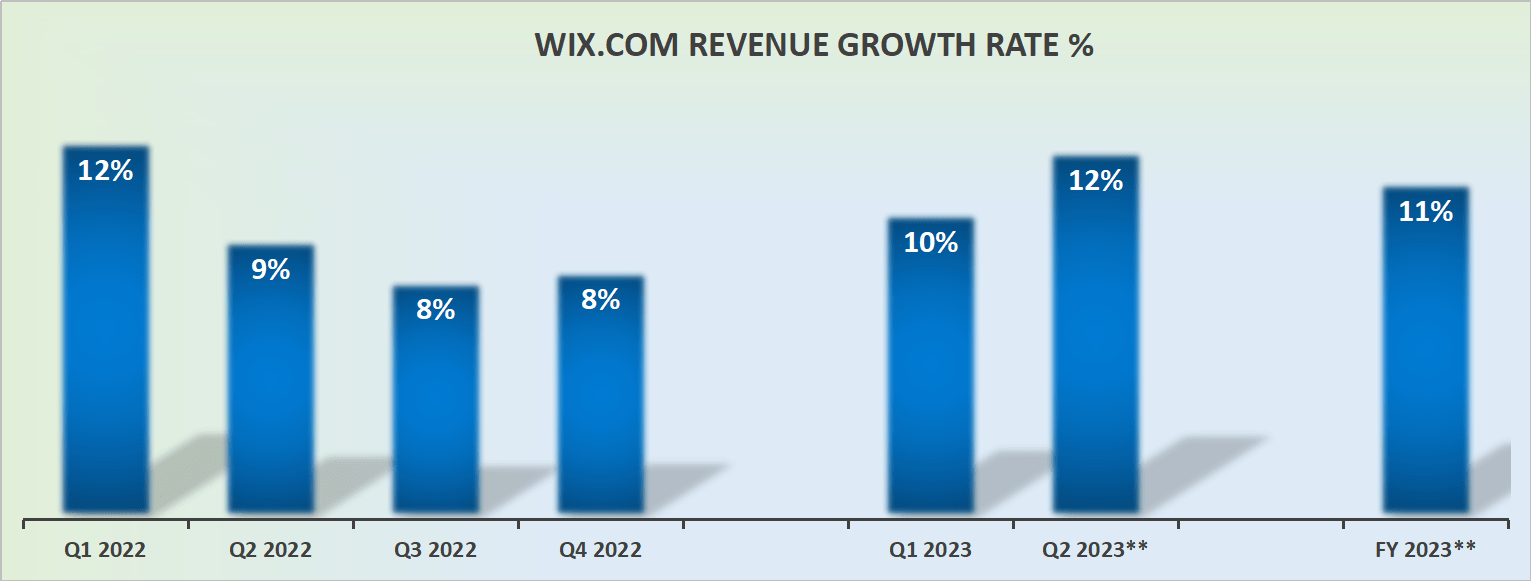

Revenue Growth Rates Are Upwards Revised

WIX revenue growth rates

Wix managed to grow its topline by 10% y/y, which is faster than the high-end of its previous guidance of 9% y/y. What's more, its outlook for the rest of the year was also upwards revised.

Accordingly, analysts were expecting Q2 2023 to see around $378 million in revenues, while Wix now guides for approximately $383 million at the midpoint.

Profitability Profile Set to Improve

Wix believes that in 2023, excluding the capex for its HQ, its free cash flow will reach $180 million. An improvement of 11% compared with the guidance provided in Q4 2022.

But the way investors should think about this is that as Wix exits 2023, it will be growing its free cash flow to around $205 million on an annualized basis.

For the above figure, I've assumed that Q4's revenues reach approximately $400 million and Wix's free cash flow margin is 13%. And then, I've multiplied by 4 this number which brings me to around $205 million per year.

Keep in mind, though, that Wix forecasts its exit rate free cash flow margin to be "more than 13%." So there's some small amount of margin for error baked into my assumptions.

For context, this leaves Wix priced at around 20x forward free cash flows. I don't believe this is a particularly cheap multiple. Particularly as investors know Wix's free cash flow is nearly entirely made up of SBC.

For reference, Wix's free cash flow margin exit rate from 2023 should be ''more than 13%'', while its SBC is expected to account for approximately 14% of total revenues, meaning that there's really no excess cash for shareholders.

Next, let's talk about shareholder returns while keeping this context in mind.

Capital Allocation

Wix has repurchased approximately $7 million worth of shares during the quarter. This figure combined with its repurchased within Q4, brings the total repurchases over the past 2 quarters since its authorization began to $250 million.

Put another way, Wix deployed just over 5% of its market cap toward share repurchases, while bringing down the share count by just under 2% compared with the same period a year ago.

The Bottom Line

Wix today trades for significantly less than it did back in 2019. In fact, unless an investor has been particularly nimble in buying at the bottom prices of this year, I have to wonder whether there's anybody around holding the stock right now that's holding onto any gains from Wix.

When Starboard Value took its position in Wix, there was a lot of hope and excitement that the activist group could find some efficiencies in Wix and improve its free cash flow potential.

For my part, to be frank, I expected even better improvements. But nonetheless, improvements are coming from Wix and I believe that new investors looking at the stock with a fresh pair of eyes will probably be enticed to find some value here.

This article was written by

DEEP VALUE RETURNS: The only Marketplace with real performance. No gimmicks. I provide a hand-holding service. Plus regular stock updates.

We are all working together to compound returns.

WARNING: Any stocks that you feel like buying after discussions with me are your responsibility.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.