PFFD: Beware Financials Exposure

Summary

- PFFD provides exposure to a broad index of preferred securities.

- PFFD has 71% exposure to financial preferreds.

- With the ongoing regional banking crisis, financial preferreds will continue to come under pressure.

- Until a comprehensive solution is found to the banking crisis, I suggest investors avoid the PFFD ETF.

Sohel_Parvez_Haque

A few months ago, I wrote a cautious article on the Global X U.S. Preferred ETF (NYSEARCA:PFFD), arguing it was not the time to own the PFFD ETF, as interest rates were still rising and PFFD had high duration risk.

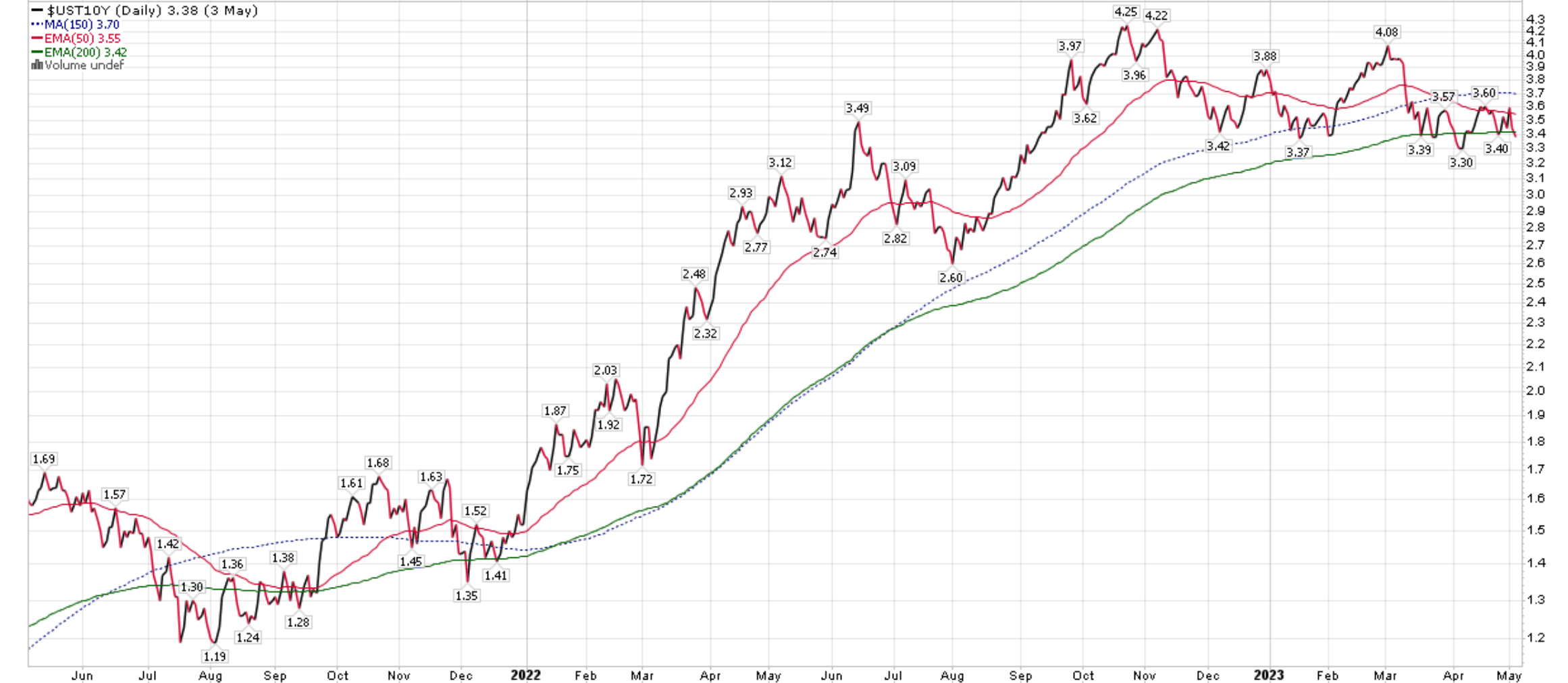

Fast forward a few months, long term interest rates appear to have peaked, with the 10Yr treasury yield now sub-3.5% (Figure 1).

Figure 1 - 10Yr yields appear to have peaked (Stockcharts.com)

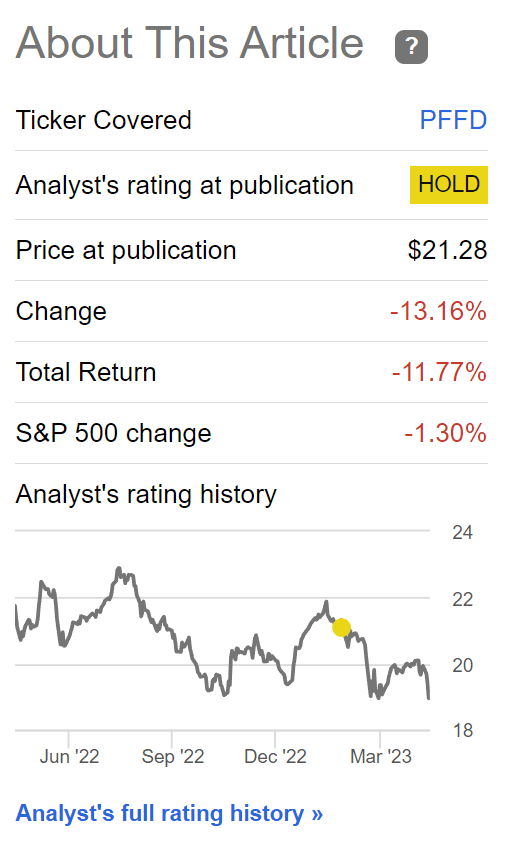

However, that has not helped the share price of the PFFD ETF, as it has declined by 12% since my article (Figure 2).

Figure 2 - PFFD has declined by 12% in total returns (Seeking Alpha)

What happened and is now a good time to buy PFFD based on my prior analysis?

PFFD Dragged Down By Financials Exposure

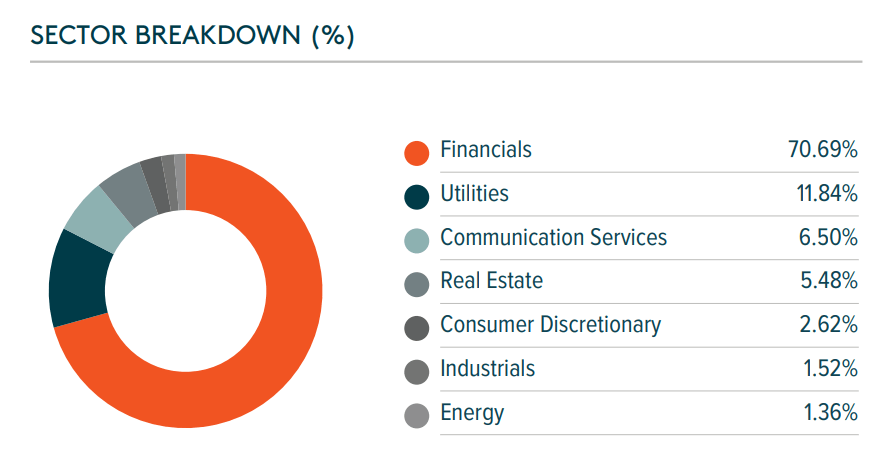

In my opinion, PFFD's performance has been negatively impacted by its outsized exposure in the Financials sector, which accounted for 70.7% of the fund's net investments as of March 31, 2023 (Figure 3).

Figure 3 - PFFD has large financials exposure (PFFD factsheet)

Since I wrote my prior article, we have seen a U.S. regional banking crisis that was sparked by the sudden collapse of SVB Financial in March.

Regional Banking Crisis In A Nutshell

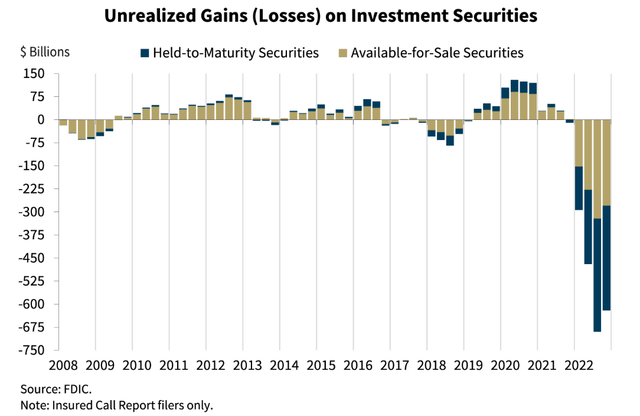

In a nutshell, the Federal Reserve's 500 bps of interest rate increases in the past year have caused enormous unrealized losses on the balance sheet of regional banks. According to the FDIC, U.S. commercial banks had a collective $620 billion in unrealized securities losses on their balance sheet as of December 31, 2023 (Figure 4).

Figure 4 - FDIC-regulated banks have $620 billion in unrealized losses on investment securities (FDIC)

Normally, banks can try to earn their way out of the hole, if the securities were 'held to maturity'. In fact, the regulators specifically allow banks to do this by classifying these securities as 'Available For Sale' and 'Held To Maturity', thus the unrealized losses bypassed banks' income statement.

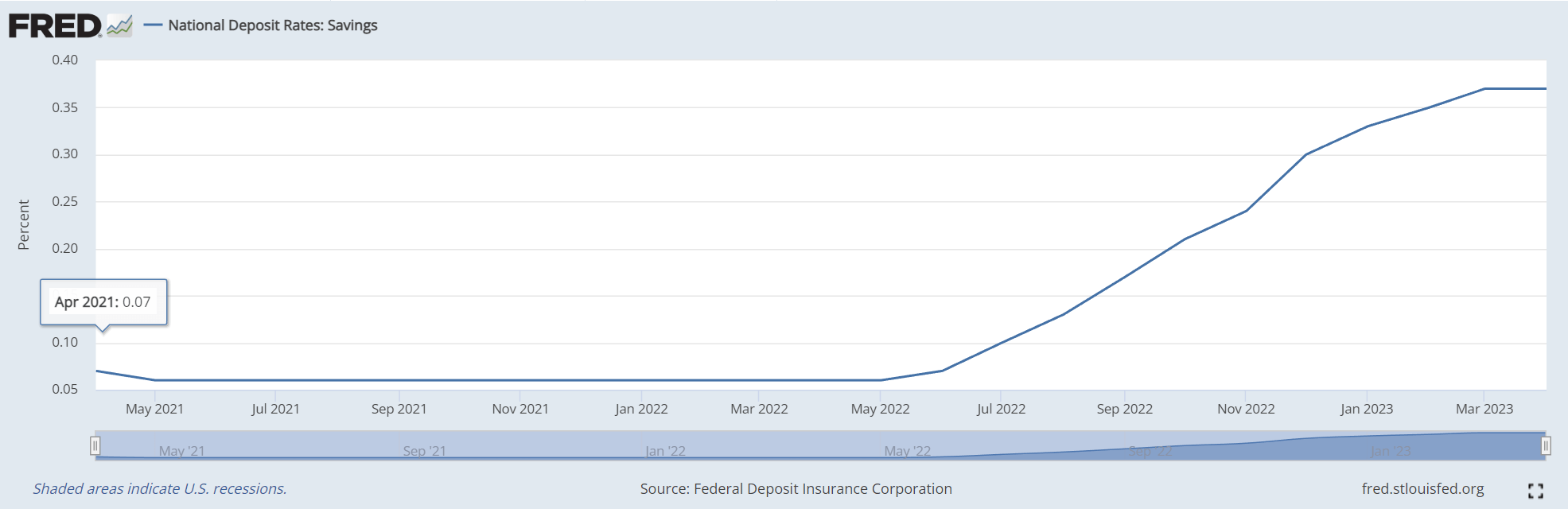

However, another problem created by the Fed's interest rate hikes was that it boosted the yields on money market funds ("MMF") to levels far above banks' savings deposit rates. For example, while MMF yields are now north of 4%, average savings deposit rates are still at 37 bps (Figure 5).

Figure 5 - Average savings deposit rates at 37 bps (St. Louis Fed)

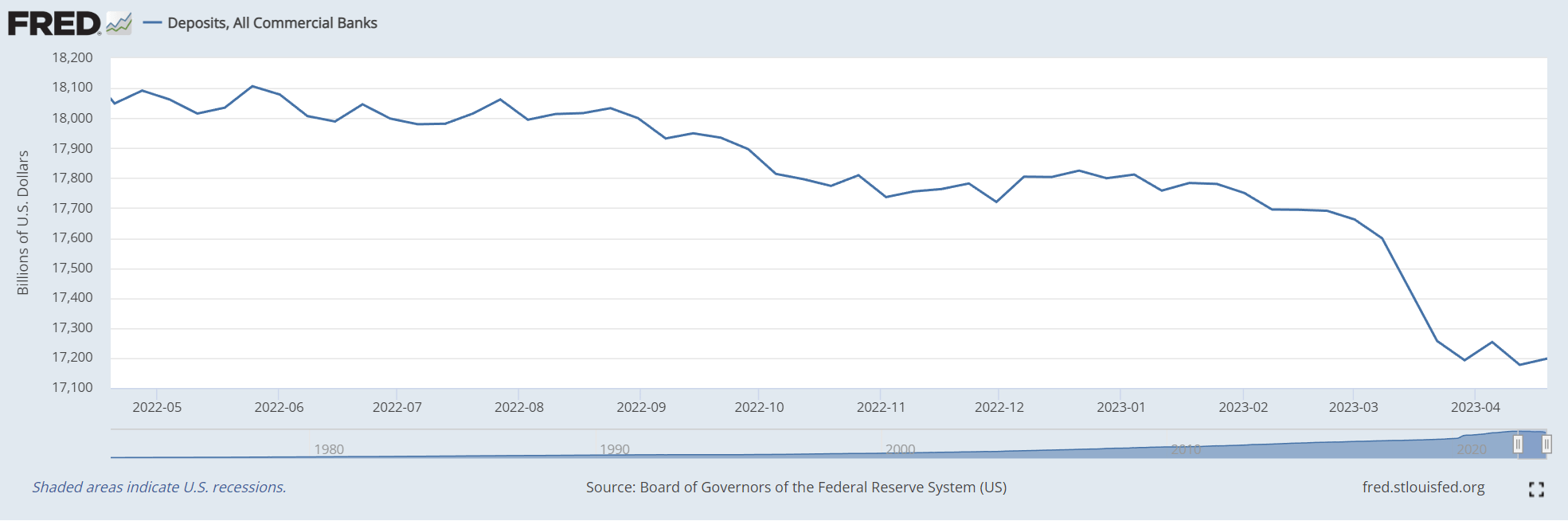

This created an incentive for depositors to take their money out of banks and move into MMFs, earning a difference in yields. In the past 12 months, U.S. commercial banks have seen a massive $900 billion in deposit outflows as a result (Figure 6).

Figure 6 - Commercial banks have seen $900 billion in deposit outflows (St. Louis Fed)

When banks face an outflow of deposits, they can either try to replace the outgoing deposits with new deposits or debt (replace liabilities at a higher cost) or sell loans and securities (reduce assets) to match the lowered deposit balances.

Unfortunately, with hundreds of billions in unrealized losses, the banks were in a conundrum. If they were to sell assets, they will have to crystallize the unrealized losses, creating a massive capital hole that needs to be filled. In fact, this is exactly what SVB Financial tried to do initially, raising equity and crystallizing unrealized losses. But investors, sensing the bank's weakness, rushed for the exits, creating a run on confidence that ultimately sank SVB and Signature Bank.

Another contributing factor to the U.S. regional bank crisis was the fact that the FDIC only insured deposits up to $250,000. This meant many individuals and corporations with account balances above the insurance limit could face a haircut on their money if their banks went under. However, the Global Systemically Important Banks (G-SIBs) like JP Morgan, Bank of America, Citigroup, and Wells Fargo enjoys an implicit guarantee from the U.S. government, as they were 'too big to fail'. This created further incentives for depositors to flee from U.S. regional banks.

I thought The Banking Crisis Was Over...?

In order to stem a rapidly developing banking crisis, the FDIC and regulators stepped in to backstop all the deposits of the failed banks SVB Financial and Signature Bank. This appeared to improve industry confidence for a few weeks, as many regional banking shares stabilized. However, all was not well beneath the surface.

As we learned from First Republic Bank's (FRC) disastrous first quarter earnings report on April 24th, the bank saw a massive contraction in net interest margin ("NIM") from 2.68% in Q1/22 to 1.77% in Q1/23, as it had to raise deposit rates to compete with money market yields. More importantly, the bank saw an incredible $105 billion decline in deposits YoY or 35.5%, despite raising savings rates. Depositors were fleeing FRC en masse.

The first quarter earnings report sank FRC's shares and the bank frantically tried to find a white knight to stem a bank run. Unfortunately, time ran out and FRC was seized by the FDIC on the morning of May 1st, 2023 and sold at an auction to JP Morgan.

The sudden collapse of a seemingly well-run financial institution reignited fears regarding the U.S. regional banking sector. Most troubling was the fact that in all 3 bank failures, the FDIC only 'bailed out' depositors, and basically zero-ed the value of the banks common shares, preferred shares, and bonds.

What Does A Banking Crisis Have To Do With PFFD?

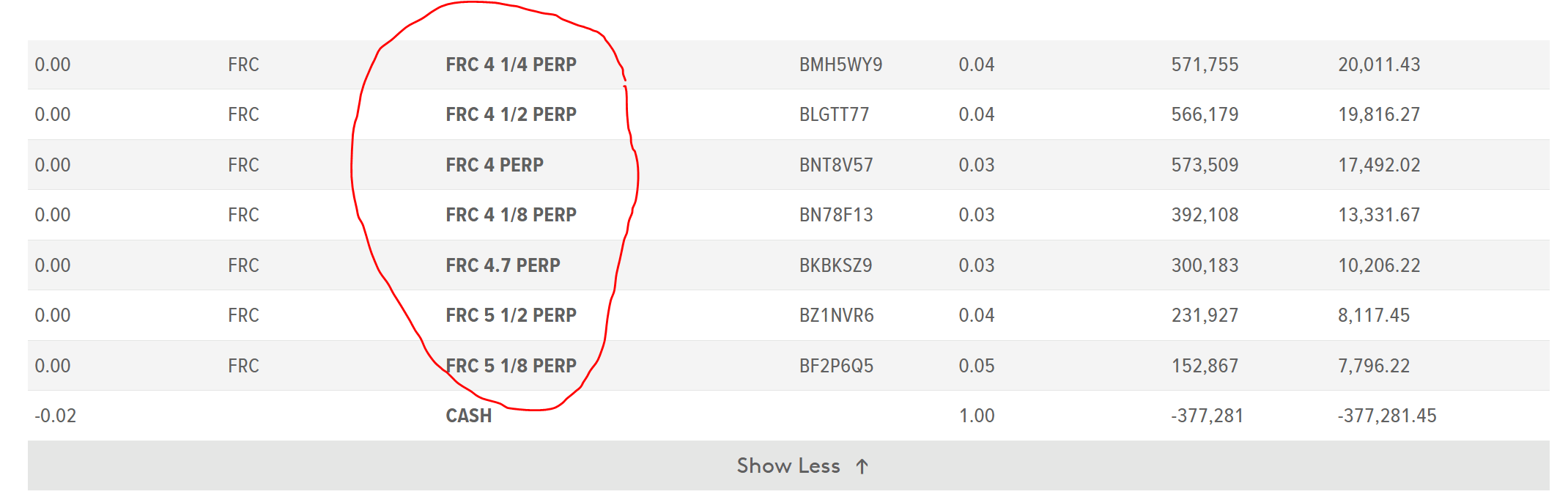

Coming back to PFFD, what does the developing regional banking crisis have to do with the PFFD ETF? Recall in figure 3, I mentioned that 71% of the ETF's holdings were preferred shares of financial companies. Well, in fact, PFFD had sizeable exposures to preferred shares issued by First Republic Bank that are now essentially worthless (Figure 7).

Figure 7 - PFFD held FRC preferred shares that are now worthless (globalxetfs.com)

Furthermore, PFFD continues to hold preferred shares of other regional banks such as Charles Schwab (SCHW), Regions Financial (RF), Synchrony Financial (SYF), KeyCorp (KEY), and PacWest (PACW), just to name a few. While most of these banks are probably sound, there is no way for investors to be sure since First Republic was also a 'well-run' bank that seemingly failed overnight.

Compounding the problem is the haphazard way the FDIC and regulators have been conducting the seizures of SVB, Signature Bank, and First Republic Bank. In a bid to maintain appearances of not bailing out 'fat cat' investors, the FDIC may be exacerbating the run on regional banks by wiping out their shareholders and bondholders. Now, anytime a bank shows signs of weakness, investors run first and ask questions later.

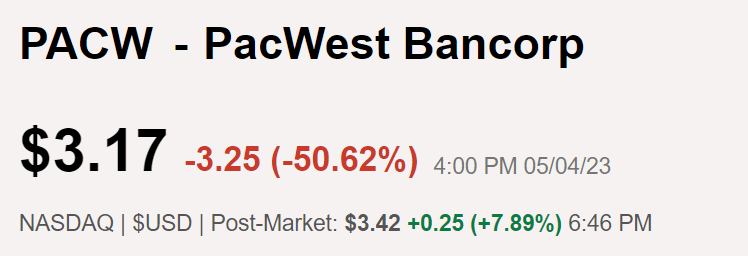

For example, the common shares of PacWest fell by over 50% on May 4th as the bank was rumoured to be looking for a buyer (Figure 8). No investor wants to be left holding the literal bag if/when the FDIC comes in to seize the bank.

Figure 8 - PACW fell by over 50% on May 4th, 2023 (Seeking Alpha)

Buy When There's Blood On The Streets?

There is an old saying that investors should buy when there is blood on the streets, even when that blood is your own. Is now the time to buy these preferred shares with both fists, since there are literally corpses (First Republic) lying around?

Being a cautious investor, I recommend investors hold off for now, since we do not yet know the depths of the crisis nor have regulators and the FDIC come up with a comprehensive solution.

For example, one potential solution to the bank runs is for the FDIC to guarantee all non-interest bearing deposits, i.e. corporate transactional accounts. This could alleviate some of the deposit flight pressure on the regional banks. However, this is controversial as it would entail 'good' banks subsidizing 'bad' banks through the FDIC, according to Wells Fargo's CEO.

Until there is a broader solution, I believe regional banks will continue to face pressures and potential bank runs, and regional bank preferred shares will continue to be sold.

Conclusion

I recommend investors avoid the PFFD ETF, as it has an extremely high exposure to preferred shares issued by financial companies. With the ongoing U.S. regional banking crisis, we are seemingly seeing bank failures on a weekly basis.

Until regulators and the government can address the core problems behind deposit flight out of regional banks, preferred shares issued by regional banks will continue to come under pressure which will negatively impact the PFFD ETF.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.