BYD Overtakes Volkswagen As China's No. 1 Auto Brand

Summary

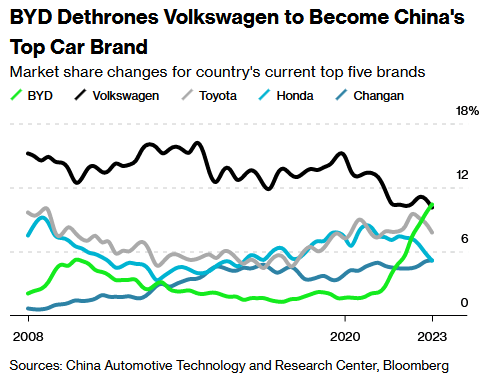

- According to Bloomberg, Volkswagen has been the No. 1 selling brand in China for at least 15 years.

- That streak ended in Q1 of this year, with BYD leapfrogging Volkswagen in sales with a rather stunning increase in EV output over the past year.

- While BYD doesn't plan to offer passenger EVs in the U.S. anytime soon, the company plans to expand sales in the EU, Latin America, and across Asia.

- Considering BYD's market cap is still only ~20% that of Tesla's, odds are that that valuation gap will close this year. Meantime, keep an eye on Ford.

Green Energy Vehicles At 2022 Central China International Auto Show Getty Images

In late April, Bloomberg reported that China-based BYD (OTCPK:BYDDY) has finally overtaken Volkswagen (OTCPK:VWAGY) as the No. 1 automobile brand in China (see graphic below). As BYD has flexed its domestic muscle, note that sales for Toyota (TM) and Honda (HMC) also have been falling of late. Bottom line is that BYD, formerly thought of as an "EV-battery company," has unleashed its power in the battery and EV supply chains to position itself as the company of the future in the world's largest and fastest-growing automobile market. Automakers dependent on China for a large majority of their growth (think Tesla (TSLA) and General Motors (GM) for instance), are going to have to rethink their strategy because competing against BYD in China could wreak havoc with their margin. Indeed, trying to hang onto market share may be one big reason Tesla had to cut prices in China and now plans to ship China-made Model-Ys to the US.

Bloomberg

Investment Thesis

As most of you know, BYD (which stands for "Build Your Dreams") more-or-less started out as a Warren Buffett and Berkshire (BRK.A) supported battery manufacturer. That history serves BYD well today as its scales up its EV manufacturing operations. However, BYD continues to invest in building out its EV-battery manufacturing capacity. Recently, according to the South China Morning Post, BYD plans to invest $1.2 billion in a new battery factory in Zhengzhou. BYD is currently the third largest EV battery manufacturer in the world, behind only No. 1 Chinese battery giant CATL and South Korea's LG Energy Solutions.

The larger point here is that BYD is likely to begin dominating the Chinese EV market because it has the size, scale, and battery manufacturing attributes and skill-sets that are all requirements to be an EV leader in China (and throughout the world). Meantime, China appears to be moving toward a more nationalistic attitude these days, which - in my opinion - means more of a "buy China" consumer market that also favors BYD.

BYD continues to move overseas with the introduction of the "Yuan Plus" EV in Columbia last October. That came after similar introductions across Costa Rica, Uruguay, and the Dominican Republic. In addition to focusing on Latin America for growth, BYD also recently opened its first dealership in Japan. And, at last year's Paris EV-expo, BYD rolled out three new EVs for the EU market.

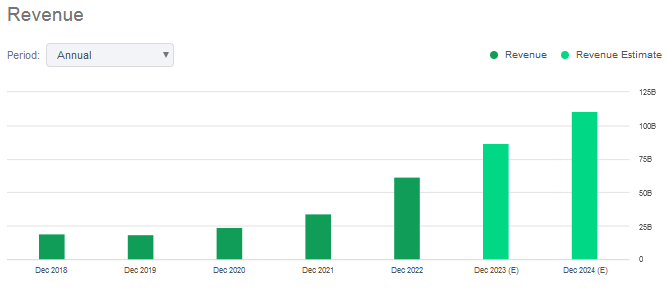

Revenue Growth

Along with the significant up-tick in BYD's global EV sales, the company's annual revenue growth profile has also been greatly enhanced:

Seeking Alpha

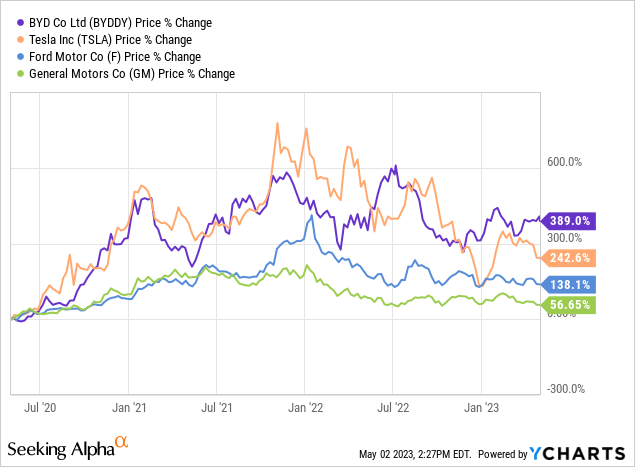

However, despite BYD's progress in the EV market, note the company's current market cap is arguably quite low compared to Tesla (as reported by Seeking Alpha):

- BYD: $99.4 billion

- Tesla: $512.9 billion

- Ford: $48.2 billion

That being the case, I have two observations here:

- I think the valuation gap between Tesla and BYD is going to narrow - partly because BYD's should rise and Tesla's could arguably fall as its margin continues to come under pressure.

- Somewhat ironically, Ford could actually be positioned very well in order to make significant headway in the EV market.

On point No. 2, Ford has two excellent EV offerings that have seen very strong demand: The F-150 Lightning truck and the Ford Mustang Mach-E. The Mustang has such a strong brand that Ford could see success establishing that model overseas. Note Ford announced it will recommence taking new orders for the Mustang Mach-E tomorrow (Wednesday, May 3). The company had previously stopped taking orders for the Mach-E because demand was so strong it outstripped the company's capacity to make them. However, Ford recently completed manufacturing plant upgrades to support a production ramp of the Mach-E in the second half of this year. It will be very interesting to watch Mach-E delivery volumes over the coming months.

Meantime, Ford also announced it has lowered the prices on the Mach-E by a range of $1,000 to $4,000 across different variants. The starting prices of the all-electric Mach-E SUV will be between $42,995 and $59,995, with all versions qualifying for a 2023 Inflation Reduction Act federal tax credit of $3,750. This is why I say that Ford looks extremely well positioned to establish itself as a strong competitor to Tesla (and all comers ...) in the domestic EV market.

Risks

Now that BYD has established itself as not only a battery maker, but also as a leading EV maker, it's interesting that Berkshire is trimming its stake in the company. Seeking Alpha reported that Berkshire recently reduced its stake to 11.87% after selling 4.235 million Hong Kong-listed shares. As per the filing referenced in that article, that transaction lowered Berkshire's holdings in BYD's H-shares down from prior 12.26% stake.

Is Berkshire nervous that its stake in BYD could be a liability if U.S./China trade tensions grow, or if China were to make a huge mistake and hit Taiwan? Who knows? Regardless, Berkshire's stake is big enough to be a significant headwind for the stock going forward if the company plans to liquidate its entire position.

BYD is facing increasing competition from Tesla and a host of China-based EV makers. However, as the first graphic in the article shows, BYD has faced all those obstacles over the past two years and the company is arguably winning. Indeed, BYD has powered onward and upward over the past three years (see chart below). And that's likely due to its battery manufacturing advantage, combined with China's dominance in the global EV supply chains and the company's advantage of being a China-based company and its status as the world's biggest and fasting growing auto market.

Summary and Conclusion

I rate BYD a hold for U.S. investors. Not so much because I don't think BYD can compete effectively for global EV sales - indeed, I feel just the opposite. My issue is China's increasingly aggressive military posture with respect to Taiwan, and concerns that if China takes serious military action on Taiwan, sanctions on the country by the U.S. and its Democratic and NATO allies could likely be swift and severe and would negatively impact investments in China-based companies. For example, we saw a similar fallout for investors in the VanEck Russia ETF (RSX) (see RSX: The Russia ETF In a Word: Toxic).

Meantime, Ford looks very interesting to me here. The stock is down 13.6% over the past year and at pixel time is down 2.7% during today's sell-off (Tuesday, May 2) to a current price of $11.72. During 15 years of contributing on Seeking Alpha, I have never placed a BUY rating on an American automaker. But I am doing it today. I find Ford's 5% yield and its positioning in the domestic EV market, combined with its leading F-150 truck popularity, quite attractive here. And that is despite concerns of a potential recession in the 2H of this year. Ford is a buy.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I am an electronics engineer, not a CFA. The information and data presented in this article were obtained from company documents and/or sources believed to be reliable, but have not been independently verified. Therefore, the author cannot guarantee their accuracy. Please do your own research and contact a qualified investment advisor. I am not responsible for the investment decisions you make.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.