ESS Tech: Q1 Guestimate And Path To Transparency

Summary

- ESS Tech remains very tight-lipped for a company launching a promising new technology that should be trumpeting its accomplishments.

- Digging out recognized revenue on units already shipped remains pick and shovel work.

- Investors may not have heard about a change in outside auditors because it was announced on a Friday afternoon.

- Completion of automated lines, and commissioning of them, should have begun to chip away at towering quarterly R&D expense.

concept of a modern high-capacity battery energy storage system in a container located in the middle of a lush meadow with a forest in the background. 3d rendering (Stock image not ESS Tech specific). Petmal

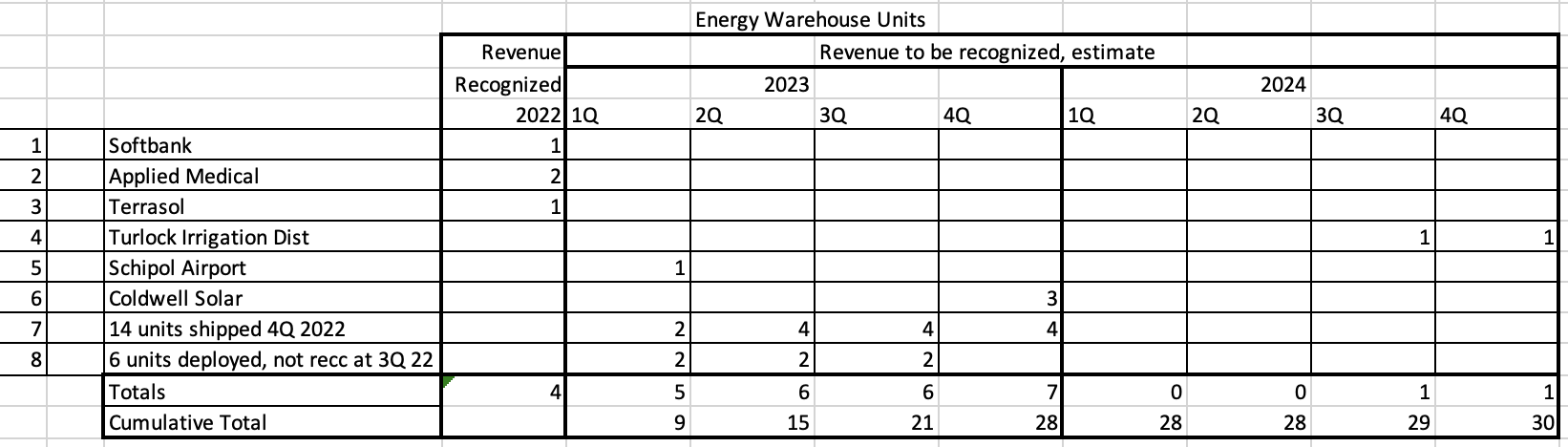

I believe ESS Tech (NYSE:GWH) would benefit from being less elusive on what's required to recognize revenues on Energy Warehouses (ESS terminology for a containerized iron flow battery) they have shipped. Here's my chart on units where revenue has been recognized and estimate of what will be recognized:

Energy Warehouse Estimates (Authors summation of company announcements)

Notes:

1-3) Earnings call Transcript 11/2/22. Answer to question of Joseph Osha

4) "Project Nexus is expected to be complete in 2024." Company release of 2/14/2023

5) company release of 1/23/23

6) "Expected ..operational late 2023". Release 4/12/23

7) Earnings call transcript, Date of Rev rec not specified except "in 23". 3/1/23 call transcript.

8) Earnings call transcript, answering question of Joseph Osha, 6 units w/rev not recognized, dates not spec'd. 11/2/22

Many of the quarterly dates for individual line items are the author's inference from company press releases.

Bear in mind that the most recent unit where revenue was recognized was a single unit to Terrasol Energy in 3Q 2022 where the revenue was $189,000. Management commented on the price of this unit:

So it's not a mile off, but it would probably be to the lower side of what we would expect going forward.

With the pick and shovel work done of digging out unit announcements, an earnings guesstimate is offered. As with a previous attempt, this can only be a guess since management resists providing guidance:

| ElectricPhred | |||

| Actual | Estimate | ||

| 4Q | 1Q | ||

| Revenue | 15 | 945,000 | |

| R&D | 22,879,000 | 16,000,000 | |

| Sales Exp | 1,721,000 | 1,750,000 | |

| G&A | 6,902,000 | 7,000,000 | |

| Net | (25,075,000) | (24,505,000) | |

| eps | $(0.16) | $ (0.16) | |

| Depreciation | 695,000 | 700,000 | |

| Cap ex | 2,994,000 | 2,000,000 | |

| Cash & Short Term | 141,027,000 | 115,222,000 | |

| EW # Rev Recognized | 5 | ||

| Price per EW | 189,000 | ||

| shares out | 152,676,155 | 152,800,000 | |

(Cash + short term = cash + restricted cash + short term investments)

The main numbers I'll be watching here, even more than revenue and eps where I don't expect great things, are cash and R&D expense. I'm assuming R&D will be less, with most of the one time expense associated with automated line installation and startup in the rear view mirror. I expect and hope that number will be down sharply. Cash in the neighborhood I've guestimated implies a significant runway to get us to reasonable revenues.

A map towards transparency

As mentioned above, I believe the company could greatly benefit from greater transparency. Many of the items management that remain opaque are well known to some constituencies (vendors, customers, and competitors but not, alas, shareholders for instance). Many of the opaque items will become known in subsequent disclosures, so why not be up front with them? And yes, I'm fine with some opacity on items that might preserve some competitive advantage.

Here's a list with some suggestions on how management could improve communication

Auditor

On April 14, the company announced E&Y will no longer be their outside auditors. You may not have heard this news since it was buried on a late Friday afternoon-- a time when bad news is often released. But the release stated the decision to seek a new auditor had been made a month earlier. Why not announce, on March 9, that an RFP for a new auditor had been generated despite the fact there were no accounting disagreements?

Revenue Recognition

I believe the company has turned to mush, what should be a very clear delineation on what's required to recognize revenue on an Energy Warehouse. Here's a quote from the 4Q earnings transcript: "four criteria for revenue recognition under GAAP had not been met as the customers did not take full control of the units, which occurs once the units are transferred via the shipping method. " Rather, management should say here are the 4 requirements and here's when we expect to meet them for each of the units already shipped.

It would be fine if units were grouped in buckets, for example: "3 units had not arrived at their install location, 2 were awaiting our onsite commissioning, 1 had not been grid inter tied, 2 had not met contractual minimum performance, etc."

Warranty Expense

I find the company's warranty expense incredibly high. During 2022 $894,000 of revenue was reported, while replacement expense for the year was more than twice that: $1,974,000. Here's a table built from footnote 8 to the financials in 10-Q's and the 10-K:

Warranty Expense (Footnote 8 to 10Q's and 10k)

What part of the technology is failing? What does the trend look like for "Repairs and Replacement" based on changes learned from previous failures?

And what about Australia?

Readers of my past articles have seen a lot of attention on company partner ESI Asia. Some comments have said I place too much emphasis on this partner. But this is the one repeat customer we have and partnering with foreign partners has been flagged as a key element of the company’s own plans for projected growth. Unfortunately the drone pictures and satellite images show zero progress on the parcel ESI apparently has under contract with the owner Fraser Coast Regional Council.

All of the development work ESI and ESS have trumpeted is on land which is, and apparently will remain, under Fraser’s control. What’s been developed to date are the access roads and drainage leading to the proposed ESI site. I have filed for, and Fraser has acknowledged, documents relating to the proposed purchase under Queensland’s Right to Information Act which is like our Freedom of Information Act here. The clock is ticking down on their promised by date.

Conclusions

I have taken yet another tax loss on yet another lot of ESS stock bought and sold at a loss. As I’m now beyond the wash sale rules, I may purchase again after the earnings announcement on May 9, particularly on any weakness. I continue to hold a large warrant position since the warrants have a number of years of life and may provide a lottery ticket type return if the technology works and management becomes a bit more transparent.

I’m not dissuaded that the company’s technology works but they have exhibited more growing pains than I would have expected given a long runway of development. I don’t think SMUD would be a customer or Munich Re would insure performance if there were significant remaining questions.

But management needs to be much more transparent and urge some transparency from their partner ESI Asia. Hopefully we see some of that on May 9.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GWH either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.