LGI: A Worthy Global Fund To Add To Your Portfolio Today

Summary

- Investors today are in desperate need of income due to the rapidly rising cost of living.

- Lazard Global Total Return and Income Fund Inc invests in a portfolio of stocks from around the world to deliver a high level of income to investors.

- The LGI closed-end fund has much more global diversification than most global funds, so it could be a way to increase the diversification of your overall portfolio.

- The CEF recently cut its distribution, but it still yields 7.61% and this appears to be sustainable.

- The fund is trading at a very attractive discount to the net asset value.

- Looking for more investing ideas like this one? Get them exclusively at Energy Profits in Dividends. Learn More »

arsenisspyros

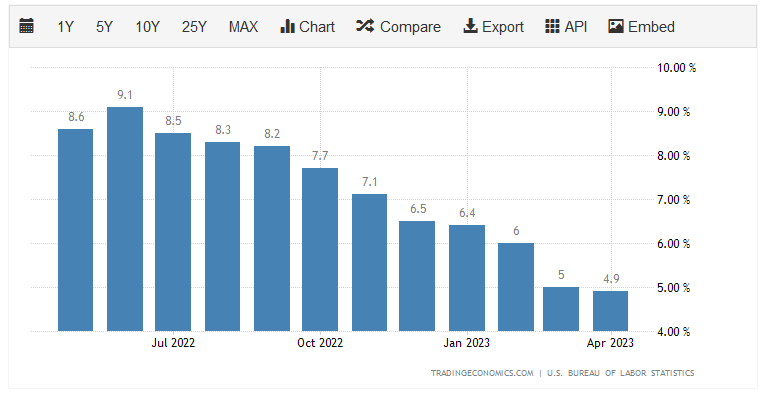

Undoubtedly, one of the biggest problems facing the average American household today has been the incredibly high level of inflation in the economy. This has pushed up the cost of living across the nation, as evidenced by the consumer price index. The consumer price index is an index that measures the price of a basket of goods purchased by the average person on a regular basis. As we can clearly see, this index has increased by at least 6% year-over-year in ten of the past twelve months:

Trading Economics

Although we have seen the rate of inflation come down in the past few months, this is mostly driven by a decline in crude oil and natural gas prices. It is also still well above the level that policymakers really want to see, and it is high enough to be severely impacting many households in a negative way. As I have pointed out in recent blog posts (see here), Americans have been resorting to borrowing money against their credit cards and spending down their savings just to make ends meet. This is certainly not the kind of environment that is conducive to or indicative of a strong economy. The main takeaway here though is that Americans are clearly desperate for additional sources of income just to maintain their standard of living. Many people have already taken on second jobs or entered the gig economy in pursuit of this goal.

As investors, we are certainly not immune to this. After all, we have bills to pay and require food for sustenance. We do have some extra options in how we can obtain more income though, since we are able to put our money to work for us in pursuit of this task. One of the best ways to accomplish this is by purchasing shares of a closed-end fund, or CEF, that invests its money in a way that results in a high level of income for shareholders. Unfortunately, these funds are somewhat underfollowed by the financial media and most financial planners are unfamiliar with them, so it is not always easy to get the information that we would like to make an informed investment choice. This is a shame because these funds offer a number of advantages over open-ended or exchange-traded funds. In particular, they are able to employ certain strategies that allow them to deliver a higher yield than just about anything else in the market. As yield is the most important thing for investors looking for income, it is easy to see why this is a real advantage for these funds.

In this article, we will discuss the Lazard Global Total Return and Income Fund Inc (NYSE:LGI), which currently boasts a respectable 7.61% yield. This is admittedly not the highest yield available among closed-end funds, but it is still high enough to provide a nice level of income and it is not so high that it indicates market fear surrounding it. I have discussed this fund before, but several months have passed since then so obviously a great many things have changed. This article will therefore focus specifically on these changes, as was as provide an updated analysis of the fund’s financial performance.

About The Fund

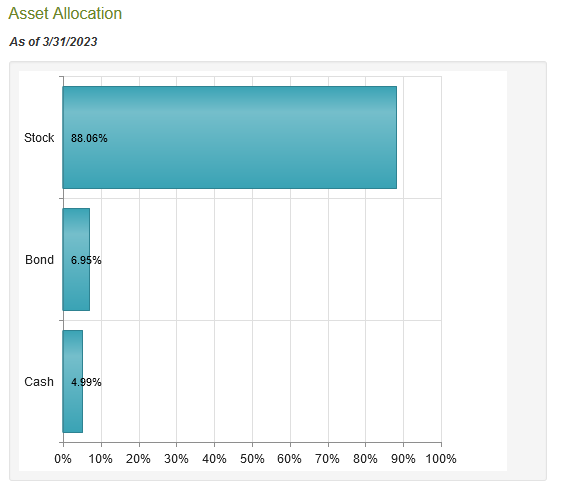

According to the fund’s webpage, the Lazard Global Total Return and Income Fund has the stated objective of providing its investors with a high level of total return. This is not particularly surprising given the fund’s name, and admittedly this is a very similar objective to that of many other closed-end funds. As the name of the fund suggests, it aims to deliver this objective through a combination of capital appreciation and current income. This is the reason why most investors purchase common equities, as these securities are known for both capital gains and income in the form of dividends. This fund is no exception to this, and as might be expected its portfolio consists mostly of common equity:

CEF Connect

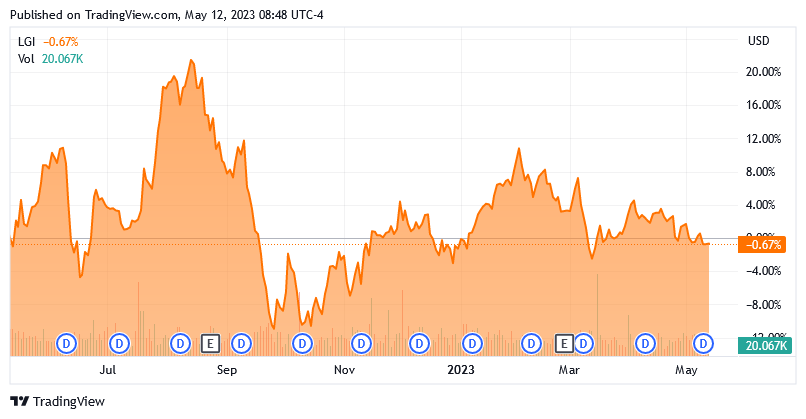

We can also see some bond holdings and cash in the portfolio, but these assets only account for 11.94% of the fund. That is normally not enough to affect the fund’s overall strategy, although it may reduce its volatility slightly compared to an all-common stock portfolio. This is particularly true considering that the problems that have been facing the bond market over the past year are probably over, which I discussed in a recent article. This is something that will probably appeal to risk-averse investors, although closed-end funds usually do not fluctuate very much in the market in terms of price. We can certainly see that in this fund, as it has been almost perfectly flat over the past year:

Seeking Alpha

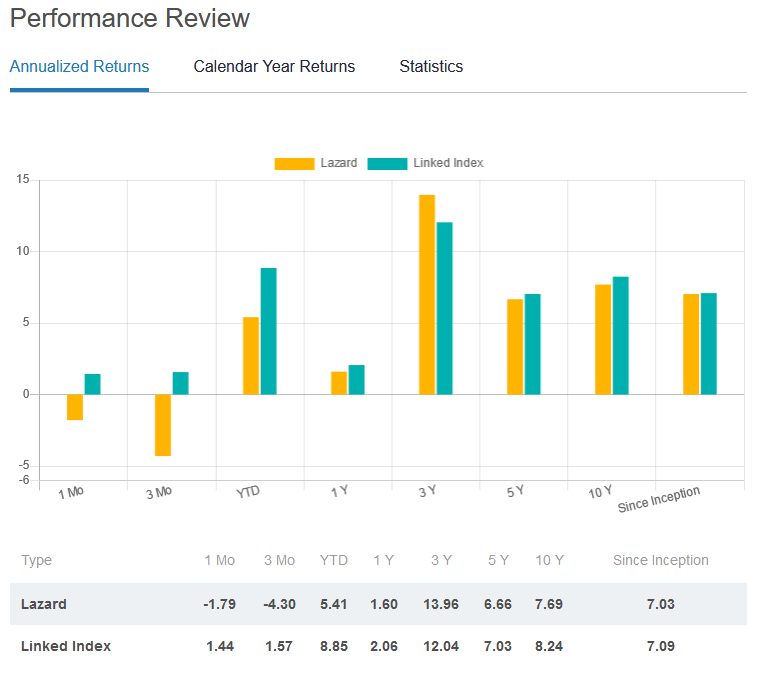

This does not, of course, mean that investors have not received any return over the period. This is because the fund was paying out distributions for the entire period. In fact, it is the usual strategy for a closed-end fund to try and maintain a relatively stable market price and portfolio size and pay out all of its investment profits to investors. This is why we need to look at the total return delivered by a fund, not just its market price performance. This is especially important as many investors use the fund’s distributions to purchase more shares of the fund and thus see quite different results than just the share price would indicate. The fund delivered a 1.60% total return over the past year, which admittedly is not impressive, but it is still better than the losses that numerous other funds delivered over the same period:

Lazard

It is somewhat unfortunate that the Lazard Global Total Return and Income Fund failed to beat its benchmark index during most periods of time, but this is not exactly unusual. In fact, actively managed funds usually fail to beat their benchmark indices, due mostly to various fees. It is actually not very difficult to beat the S&P 500 Index (SP500), but most managers cannot beat it by enough to cover their fees and still have enough left over to provide the investors with excess returns. The fact that this fund managed to get as close as it did over its entire lifetime is quite impressive. It is worth noting though that the S&P 500 Index has delivered an average annual return of 11.88% since its creation in 1957, so it actually beat both this fund and its benchmark index over the long term.

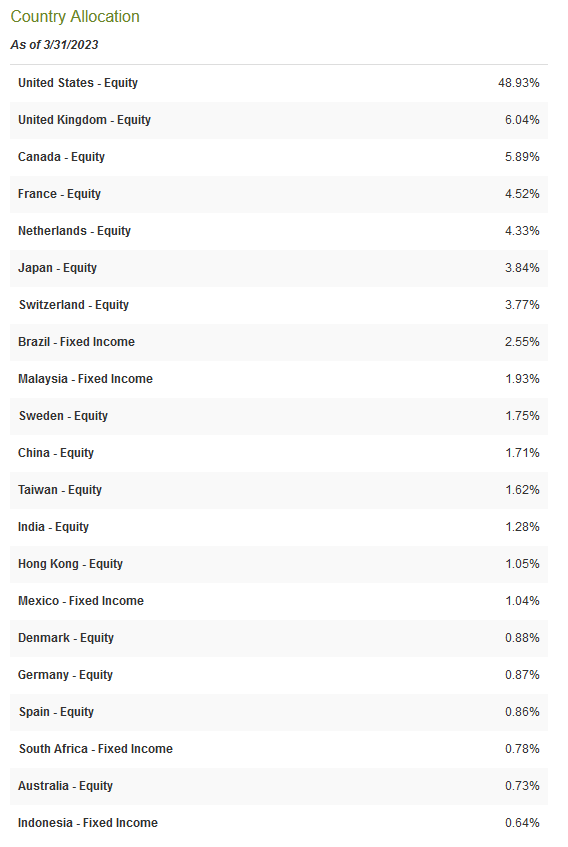

This fund is not exactly trying to deliver returns on par with the S&P 500 Index though, as that is a purely American index. As the name of this fund implies, the Lazard Global Total Return and Income Fund is a global fund that invests in securities issued by nations all over the world. As of March 31, 2023, only 48.93% of the fund is invested in American stocks:

CEF Connect

This is a lower percentage than we typically see in global funds. As I have pointed out numerous times in the past, most global funds have 60% to 70% of their assets invested in the United States despite the fact that the United States accounts for less than a quarter of the global gross domestic product. This fund has somewhat less exposure than that, although it is admittedly over-weighted to this nation based on its actual contribution to global economic output. As this fund is somewhat less allocated to the United States than most funds, it could actually help an American investor reduce their domestic exposure if it is included in a portfolio that contains other funds. This is important because of the protection that it provides against regime risk. Regime risk is the risk that some government or other authority will take some action that has an adverse impact on a company in which we are invested. The only realistic way to protect ourselves against this is to ensure that only a relatively small proportion of our assets are invested in any given country. This fund appears to be one way to help us accomplish this, particularly if an investor is overly exposed to the United States.

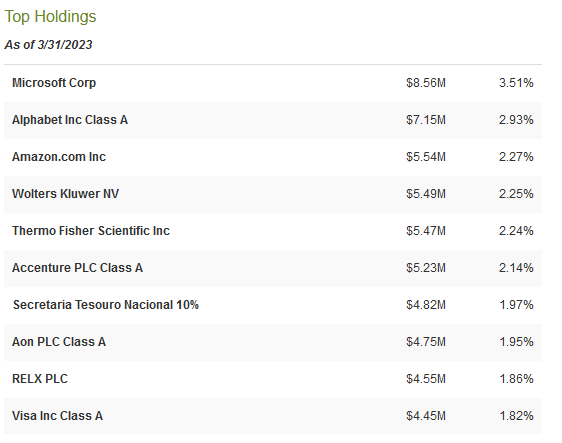

We can see some of the fund’s international exposure by looking at the largest positions in the fund. Here they are:

CEF Connect

Wolters Kluwer N.V. (OTCPK:WOLTF), Accenture plc (ACN), Aon plc (AON), and RELX PLC (RELX) are all non-American companies. The Secretaria Tesouro Nacional position is Brazilian government debt, so obviously that is foreign as well. Thus, fully half of the fund’s largest positions are non-American. This is more than even most other global closed-end funds possess, which reinforces the fact that this is a global fund. In addition, I cannot think of any other closed-end fund that has any of the foreign companies shown above listed among its largest positions, so this fund may help reduce an investor’s concentration risk as well. Concentration risk, as I have explained in previous articles, is caused by the fact that most funds hold the same positions so anyone that invests in multiple funds will usually be much less diversified than they think they are. This is especially true with American funds as nearly all of them have outsized positions to the major technology companies.

There have been two significant changes to the fund’s largest positions list over the past six months. These are that Johnson & Johnson (JNJ) and Dollar General (DG) were both removed and replaced with RELX and Visa Inc. (V). This change actually decreased the fund’s American exposure over the period, which is rather nice to see as the American market appears to be overvalued. It also reduces our regime risk somewhat, which is also nice. The fact that so few changes have been made to the fund over the past six months might lead us to believe that this fund has a fairly low turnover. This is certainly true as its 15.00% annual turnover is very low for an equity closed-end fund. The reason that this is important is that it costs money to trade stocks or other assets, which are billed directly to the fund’s shareholders. This naturally creates a drag on the fund’s performance and makes management’s job more difficult because the portfolio needs to earn sufficient excess returns to cover these extra costs.

As was explained earlier in this article, there are very few fund managers that are able to accomplish this on a consistent basis, which usually results in these funds underperforming their benchmark indices. As we have already seen, this one has struggled to beat its benchmark over time, although it has not underperformed very much over the long term.

Leverage

In this introduction to this article, I stated that closed-end funds such as the Lazard Global Total Return and Income Fund have the ability to employ certain strategies that can boost their yields well beyond that of any of the underlying assets or just about anything else in the market. One of these strategies is the use of leverage. In short, the fund borrows money and then uses those borrowed funds to purchase stocks and other assets. As long as the total return of the purchased securities is greater than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for that reason. Fortunately, this fund easily meets that requirement as its levered assets only comprise 11.04% of its assets as of the time of writing. Thus, the fund appears to be striking a reasonable balance between risk and reward.

Distribution Analysis

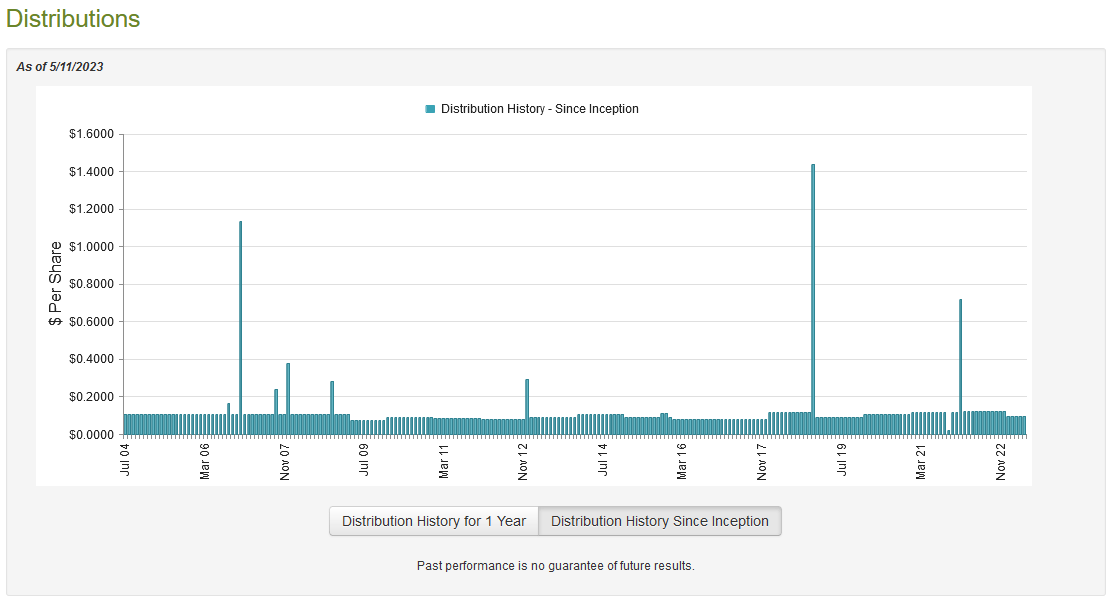

As was stated a few times over the course of this article, one of the major attractions to closed-end funds is the remarkably high yields that these entities pay out. The Lazard Global Total Return and Income Fund Inc invests in a portfolio primarily consisting of common stocks issued by companies all over the world, applies a layer of leverage to boost its returns, and then pays out the profits to investors via a distribution. This could be expected to result in a high yield, which is certainly the case. The fund currently pays a monthly distribution of $0.0934 per share ($1.1208 per share annually), which gives it a 7.61% yield at the current price. The fund has unfortunately not been very consistent with this distribution over the years, and it has varied quite a bit over time:

CEF Connect

The fact that the fund’s distribution has varied so much over time could prove to be a bit of a turn-off for those investors that are seeking a stable and secure source of income to use to pay their bills or finance their lifestyles. However, usually, when we see this sort of variation, it is caused by the fund changing its distribution in response to the performance of the portfolio. This is done so that the fund does not end up drawing down its portfolio just to pay its distributions, which is a good thing for the long-term viability of the fund. We can see this evidenced by the fund’s distribution cut back in January, which immediately followed one of the most challenging markets in years. It still is rather annoying for investors, though. However, anyone buying the fund today will receive the current distribution at the current yield and does not have to worry about the fund’s past performance. Thus, the most important thing is the fund’s ability to sustain its current distribution going forward.

Fortunately, we have a relatively recent document that we can review for our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, it will not include data from the past few months, but it will give us a good idea of how well the fund performed in the challenging conditions of 2022 and the events that caused the fund’s distribution to be cut in January. As such, it should work pretty well for our analysis. During the full-year period, the Lazard Global Total Return and Income Fund Inc received $3,208,436 in dividends and $1,717,112 in interest from the assets in its portfolio. This gives the fund a total investment income of $4,925,548 for the full-year period. It paid its expenses out of this amount, which left it with $682,948 available for shareholders. As might be expected, this was nowhere close to enough to cover the $19,473,977 that the fund actually paid out in distributions during the year. At first glance, this is likely to be quite concerning as the fund’s net investment income was nowhere close to enough to cover its distributions. This alone is not as big of a problem for equity funds as it is for fixed-income funds, however.

This is because an equity fund like this one has other means through which it can obtain the money that it needs to pay out its distribution. For example, it might have capital gains that can be distributed to the shareholders. As can probably be expected by anyone that watched the market last year, the fund did generally fail at this task. It did not do that poorly, however, as it did manage to have net realized gains of $17,644,540 over the period. These gains were more than offset by $68,743,310 net unrealized losses, though.

Overall, the Lazard Global Total Return and Income Fund Inc’s assets declined by $69,834,088 after accounting for all inflows and outflows over the period. This is certainly concerning, however, its net realized gains and net investment combined totaled $18,327,488, which was very close to the total amount that it paid out in distributions. If it can deliver a similar performance in 2023 to that of 2022, it should not have any real trouble paying out the smaller distribution that it now has. As the market has been surprisingly strong year-to-date, it can probably accomplish this task. Thus, the distribution is probably reasonably safe.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Lazard Global Total Return and Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of May 11, 2023 (the most recent date for which data is available as of the time of writing), the Lazard Global Total Return Fund had a net asset value of $16.83 per share but the shares currently trade for $14.77 each. This gives the shares a 12.24% discount to net asset value at the current price. This is a reasonably attractive price to pay for the fund’s shares, and it is better than the 11.83% discount that the shares have had on average over the past month. Overall, the price appears to be very reasonable today.

Conclusion

In conclusion, the Lazard Global Total Return and Income Fund Inc is one closed-end fund that investors can use to earn an income from their portfolios today. The fund is a common equity fund, so it comes with all the inherent advantages of investing in common equity but the returns from its portfolio can be easily used as income or reinvested. The fund also has lower American exposure than most global funds, so it can help an investor achieve appropriate international diversification. The current Lazard Global Total Return and Income Fund Inc distribution appears to be sustainable, barring a market collapse, and the fund is trading at a very attractive valuation. Overall, Lazard Global Total Return and Income Fund may be worth considering today.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

At Energy Profits in Dividends, we seek to generate a 7%+ income yield by investing in a portfolio of energy stocks while minimizing our risk of principal loss. By subscribing, you will get access to our best ideas earlier than they are released to the general public (and many of them are not released at all) as well as far more in-depth research than we make available to everybody. In addition, all subscribers can read any of my work without a subscription to Seeking Alpha Premium!

We are currently offering a two-week free trial for the service, so check us out!

This article was written by

Traditionally, we have not always responded to comments but in order to improve the quality of our research, comments will be reviewed and we will respond to issues regarding errors or omissions. This does not include our premium service, "Energy Profits In Dividends" which is available from the Seeking Alpha Marketplace. This service does include detailed discussions with our team both on the reports themselves and in a private forum.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.