European Central Bank chief Christine Lagarde. (Source: Bloomberg)

It may not be the end, but it is certainly the beginning of the end of the European Central Bank's hiking cycle. The governing council decided to raise its official deposit rate by a modest 25 basis points to 3.25 percent on Thursday. In a further dovish move, forward guidance was left suitably vague, simply saying that borrowing costs will be “sufficiently restrictive.” Policymakers are smart to relax their tightening stance.

This reduction in scale, following three half-point hikes this year, brings the ECB into line with the Federal Reserve and the Bank of England. The Fed also lifted official rates by 25 basis points on Wednesday, and the BOE is expected to follow suit on May 11. These could prove to be their last upward moves in this cycle, and while the ECB probably isn’t done yet, it clearly didn’t feel sufficiently confident to continue blazing away with a bigger move today when the Fed is probably pausing for the foreseeable future. “We are not pausing, that is very clear,” ECB President Christine Lagarde said in Thursday’s press conference. “We know that we have more ground to cover.”

This more reflective approach is to be welcomed after the past year or so of sharp increases in central bank benchmark interest rates, which are causing problems in the banking sector. While bank failures — or a blowout in the differentials between core and peripheral European sovereign yields — have yet to manifest in the euro area, it makes sense not to test where the frailties lie. With the bulk of the ECB’s €1.3 trillion bank liquidity program, Targeted Longer-Term Refinancing Operations, running off next month, the governing council needs to be vigilant that credit continues to be available to keep the economy afloat.

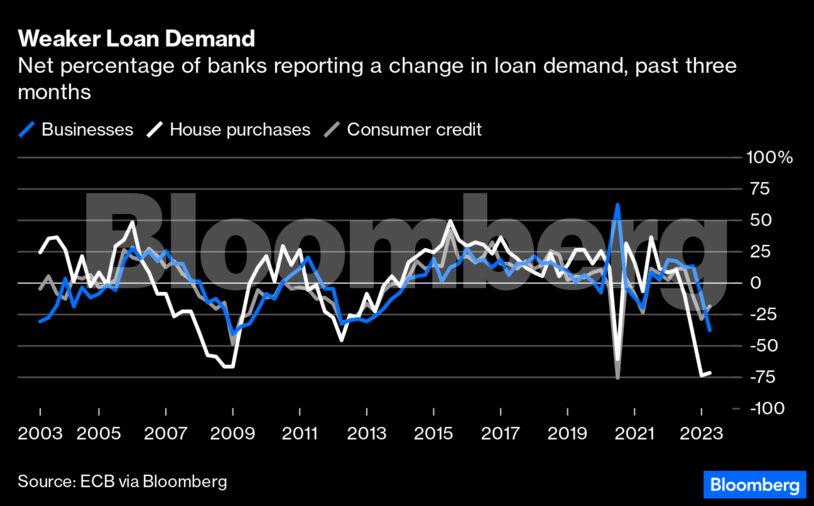

It is the sharp contraction in bank lending that ought to worry the ECB the most as it highlights the risk of overtightening, possibly leading to a credit crunch. Banks reported net declines for mortgages, loans to companies and household consumer credit in the first quarter as they tightened credit standards substantially. March M3 money supply annual growth fell by a record -3.9 percent, while the narrow money M1 measure is contracting at a 10 percent pace. Recession may be avoided — but if it isn't, policymakers can’t claim that there haven’t been plenty of warning signs.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. Views are personal and do not represent the stand of this publication.

Credit: Bloomberg