Prudential: Declining Investment Portfolio Could Hurt Investors

Summary

- The quarter 1 results provided a relatively glowing picture of Prudential Financial Inc.

- Current data suggests that there will be a continued elevated level of claims.

- Both the company’s investments in bonds and commercial mortgage-backed securities will adversely affect the company going forward.

FangXiaNuo

Preamble

Since January, I've written several articles on our current financial sector malaise. The first, published in February, forecast an imminent banking crisis. Another included an overview of the effect a slump in the value of commercial real estate is having on both the banking sector and the economy in general.

In this piece, an exploration of the impact a decline in the value of Prudential Financial's (NYSE:PRU) portfolio of commercial mortgage-backed securities (CMBS) may have. And there is ample evidence that we are in an environment of declining values of commercial real estate. In other words, Prudential Financial, has the potential to become a major bag holder of CMBS.

If this were not bad enough, the company confirmed that excess claims were continuing to be a headwind for profitability going forward.

The good

Overall, Prudential's Q1 23 financial results and Q2 guidance were pretty decent. Whilst it is true that the adjusted operating EPS of $2.66 was below consensus, it was certainly a strong performance, given the current state of the global economy.

Also impressive was the marked improvement in net income; "Net income attributable to Prudential Financial, Inc. of $1.462 billion or $3.93 per Common share versus net loss of $493 million or $1.33 per share for the year-ago quarter."

In addition, Prudential's management provided a positive outlook for 2Q '23, forecasting around $3.29 per share. It is important to note though that this forecast is dependent on the global economy floating along on a tide of benign circumstances.

Despite net outflows of $14 billion, driven both by retail and institutional investors, assets under management were $1.417 trillion. On the downside, assets under management were down 12.5% ($1.620 trillion) from the previous year, probably due in large part to improved rates investors can achieve with short-term treasuries. Regardless of the drop in these figures, the book value per common share rose from $76.77 to $85.33.

As we all know, when a company pays a dividend, it represents confidence in the future. For Prudential, "dividends paid in the first quarter were $1.25 per Common share, representing a 5% yield on adjusted book value." Furthermore, at the time of writing, this represents a yield of 6.13% at the current share price.

Reading the rather rosy picture described above, you have to wonder why PRU stock has dropped around 20% year to date.

The bad

During the quarterly conference call, Caroline Feeney, Head of US Businesses, stated her belief that high claims due to elevated mortality rates were heading lower; "the overall trend (In mortality) is better than the two previous winters, reinforcing our belief that we will return to pre-pandemic mortality levels in the long term." But, unfortunately, current reports do not, in my view, support this conviction.

Take for example the official statistics for the UK, which show a continued elevated level of mortality above the 5-year average of 12.9%. Now, you may say that is not too bad, until you realise that the average being used is itself elevated due to the high level of mortalities over the last couple of years. In Germany, for the first week of January, mortality was significantly above the average of the previous 4 years; +26%. In fact, at the beginning of January 2023, at least moderate excess mortality was recorded in almost all European countries. And according to data provided by OECD, the USA has a continuing high level of excess mortality for 2023. As an investor, you could be forgiven for thinking that, in regards to claims for deaths, the situation is getting back to normal, given the silence on this matter in the MSM. On a personal note, I find the silence on these continued high numbers for deaths a tad weird given the hysteria that accompanied the pandemic.

During the conference call, Rob Falzon, Vice Chairman, conceded that excess mortality is a continuing drag on profitability; "These results reflect underlying business growth, including the benefits from a higher interest rate environment, offset by lower variable investment and fee income, as well as elevated seasonal mortality experience."

The ugly

Few people fully understand how the money they add to their pension pots enables a modern economy to chug along. One of the ways is through the purchase by pension funds of commercial mortgage-backed securities (CMBS). To begin with, banks make loans to whoever for the purchase or refinancing of properties such as office buildings, malls, and warehousing. Lots of these loans are then bundled together and sold to institutions such as Prudential Financial. Insurance companies are attracted to CMBS because they offer relatively high yields and diversification benefits for their portfolios. Once sold, the banks take the money and make more loans, and so the economy gets the fuel to expand. All good, except if the underlying investments in these CMBS lose value or fail to provide the income expected.

A serious drop in the value of CMBS could have significant effects on Prudential Financial as it has a significant investment portfolio in these instruments. This could lead to a decrease in the company's overall profitability and net worth. Furthermore, a significant decline in the value of CMBS could lead to a credit crunch, making it more difficult for Prudential Financial to issue new loans and investments.

Furthermore, a significant decline in the value of CMBS could also impact Prudential Financial's credit rating. If the company's investment portfolio were to suffer significant losses, its credit rating could be downgraded by rating agencies such as Moody's or S&P. A credit downgrade could make it more expensive for the company to borrow money, as investors may perceive it to be a riskier investment.

The company is a major provider of annuities, which are financial products that provide a guaranteed income stream to the policyholder over their retirement. Annuities are typically invested in a variety of assets, including fixed-income securities such as CMBS. So, even worse for current pensioners, a significant decline in income from these CMBS could conceivably lead to problems with the annuities currently being paid. On a more positive note, Prudential has invested in a range of assets to mitigate this kind of risk so that they can meet their obligations to annuity holders.

Current status of commercial real estate

The commercial real estate market has experienced a decline in property values recently due to a combination of factors. One of the main reasons is the fallout from the COVID-19 pandemic, which has led to many workers opting for a home office. This has caused a decline in demand for office, retail, and industrial space, leading to higher vacancy rates and lower rents. As a result, property owners and investors have seen a decrease in cash flow and profitability.

According to some reports, commercial real estate values are already down 15% versus last year. A rather gloomy report from Morgan Stanley predicts a collapse in values of as much as 40%.

Further evidence comes from Trepp, which claims to be the industry's largest commercially available database of securitized mortgages. In March, the company reported that "The CMBS delinquency rate jumped in February 2023, the second biggest jump since the beginning of COVID-19."

In addition to these sources of evidence, there have been oodles of press reports of borrowers hounding lenders for relief from their mortgage payments or defaulting due to a collapse in demand for space and slumping property values, some of which I have described in a previous article.

Prudential's portfolio of CMBS

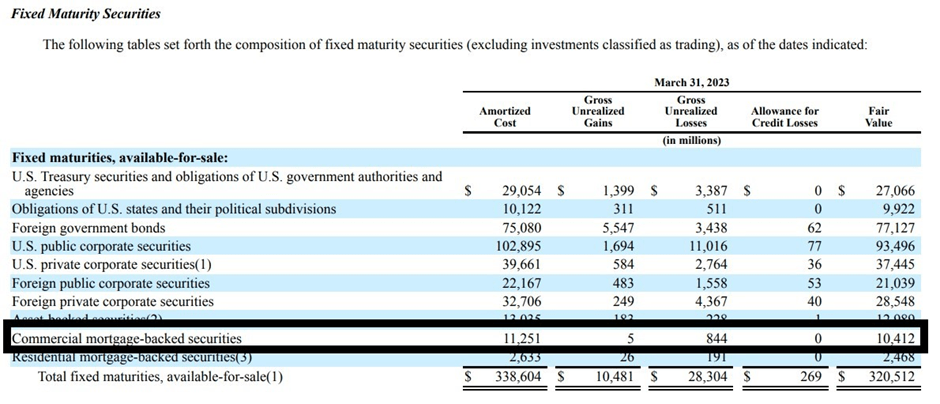

If you take the trouble to review Prudential's Form 10-Q for the quarterly period ended March 31, 2023, you will find the table shown below on page 27. The table shows that despite a record of minimising risk in investments, there has been a drop in value of its portfolio of CMBS of 7.5%. As you may note, all but one of other fixed income instruments have also dropped in value.

Fixed Maturity Securities (Prudential's Form 10-Q)

Whilst it is true that CMBS make up a relatively small proportion of the company's investments, a serious drop of the magnitude predicted by Morgan Stanley will have a serious impact on the company going forward.

Other fixed income securities

On a more upbeat note, US treasuries have not declined significantly, and one can easily believe that the value of these bonds will rise should we move into a new era of interest rate declines. In addition, if interest rates do decline, the rather large holding of foreign government bonds and other bond holdings ought to receive a boost, thus potentially offsetting declines in the value of the CMBS.

To sum up

Regardless of the upbeat quarterly report, the stock price of Prudential Financial has been heading lower, the reasons for which can only be guessed at. However, potentially one reason may be the continuing drag on profits caused by excess claims. In addition, the values of the company's portfolio of CMBS appear to be heading south, and whilst these CMBS holdings make up a relatively small proportion of the company's assets, a further fall is not a positive. Although, if, as appears to be the consensus, the Fed begins to reduce interest rates, the losses for the holdings of CMBS may be offset by gains in the value of other bonds.

As always, this does not constitute advice and investors ought to carry out their own due diligence.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.