ETG: This Globally-Diverse CEF Is Worth Considering For Your Portfolio Today

Summary

- Investors are in desperate need of income as inflation is rapidly raising the cost of living.

- Eaton Vance Tax-Advantaged Global Dividend Income Fund invests in a portfolio of common and preferred stocks issued by companies all around the world.

- The ETG fund does not have as much of a focus on dividends as it claims to, but it can still pay out capital gains and provide a solid yield.

- The fund beat the broad market indices over the past twelve months and appears to be able to cover its distribution.

- The ETG fund is currently trading at a very attractive valuation.

- Looking for a helping hand in the market? Members of Energy Profits in Dividends get exclusive ideas and guidance to navigate any climate. Learn More »

FG Trade Latin

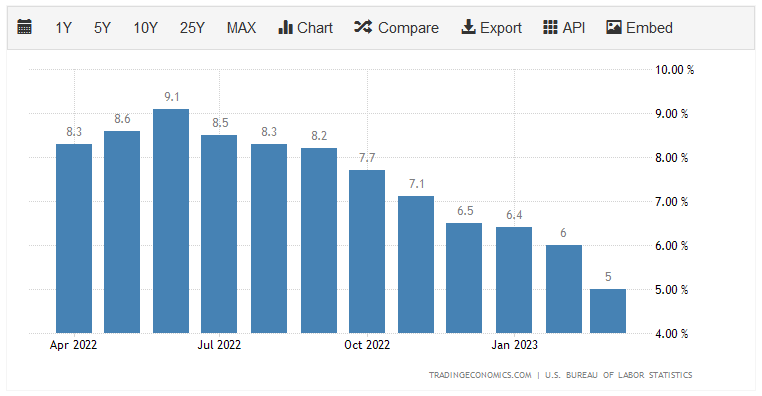

It is essentially certain that the biggest challenge facing most American households today is inflation. Although it has seemingly come down in recent months, we have still seen the cost of living as measured by the consumer price index, increase by at least 6% year-over-year in eleven of the past twelve months:

Trading Economics

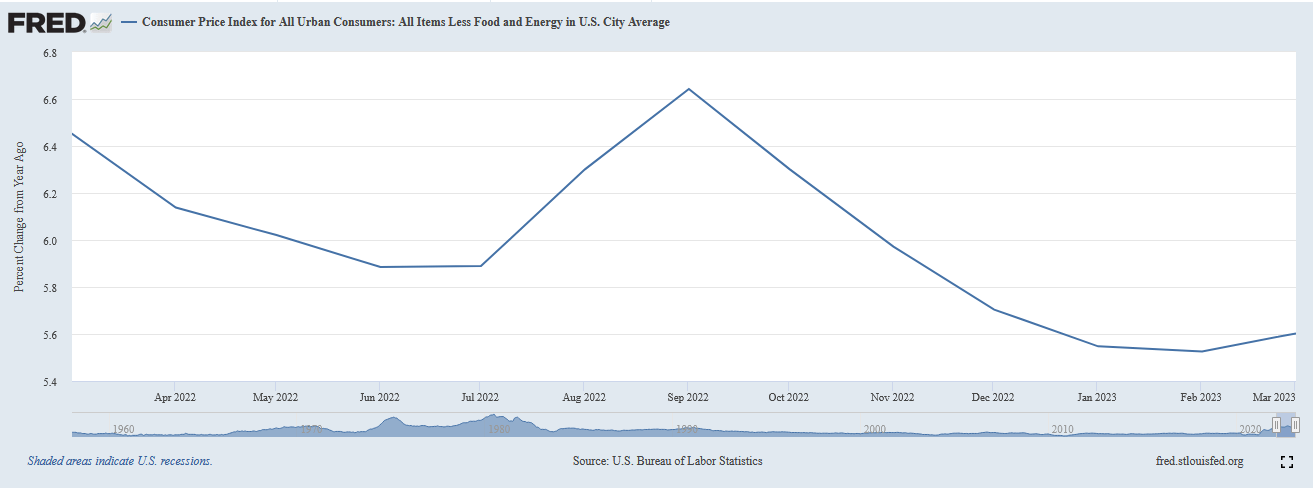

As I stated in a recent blog post, even the improvements that we have seen in the past few months may be misleading. This is because the improvements are almost completely caused by the decline that we have seen in energy prices so far this year. In fact, if we just look at the core consumer price index, which excludes volatile food and energy prices, inflation seemingly got worse in March:

Federal Reserve Bank of St. Louis

This is the reason why April marked the 24th straight month of real wage declines and why a growing number of people are seeking out second jobs or other sources of income. In short, most Americans are desperately in need of new sources of income just to maintain their lifestyles.

As investors, we are certainly not immune from this. After all, we have bills to pay and need to feed ourselves and our families. Fortunately, we do have other means that we can employ to obtain the extra money that we need to accomplish this. That is because we are able to put our money to work for us in obtaining income. One of the best ways to accomplish this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not particularly well-followed by the financial media and financial planners are not usually very familiar with them so it can be difficult to obtain the information that we really want to make an informed decision. That is quite unfortunate as these funds offer a number of advantages over open-ended or exchange-traded funds. Most importantly, these funds are able to employ a variety of strategies that have the effect of boosting their yields well beyond that of any of the underlying assets. As a result, many closed-end funds have some of the highest yields that can be found in the market today.

In this article, we will discuss the Eaton Vance Tax-Advantaged Global Dividend Income Fund (NYSE:ETG), which currently has a 7.55% yield. I have discussed this fund before, but several months have passed since that time so obviously a great many things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage, the Eaton Vance Tax-Advantaged Global Dividend Income Fund has the stated objective of providing its investors with a high level of after-tax total return. This is hardly surprising considering that the fund’s name implies that it invests primarily in dividend-paying common equities. This assumption is supported by the fact sheet’s description of the fund’s strategy:

“The Fund invests primarily in global dividend-paying common and preferred stocks and seeks to distribute a high level of dividend income that qualifies for favorable federal income tax treatment.”

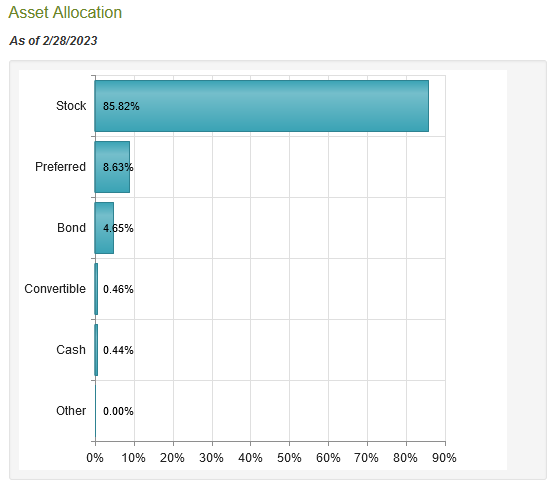

The fund’s portfolio is in line with this strategy as 85.82% of its total assets are invested in common stocks:

CEF Connect

The reason why the emphasis on total return is unsurprising is that common stocks are by their very nature a total return investment vehicle. After all, most investors purchase common stocks in order to receive an income via the dividends that they pay out and benefit from capital gains as the company grows and prospers. The Eaton Vance Tax-Advantaged Global Dividend Income Fund has basically the same goals, and it pays out its capital gains and net dividend income to its investors. This is the common theme with closed-end funds. In short, they aim to maintain a reasonably stable share price and portfolio size while distributing all of their investment profits to the investors.

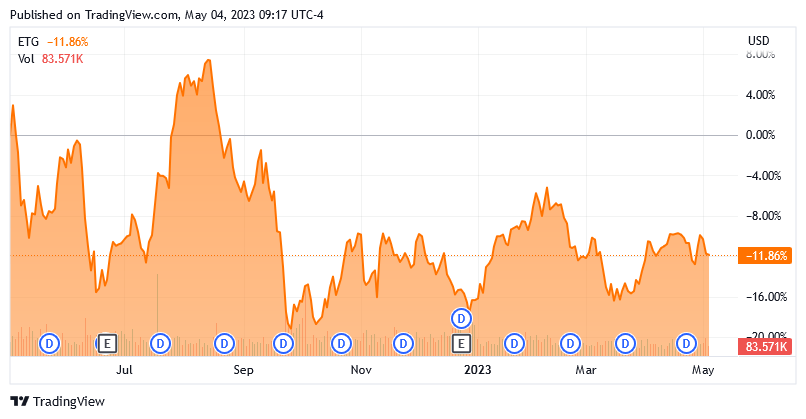

As everyone reading this is no doubt well aware, the last year has not been particularly good for the stock market in either the United States or abroad. As of the time of writing, the S&P 500 Index (SP500) is down 2.01% and the iShares MSCI World ETF (URTH) is down 0.51% over the past twelve months. Both of these indices were down significantly more than these figures last December, but we have seen a strong bull market since that. Unfortunately, the Eaton Vance Tax-Advantaged Global Dividend Income Fund has handed its investors a much more disappointing performance. The closed-end fund is down 11.86% over the same period:

Seeking Alpha

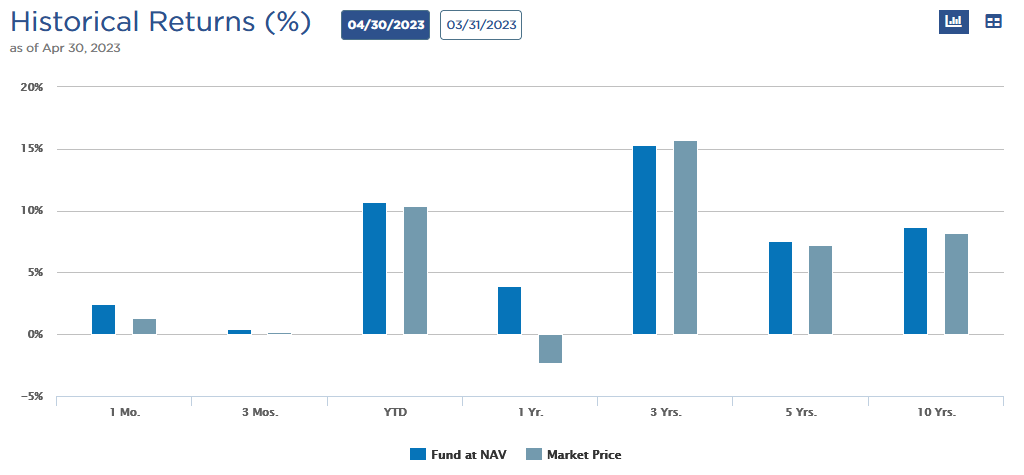

When we consider that the fund boasts a much higher yield than either index, the overall performance differences are not nearly as stark as one may assume. As of April 30, the fund’s portfolio has actually delivered a positive total return over the trailing twelve-month period, although investors in the shares still lost money on a total return basis:

Eaton Vance

It is not uncommon for a closed-end fund’s portfolio to deliver a dramatically different performance than the shares in the market. This is because a closed-end fund is not constantly issuing and redeeming shares in order to ensure that its market price performs in line with the net asset value. This can sometimes result in opportunities in which we can buy the fund’s assets for less than they are actually worth. This is something that we will discuss later in this article.

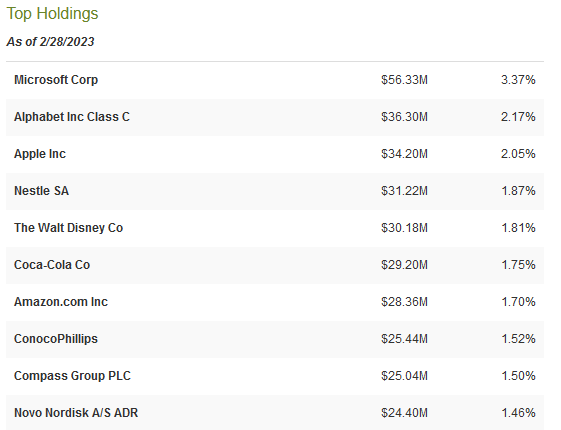

In my last article on the Eaton Vance Tax-Advantaged Global Dividend Income Fund, I showed that this fund is a bit more diverse than many of Eaton Vance’s other equity closed-end funds. This continues to be the case and indeed by some metrics, the fund has improved. Here are its largest positions:

CEF Connect

The first thing that we notice here is that the portfolio does not really make a lot of sense given the fund’s claims that it is investing in dividend-paying stocks. In particular, the four mega-cap technology companies are not things that we would normally expect to see in any dividend portfolio due to the fact that none of these companies pay any sort of respectable dividend. However, there are a number of other companies in this list that likewise pay a negligible yield. Here are the dividend yields from all of the companies that comprise the fund’s largest holdings:

Company | Current Dividend Yield |

Microsoft (MSFT) | 0.89% |

Alphabet (GOOG) | 0.00% |

Apple (AAPL) | 0.55% |

Nestle (OTCPK:NSRGF) | 2.54% |

The Walt Disney Company (DIS) | 0.00% |

Coca-Cola (KO) | 2.89% |

Amazon.com (AMZN) | 0.00% |

ConocoPhillips (COP) | 2.12% |

Compass Group PLC (OTCPK:CMPGF) | 1.50% |

Novo Nordisk (NVO) | 1.41% |

As of the time of writing, the S&P 500 Index yields 1.58%, and the Dow Jones Industrial Average (DJI) yields 1.96%. We can clearly see that only three of the fund’s holdings have higher yields than an index fund. This is certainly not what we would expect to find in any dividend-focused fund, especially considering that there are numerous companies in the shale oil drilling space that currently have yields well above 6%, yet we do not see any of them here. It appears that this fund is focused almost exclusively on capital gains, despite the way that its own fact sheet describes its strategy. I do suppose that it is a blessing that this fund does not have as large of exposure to the non-dividend-paying technology stocks as some of Eaton Vance’s other income funds.

There have been surprisingly few changes since the last time that we discussed this fund. In fact, the only significant change is that EOG Resources (EOG) was removed from the fund’s largest positions and replaced with Compass Group PLC. I am not particularly happy about the reduction in energy exposure, particularly considering that there are some signs that energy prices will rebound over the next few months if the United States manages to avoid a recession. However, a food service company does add some diversification and the extra international exposure is nice to see. Overall, the fact that so few positions have changed over the past few months could be a sign that this fund has a fairly low turnover. It had an annual turnover of 59.00% in 2022, which is about average for an equity closed-end fund. The reason why this is important is that it costs money to trade stocks or other assets, which is billed directly to the shareholders. This creates a drag on the fund’s performance and makes management’s job more difficult because it will need to generate sufficient excess returns to cover these additional expenses and still deliver an acceptable return for the fund’s shareholders. This fund managed to beat the major indices over the past year, so it does appear that management is doing an adequate job at that task for the time being. However, past performance is no guarantee of future results, so we will want to constantly monitor the fund and ensure that it continues to deliver adequate returns.

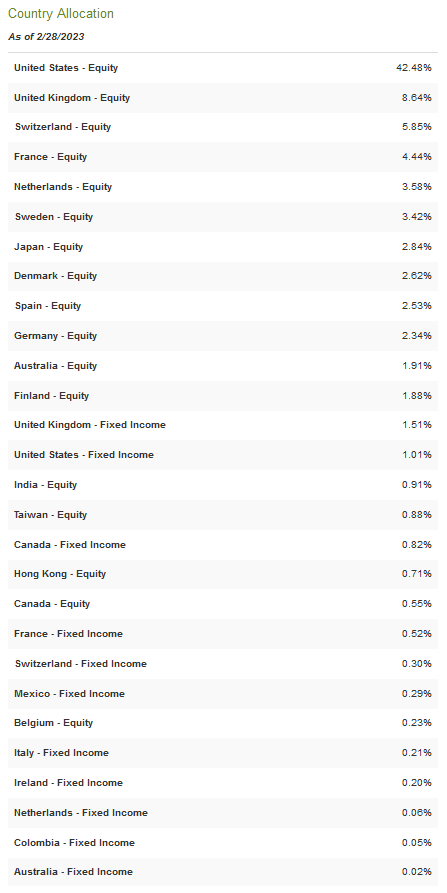

As implied by the name of the fund, and stated earlier in the article, the Eaton Vance Tax-Advantaged Global Dividend Income Fund is a global fund that holds securities issued by companies that are located all over the world. We can see this by looking at the fund’s largest positions, as Nestle, Compass Group, and Novo Nordisk are all foreign companies. This foreign exposure extends across the company’s entire portfolio. In fact, as shown here, only 42.48% of the fund’s assets are invested in American companies:

CEF Connect

This is a very internationally diverse portfolio for a global fund. As I have pointed out in various previous articles, most global funds have 60% to 70% of their assets invested in American companies. The fact that this one has lower is nice to see and it allows the fund to be included in a portfolio with other funds and effectively reduce the overall domestic exposure. This is nice because of the protection that it provides us against regime risk. Regime risk is the risk that some government or other authority will take an action that has an adverse impact on a company in which we are invested. The only real way to protect ourselves against this risk is to ensure that only a relatively small percentage of our assets is exposed to any individual nation. As we can clearly see, the Eaton Vance Tax-Advantaged Global Dividend Income Fund appears to be doing a reasonable job at this.

Leverage

In the introduction to this article, I stated that closed-end funds such as the Eaton Vance Tax-Advantaged Global Dividend Income Fund have the ability to employ certain strategies that increase their yields beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund is borrowing money and then using that borrowed money to purchase domestic and foreign common and preferred stocks. As long as the purchased assets can provide a higher total return than the interest rate that the fund has to pay on the borrowed funds, the strategy works pretty well to boost the effective yield of the portfolio. Since this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much leverage since that would expose us to too much risk. I do not usually like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. The Eaton Vance Tax-Advantaged Global Dividend Income Fund, fortunately, fulfills this requirement as its levered assets only comprise 21.67% of the portfolio as of the time of writing. Thus, it appears that this fund is striking a reasonable balance between risk and reward.

Distribution Analysis

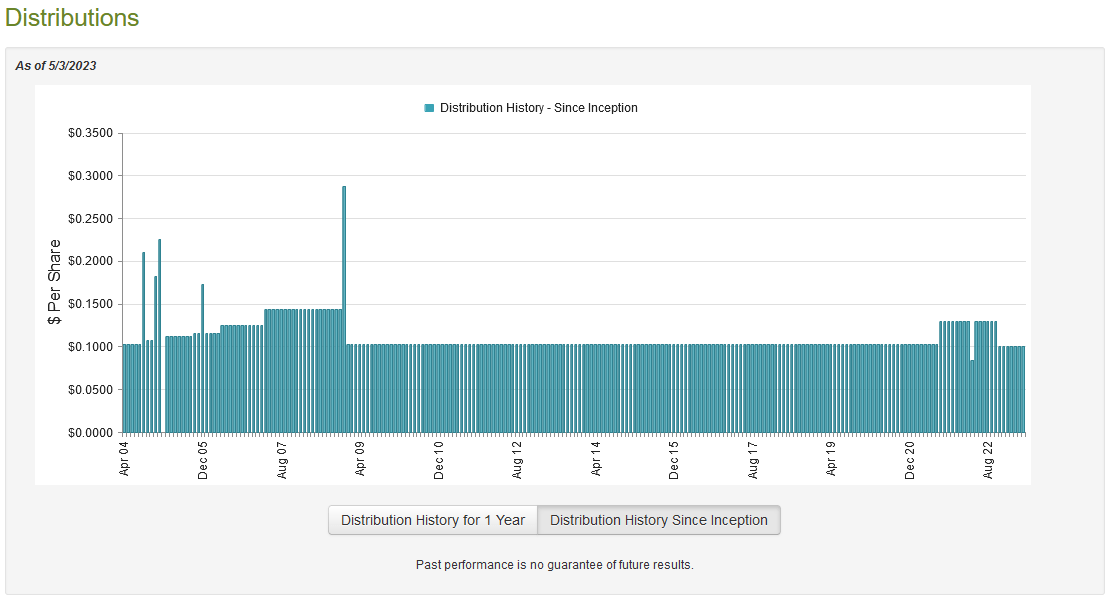

One of the biggest reasons why investors purchase shares of closed-end funds is that these entities usually have higher yields than just about anything else in the market. This comes from the fact that most closed-end funds aim to maintain a relatively stable portfolio size and pay out all of their capital gains to investors. Thus, the yields can be quite high if the portfolio manages to achieve reasonable returns. In the case of this fund, it clearly appears to be doing that and applies a layer of leverage to boost its effective yield further. Thus, we can assume that the fund probably has a fairly high distribution yield. That is certainly the case as the Eaton Vance Tax-Advantaged Global Dividend Income Fund pays a monthly distribution of $0.1001 per share ($1.2012 per share annually), which gives the fund a 7.55% yield at the current price. The fund used to be a very consistent distribution payor, but it cut its distribution back in November 2022 along with many of Eaton Vance’s other funds:

CEF Connect

The biggest reason for the distribution cut is probably because of the fund’s large exposure to the mega-cap technology companies, which significantly underperformed the market last year. I showed this in a prior blog post. While it was far from the only fund to get caught off guard by the disappointing performance of many of these stocks, and in fact, it is somewhat less exposed to the major technology companies than the S&P 500 Index as a whole, the fact that it had to cut the distribution may still be a turn-off for those investors that are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. However, it is important to keep in mind that anyone buying the fund’s shares today will receive the current distribution at the current yield and will not be hurt by the fact that the fund cut its distribution several months ago. As such, the most important thing for anyone considering buying this fund today is its ability to sustain the current distribution.

Unfortunately, we do not have a particularly recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund’s most current financial report is its annual report which corresponds to the full-year period that ended on October 31, 2022. As such, this report will not include any data regarding the fund’s performance over the past six months. This is unfortunate because the market has rebounded quite a bit year-to-date so the fund probably enjoyed some investment profits over the period that can help to support the distribution. We will not see those profits reflected in this report, but we should still get at least some idea of the fund’s financial performance and the rationale behind the distribution cut in November. During the full-year period, the Eaton Vance Tax-Advantaged Global Dividend Income Fund received $50,361,870 in dividends and $9,943,433 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund had a total investment income of $61,819,964 over the period. It paid its expenses out of this amount, which left it with $38,670,263 available for the shareholders. As might be expected, this was nowhere close to enough to cover the distributions that the fund paid out over the period. This fund paid out $119,073,693 in distributions over the course of the year. At first glance, this is something that may be concerning as the fund’s net investment income was nowhere close to enough to cover its distributions.

However, the fund does have other methods that it can employ to obtain the money that it needs to cover the distributions. For example, it might be able to generate sufficient capital gains that can be paid out to the investors. As might be expected from the poor performance of the markets over much of 2022, the fund generally failed at this, but it did not do overly poorly. During the full-year period, the fund achieved net realized gains of $82,416,737 but this was more than offset by $505,718,500 net unrealized losses. Overall, the fund’s assets under management declined by $501,004,691 after accounting for all inflows and outflows. While this is disappointing, the fund’s net investment income plus net realized gains were enough to cover its distributions, albeit barely. These two items together totaled $121,087,000, which was more than the distribution. The reason for the distribution cut thus appears to be that the fund’s lower asset base makes it much harder for the fund to earn the returns that it needs to sustain the previous level and that management expected 2023 to be a challenging market. It remains to be seen whether the fund will be able to cover the distribution at the new level but so far, the market has been cooperative.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Tax-Advantaged Global Dividend Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of May 3, 2023, the Eaton Vance Tax-Advantaged Global Dividend Income Fund has a net asset value of $17.49 per share but the shares currently trade for $15.76 each. This gives the shares a 9.89% discount on the net asset value at the current price. This is better than the 8.50% discount that the shares have averaged over the past month, and it is a very reasonable price to pay for the fund. Overall, the price for this fund certainly appears to be quite reasonable today.

Conclusion

In conclusion, investors are generally in need of income today in order to maintain their standard of living in the face of the highest inflation that we have seen in four decades. The Eaton Vance Tax-Advantaged Global Dividend Income Fund appears to be a very reasonable way to accomplish that task as it has a fairly respectable distribution, an attractive valuation, and a reasonably diverse portfolio. The fact that the fund has beaten the S&P 500 Index over the past year is also a very attractive characteristic. Admittedly, the fund’s distribution cut several months ago may be a bit of a turn-off but that has no impact on anyone purchasing the shares today. Overall, Eaton Vance Tax-Advantaged Global Dividend Income Fund is worth considering for your portfolio.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

At Energy Profits in Dividends, we seek to generate a 7%+ income yield by investing in a portfolio of energy stocks while minimizing our risk of principal loss. By subscribing, you will get access to our best ideas earlier than they are released to the general public (and many of them are not released at all) as well as far more in-depth research than we make available to everybody. In addition, all subscribers can read any of my work without a subscription to Seeking Alpha Premium!

We are currently offering a two-week free trial for the service, so check us out!

This article was written by

Traditionally, we have not always responded to comments but in order to improve the quality of our research, comments will be reviewed and we will respond to issues regarding errors or omissions. This does not include our premium service, "Energy Profits In Dividends" which is available from the Seeking Alpha Marketplace. This service does include detailed discussions with our team both on the reports themselves and in a private forum.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.