Maersk: We Do Not Share Management's Optimism For Second-Half 2023

Summary

- A.P. Møller - Mærsk A/S delivered 66% lower net profit in Q1.

- The company's very solid balance sheet and continued profitability should help them weather the downturn in the market.

- We believe that the dividend yield of 35% will drop and that there is still a high risk of further decline in the share price.

Rixipix

Maersk logo (A P Moeller Maersk)

Investment Thesis

In our previous analysis of the 1st of March this year on A.P. Møller - Mærsk A/S (OTCPK:AMKBY), (OTCPK:AMKBF) we decided to start our coverage of AMKBY with a Sell stance.

We do not share management's belief that the downturn in freight rates was only caused by buyers destocking their inventory.

The world's largest container shipper has just published their results for the first quarter, so we want to share with our readers our thoughts and see if we need to make changes to our stance.

First Quarter 2023 Financial Results

We noted from the 1st quarter financial results that the volume of containers shipped declined in Q1 by 9.4% year-on-year. The average freight rate was also down from $4,553 per FFU to $ 2,871 per FFU in Q1, which was a drop of 36.9%.

Consolidated revenue for the quarter was $14.21 billion as opposed to $19.289 billion in Q1 of 2022. The EBIDTA was $3.97 billion compared to $9.08 billion a year ago.

Net profit declined by 66% from $6.81 billion in Q1 of 2022 to $2.32 in Q1 of 2023. However, their free cash flow was a solid $4.22 billion last quarter.

EPS was $131 down from $364.

This steep decline in earnings does not bode well.

On a more positive note, AMKBY does have an excellent balance sheet. With a gross total debt of $15.28 billion and total cash of $22.28 billion, the net debt is negative $7 billion.

The dividend paid out was $9.4 billion for the year and they have also continued to buy back shares with purchases worth $718 million in the first quarter.

AMKBY is an ADR that represents 1/200th of one ordinary share in A.P. Møller - Mærsk A/S. They pay an annual dividend. The last dividend on the ADR was $3.1386 which was paid out on the 17th of April. Based on the latest share price of $8.88 the TTM yield is a whopping 35%.

Our thesis is based on lower earnings and cash generation going forward.

How much is dependent on so many factors. Therefore, it is hard to predict exactly how much dividend they will be able to distribute. However, we are certain that it will be lower. With a 35% yield, it is "normal" to expect and accept dividend cuts. It is impossible to say, with any certainty, how big those cuts will be.

Management of AMKBY is still optimistic and has guided investors during the Q1 presentation that they expect volume to gradually start to pick up by 2H of 2023, as they believe that inventory correction will be completed by then. They also foresee that the global GDP growth should grow in a range of -2.5% to +0.5%.

Risks and Final Thoughts

We are of the opinion that their guidance is too optimistic.

When we look at China's decline in export over the last few months, it is clear to us that with the effect of inflation and particularly higher interest rates, consumers have less disposable income available for the purchase of consumer products. The rate of acceleration in the Fed's hikes in interest rates is the highest in recent history, which means that consumers have had little time to adjust to these changes.

China's new export orders fell in April from 50.4 to 47.6, which is the lowest in three months. That affects the demand side.

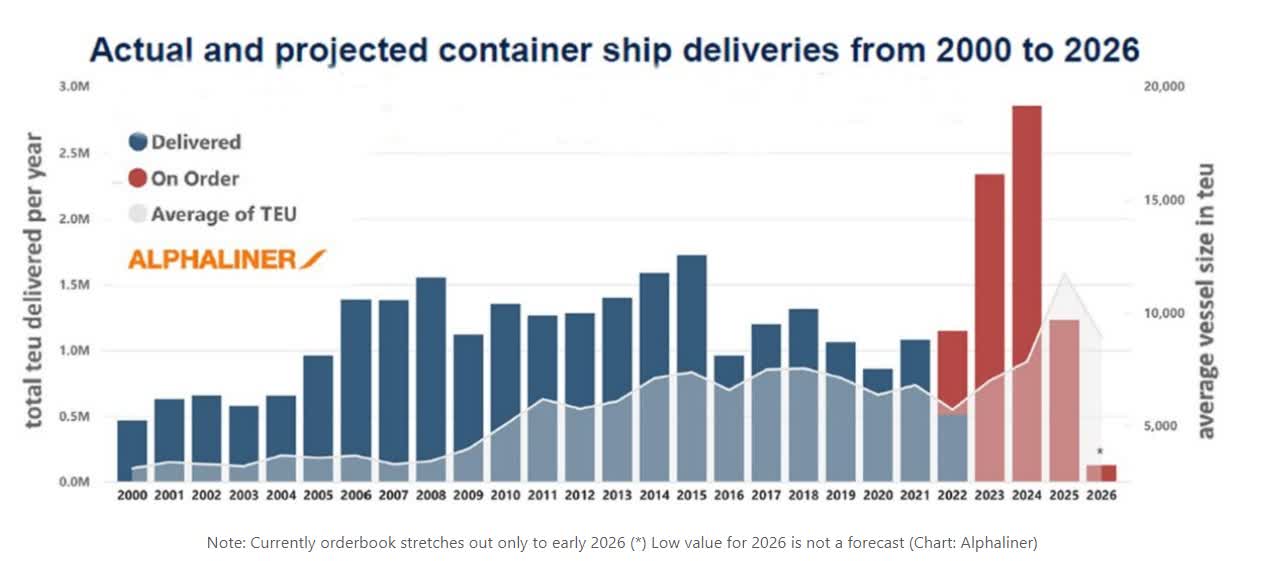

We are also of the opinion that we have not yet seen the full effect of all the containership newbuilding deliveries. Here is the status as of October 2022;

Containerships order book as of October 2022 (Alphaliner)

Since then, ship owners are still ordering many new large container vessels. According to an article in Tradewinds last month, ship owners were in discussions to order another 40 large container ships.

History tells us that this will put further pressure on the pricing power of all the liner companies. It takes time to absorb so many new vessels.

The liner companies are trying to mitigate the damage by reducing the speed of the vessels. This helps them save fuel and fill up each vessel with more boxes, but on the other hand, the earnings per day per voyage decrease as each voyage takes a longer time which means they have to pay more in charter payments.

All in all, we are of the opinion that the earnings will get worse, and not better, in the second half of 2023.

Although the past dividend yield is very tempting, investors should focus on the return OF investment rather than ON the investment.

Since our Sell stance in early March, the share price has dropped 27%.

AMKBY - share price development (SA)

The number 8 when spoken in Cantonese means prosperity. With triple 8, that number is a very auspicious one for Chinese people all over the world.

Regardless of that, we continue our Sell stance for now. Should our thesis continue to be right, a dividend cut will come next year. The share price will in all likelihood drop even before a potential cut takes place if we see weak earnings in the next two to three quarters.

We will be watching data coming out from China on their export in the coming month and also be tracking the development of the freight market per container. If we see not just one month but 3 - 5 months of improvements we might upgrade AMKBY.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.