Telephone and Data Systems: High Dividend, High Risk

Summary

- Telephone and Data Systems, Inc. looks great on paper, with a dividend yield closing in at 8%.

- Unfortunately, the strategy contradicts management's earnings guidance, and the company can't cover the dividend with cash flow.

- With valuation multiples elevated, I believe TDS stock has limited upside potential and significant downside risk. I rate this stock a sell.

temizyurek/E+ via Getty Images

Telephone and Data Systems, Inc. (NYSE:TDS) looks great on paper, with a dividend yield closing in on 8% and a robust strategy put forward by management. Unfortunately, the strategy contradicts management's earnings guidance, and the financials don't support the dividend today. I believe that TDS stock has limited upside potential and significant downside risk, and investors should look for an opportunity to exit the stock in the near future.

Strategy And Guidance Full Of Contradictions

Telephone and Data Systems is a niche player in the telecommunications space focused on rural and underserved markets. Their business has been relatively stagnant, with revenue growing at a 0.5% CAGR since 2015 and OI declining at a 3.8% CAGR over the same time.

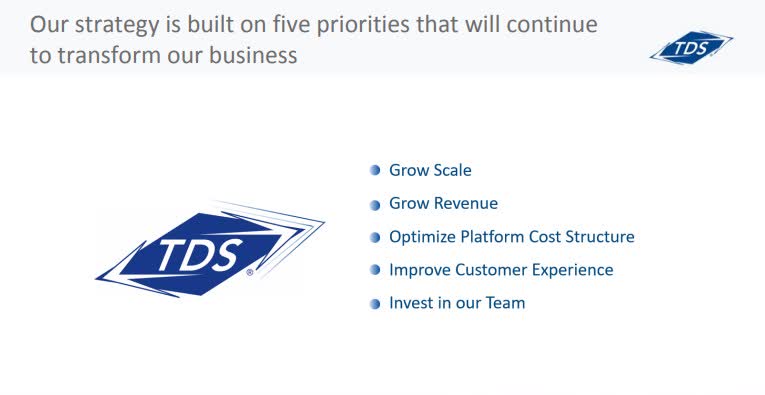

In the Q4 2022 earnings presentation, the company presented a strategy that sounds great on paper. However, their strategy and earnings guidance are full of contradictions.

TDS 2023 Strategy (tdsinc.com/investor-relations/)

First, the company claims to have a strategic priority to grow scale and revenue. That sounds great after years of stagnant revenue. However, the earnings guidance proposes revenue growth from less than 1% at the low end to less than 3% at the high end. To me, that doesn't sound like growing scale and revenue.

Next, the company sets out a goal to optimize its cost structure. Again, that sounds great after years of backward OI. The company then says they want to invest in their team (not usually helpful to cost structure) and delivers earnings guidance with EBITDA declining 10% at the low and flat at the high end. Keep in mind, the EBITDA decline would be on growing revenue. It doesn't seem like cost optimization is really a high priority.

Lastly, the company has a lofty goal to deliver fiber to 60% of addresses by 2026. This is great news since residential fiber drove all of their (minimal) growth in 2022. However, in the Q4 2022 earnings call, management indicated they would scale back on capex to improve cash flow. I don't see how you would rapidly scale fiber deployment (at a cost of $60 to 80K per route mile) to rural communities and scale back capex. In fact, the earnings guidance shows capex only flat to slightly down.

Financials Don't Support The Dividend

Reviewing the financials from the Q4 2022 earnings release, I don't understand how TDS is still a dividend stock, especially one that has increased the payout annually for 49 years. Their cash flow and balance sheet are in a precarious position. A few points really stand out:

- In 2022, interest expense was higher than operating income

- In 2021 and 2022, cash flow from operations didn't cover capex, let alone the dividend payout

- In 2021 TDS returned 76% of net income to shareholders between dividends and share repurchases. In 2022 that increased to 243% of net income

- Long-term debt has increased to $3.7 billion, up from $2.3 billion in 2019

- FCF was only positive once in the last five years

TDS does have long maturities on its debt, some as far out as 2070, and $360 million in cash on hand. With that in mind, the dividend is not an immediate risk.

However, as near-term debt expires, it will be rolled over at higher interest rates, further eroding profitability. As discussed in strategy, the need to invest in expensive fiber internet to maintain revenue will also continue to place a demand on cash.

TDS has essentially been funding the dividend with cheap, long-term debt, and I do not believe they can maintain this strategy much longer without a turnaround in the financials. Based on the 2023 earnings guidance, TDS management doesn't expect a turnaround to occur anytime soon.

Stock Price Relies On Dividend

As discussed above, TDS is certainly not a growth stock, with revenue growing at a 0.5% CAGR since 2015 and OI declining at a 3.8% CAGR over the same time. To that end, valuation multiples suggest the stock is overpriced. P/E is up over 1,000% to historical, EV/Sales is up 8% to historical, and EV/EBITDA is up 19%. With limited growth opportunities, confirmed by management's earnings guidance, the stock price is at the high end of a valuation range.

This is a dividend-driven stock, with a yield close to 8% at the time of publication. But the company can't afford to cash flow its dividend. As the dividend goes, so goes the stock price.

I believe that with the dividend at risk, high valuation multiples, and stagnant financials, the current price has limited upside and significant downside.

Upside Potential

Considering that TDS management isn't even forecasting a turnaround in the financials, the best upside scenario is a buyout by a larger telecom. TDS generates a sizeable portion of its revenue from wholesaling network capacity to the Big Three of Verizon, AT&T, and T-Mobile. Verizon, especially, has shown a desire to acquire rural networks with its 2021 purchase of Bluegrass.

A buyout of TDS by another telecom would likely be a better outcome for shareholder value. This is especially true considering the multi-billion dollar cash flows of the Big Three, and the strong dividends from AT&T and Verizon.

Verdict

TDS is precarious because of its high debt levels and low cash flow. The dividend yield may be attractive, but the company cannot afford to pay it out with current cash flows. Management's earnings guidance shows no signs of improving the financials anytime soon.

Due to these facts, I believe TDS stock has limited upside potential and significant downside risk. Though the dividend yield is attractive, investors should proceed cautiously when considering TDS stock. With that in mind, I recommend investors look for an opportunity to exit the stock in the near future.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.