National Vision Holdings: Keep An Eye On This One

Summary

- National Vision Holdings has done well for itself in recent years, and that trend looks set to continue as the company opens more stores.

- This value-centric brand is quite healthy, and shares are reasonably priced, though not the cheapest.

- In all, investors should keep an eye on this as a valid prospect moving forward.

- Looking for a helping hand in the market? Members of Crude Value Insights get exclusive ideas and guidance to navigate any climate. Learn More »

LaylaBird/E+ via Getty Images

Some companies can be rather difficult to understand. Others, meanwhile, tell you their story by the name that they operate by. A great example of the latter case involves a firm called National Vision Holdings (NASDAQ:EYE). Both the company's name and its ticker symbol make very clear the fact that the company is dedicated to the eye space. Of course, we do need to dig a bit deeper to understand precisely the segment of the market that it operates in. What we find is one of the largest optical retailers in the U.S. market, with a significant physical footprint and shares that are reasonably priced. At the end of the day, a simple company that can be purchased for a decent price and that operates as an industry leader should be viewed as a ‘buy’ opportunity.

An eye on EYE

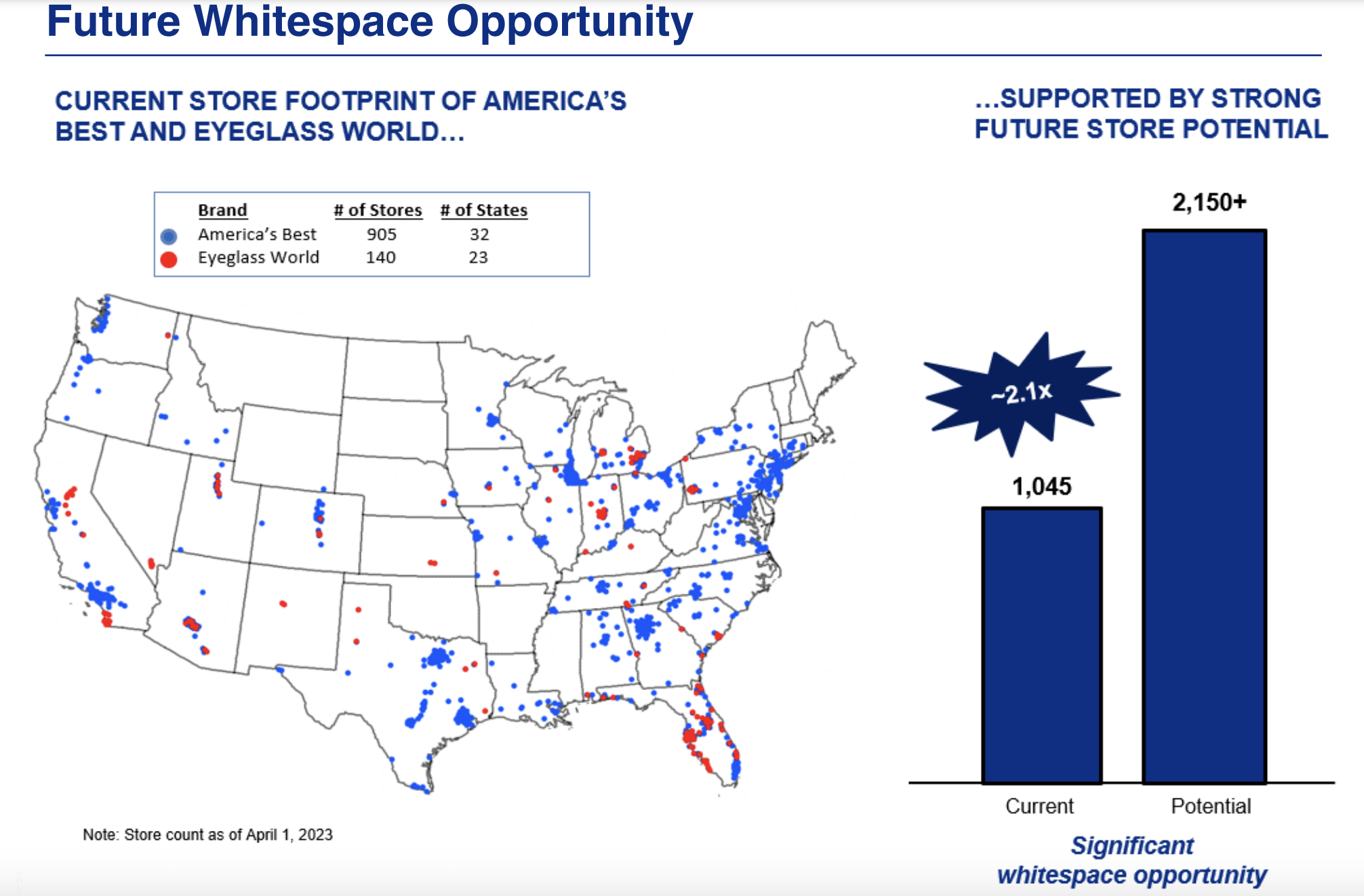

As I mentioned already, National Vision Holdings operates as an optical retailer here at home. In particular, the company seems to focus on the value segment of the industry, catering to budget conscious consumers. Of the 1,045 stores that the company has (excluding in-store partnerships), with 905 under the America’s Best brand name and the remaining 140 under Eyeglass World, the company provides its customers with a variety of goods and services. In particular, the company focuses on what it calls bundled offers. Examples include providing customers with two pairs of eyeglasses plus an eye exam for only $79.95 at its America’s Best locations and for $89 at Eyeglass World. This pricing is substantially lower than many other providers in the industry.

National Vision Holdings

Operationally, the company has two different segments that it runs. The first of these is known as the Owned & Host segment, which includes the two aforementioned brands, as well as its Vista Optical locations in certain Fred Meyer stores and in some military bases. The other segment is the Legacy portion of the company, which involves its management of Vision Centers in certain Walmart (WMT) locations. The company also has FirstSight Vision Services, which operates as a single service health plan under California law and issues individual vision plans throughout the state. On top of the significant store count that the company has, it also boasts 16 different websites that it sells its goods through.

Author - SEC EDGAR Data

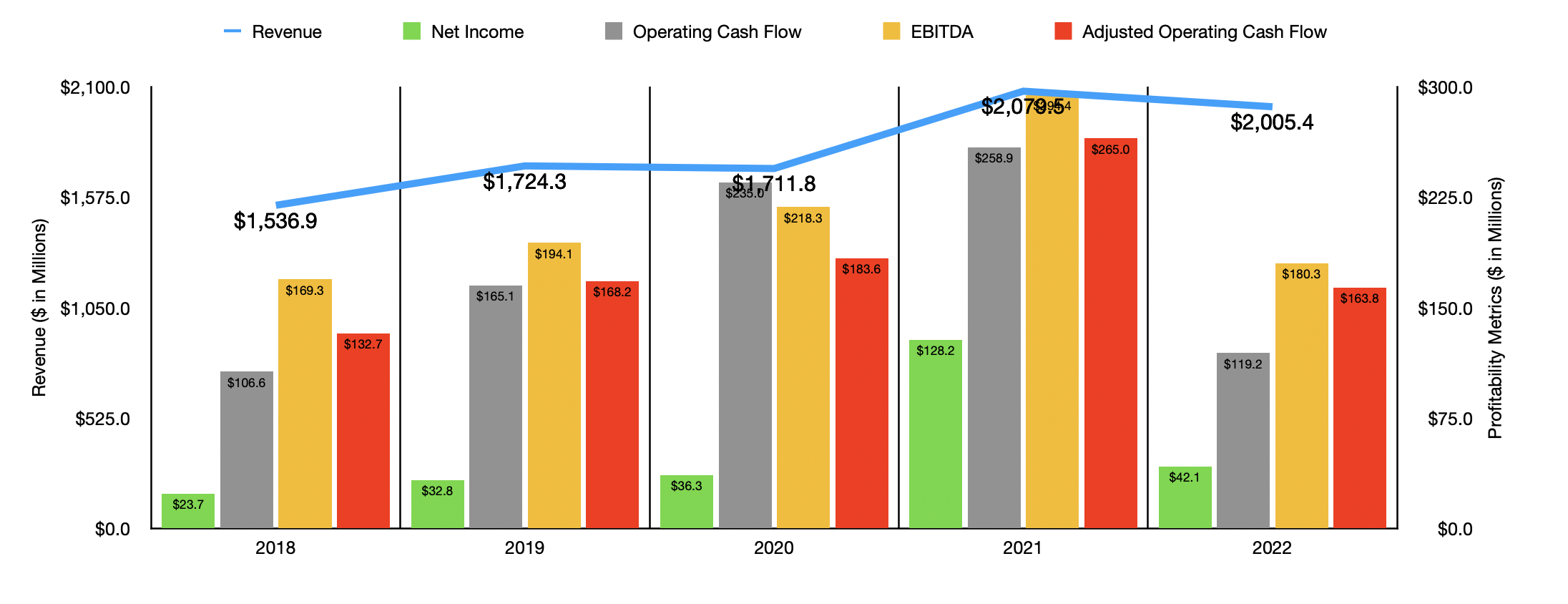

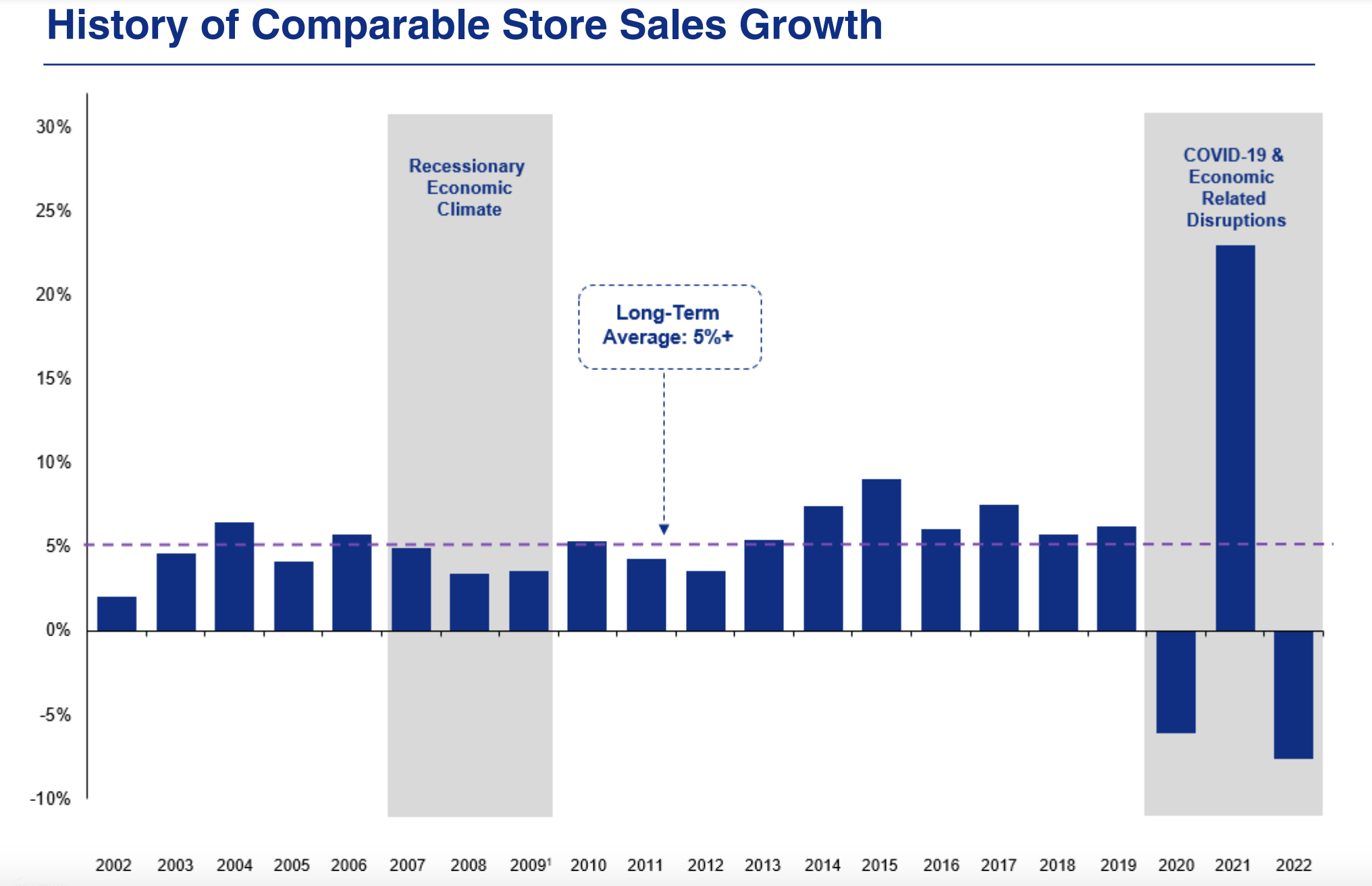

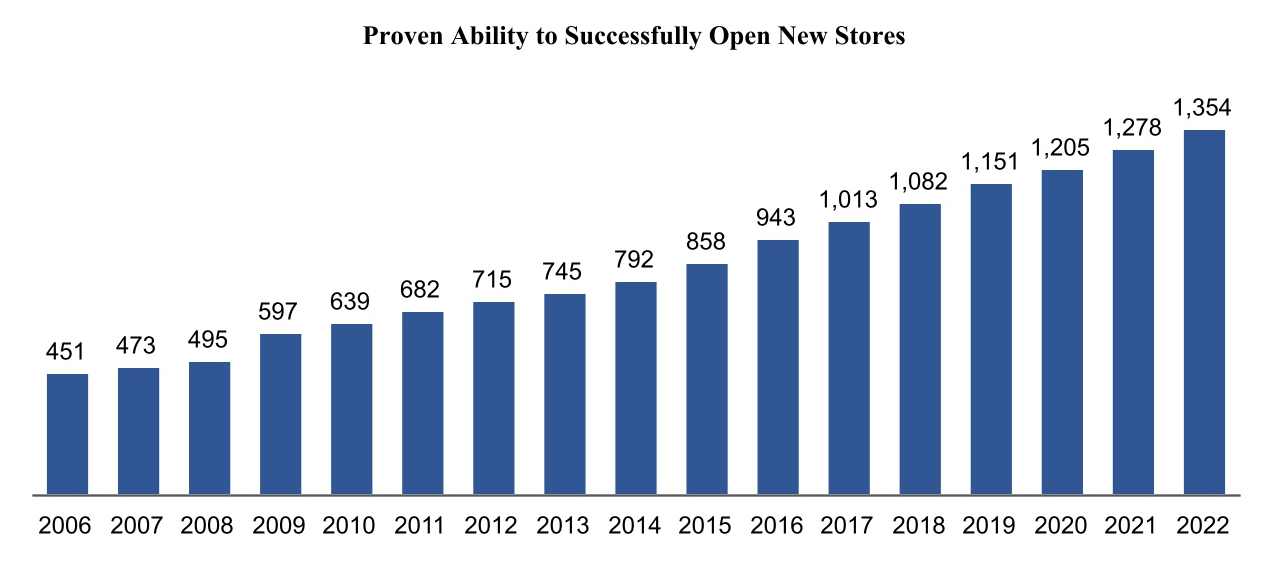

Financially, the company has done quite well for itself in recent years. From 2018 through 2022, revenue with the company expanded from $1.54 billion to $2.01 billion. Interestingly, the COVID-19 pandemic resulted in a spike in comparable store sales during 2021. This strength was sandwiched between negative comparable sales growth in both 2020 and 2022. Obviously, after the pandemic came to an end, pent up demand helped the company out immensely. That's where 2021 was the year in which revenue on record was the highest, totaling $2.08 billion in all. Although comparable sales growth has been volatile over the past few years, the company has been building permanent revenue opportunities for itself. This was accomplished by management being dedicated to continuing opening new stores. In 2018, for instance, the total number of locations the company had across all formats came in at 1,082. By the end of 2022, this number had grown to 1,354.

National Vision Holdings

f

National Vision Holdings

On the bottom line, the picture has been a bit more volatile. But the overall trend has been the same. The general trajectory for net profits, operating cash flow, adjusted operating cash flow, and EBITDA, has all been positive. Because of the strong comparable sales growth in 2021, that was the best year for the company from an earnings and cash flow perspective. And in some respects, the weakening experienced after has set the company back to some degree. 2022 results were actually lower, from a profit and cash flow perspective, than they were in 2019 before the pandemic.

Author - SEC EDGAR Data

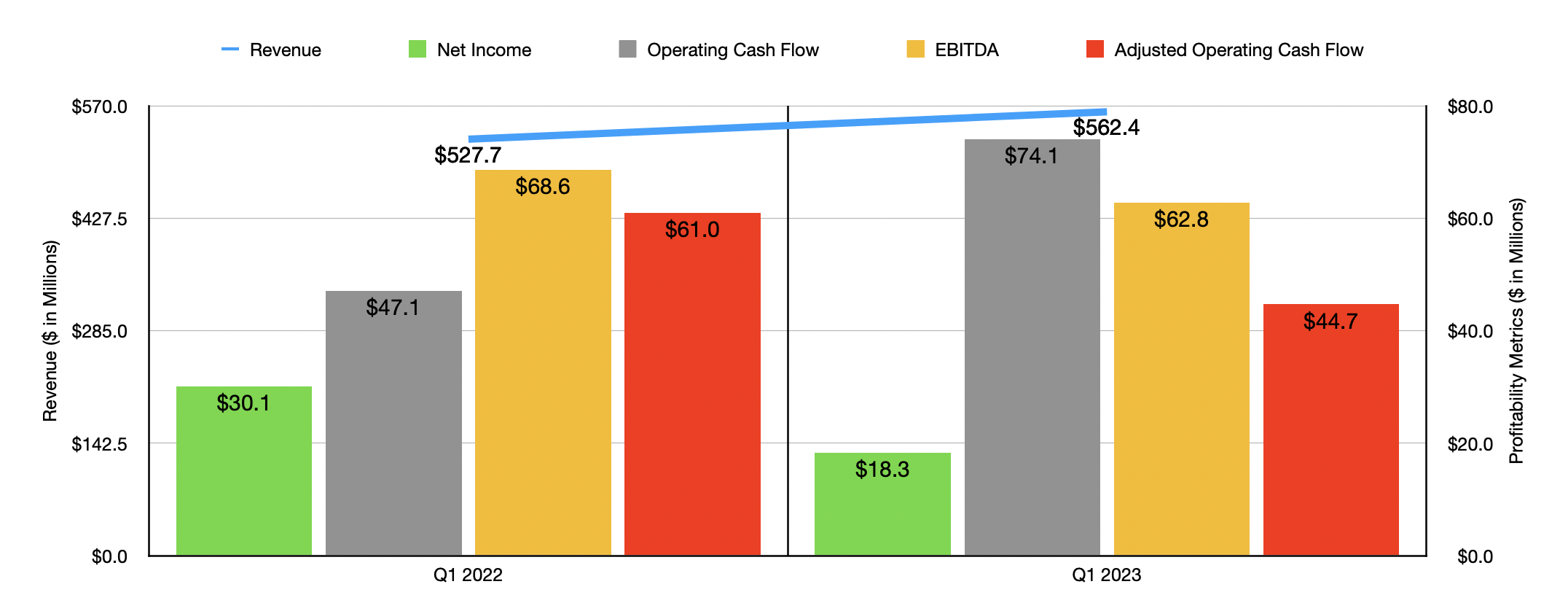

As you can see in the chart above, the company saw some mixed results in early 2023. Revenue of $562.4 million in the first quarter of the year came in higher than the $527.7 million the company reported one year earlier. On the other hand, profits fell from $30.1 million to $18.3 million. A good portion of this increase involved a $9 million swing in net interest expense. But the company also experienced a rise and its cost of revenue from 44.7% of sales to 45.2%. That hit the company's bottom line, from a pre-tax perspective, negatively to the tune of $2.7 million. And the company also saw a rather unfavorable increase in its selling, general, and administrative costs from $228.6 million to $249.9 million. On the cost of sales side, an increase in optometrist related costs was largely to blame. Meanwhile, increased performance-based incentive compensation and higher payroll costs Hit the company's bottom line as well. Other profitability metrics are somewhat mixed. For instance, operating cash flow went from $47.1 million to $74.1 million. But if we adjust for changes in working capital, we would have seen it drop from $61 million to $44.7 million. And finally, EBITDA for the company declined from $68.6 million to $62.8 million.

For the 2023 fiscal year in its entirety, management believes that overall revenue will hit an all-time high if it achieves the midpoint of guidance. That guidance is currently for sales of between $2.08 billion and $2.14 billion. Comparable sales growth should be between 0% and 3%, with the company also benefiting from the opening of between 65 and 70 new stores. Management is currently forecasting earnings per share of between $0.42 and $0.60. At the midpoint, this would translate to net income of $47 million. The other guidance that management provided was actually enough for me to estimate the other profitability metrics as well. Operating cash flow for the company should be around $152 million, while EBITDA should be a bit higher at $172.4 million.

Author - SEC EDGAR Data

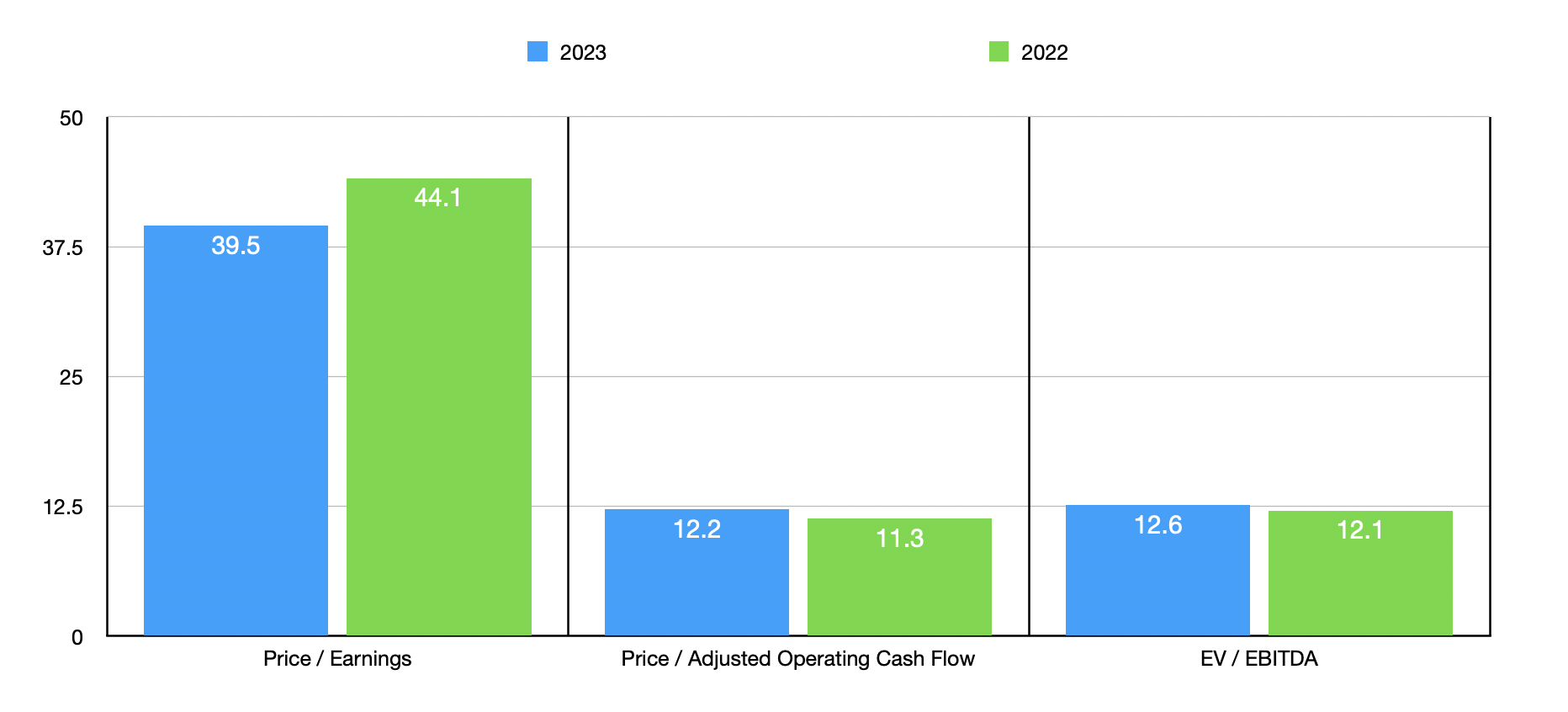

Using these figures, I was able to value the company. In the chart above, you can see the valuation of the firm using both the estimates for 2023 and the actual numbers generated in 2022. With the exception of the price to earnings multiple, which looks rather lofty, the company looks to be fairly reasonably priced. As part of my analysis, I also compared the company to five firms that also play in the vision space. On a price to earnings basis, two of the five were cheaper than National Vision Holdings. And when it comes to both the price to operating cash flow approach and the EV to EBITDA approach, I found that one of the five firms was cheaper.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| National Vision Holdings | 39.5 | 12.2 | 12.6 |

| Alcon (ALC) | 119.3 | 32.5 | 25.1 |

| The Cooper Companies (COO) | 52.0 | 28.1 | 24.2 |

| Bausch + Lomb (BLCO) | 1,193.5 | 22.7 | 16.1 |

| Novartis (NOV) | 31.8 | 14.4 | 13.6 |

| Centene (CNC) | 25.5 | 4.1 | 8.4 |

Takeaway

For those who have an interest in a company with a very niche market that continues to demonstrate attractive growth, both on the top and bottom lines, National Vision Holdings is an interesting prospect to keep in mind. Although the company has faced a bit of volatility recently from a fundamental perspective, the overall trajectory is positive and shares look attractively priced from a cash flow perspective. Given these factors, I have no problem rating the company a ’buy’ to reflect my view that it's likely to outperform the broader market moving forward.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!

This article was written by

Daniel is an avid and active professional investor. He runs Crude Value Insights, a value-oriented newsletter aimed at analyzing the cash flows and assessing the value of companies in the oil and gas space. His primary focus is on finding businesses that are trading at a significant discount to their intrinsic value by employing a combination of Benjamin Graham's investment philosophy and a contrarian approach to the market and the securities therein.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.