SMHB: A Huge Yield With Specific Risks

Summary

- ETRACS 2xMonthly Pay Leveraged US Small Cap High Dividend ETN has an impressive distribution rate.

- The SMHB exchange-traded note incurs 3 specific risks that plain vanilla ETFs don’t have.

- Moreover, SMHB has suffered a steep decay in value and distributions.

- Quantitative Risk & Value members get exclusive access to our real-world portfolio. See all our investments here »

FooTToo/iStock via Getty Images

SMHB strategy

ETRACS 2xMonthly Pay Leveraged US Small Cap High Dividend ETN (NYSEARCA:SMHB) is an exchange-traded note, or ETN, launched on 11/08/2018 and leveraging the Solactive US Small Cap High Dividend Index. It has an impressive 12-month trailing distribution rate of 28% and an annual fee of 0.85%. Such a high yield clearly targets income-seeking investors. This article aims at warning them of specific risks.

As described by UBS, this financial product...

...is designed to provide 2 times leveraged long exposure to the compounded monthly performance of the Solactive US Small Cap High Dividend Index, less financing costs and tracking fees, and may pay a variable monthly coupon linked to the leveraged cash distributions associated with the underlying index constituents.

The underlying index has 100 constituents, listed on Solactive website (click here to see them).

Risk #1: Counterparty risk

However, ETRACS 2xMonthly Pay Leveraged US Small Cap High Dividend ETN has no portfolio with holdings to guarantee an asset value. SMHB is an exchange-traded note, not an exchange-traded fund ("ETF"). To be more specific, it is "senior Series B unsecured debt securities issued by UBS, maturing on November 10, 2048." Therefore, it incurs a counterparty credit risk. UBS Group's credit rating is A- at Standard and Poor's, AA- at Fitch, and A3 at Moody's, all with negative outlook since the acquisition of Credit Suisse. Anyway, ETNs may not resist a major banking crisis.

Risk #2: Leveraged drift

Most leveraged ETFs have a daily objective. This ETN has a monthly one. It may also suffer a decay due to leveraging, but it works differently on a monthly time frame. Imagine an asset that goes up 25% one month and down 20% the next month. A perfect double-leveraged product goes up 50% the first month and down 40% the second month. On the close of the second month, the underlying asset is back to its initial price:

(1 + 0.25) x (1 - 0.2) = 1

At the same time, the perfect leveraged product has lost 10%:

(1 + 0.5) x (1 - 0.4) = 0.9

Nothing has changed for the underlying asset, and the product price is down 10%. It is not a scam, just the normal behavior of a leveraged and rebalanced portfolio. A good news: In a trending market, beta-slippage can be positive. If the underlying index goes up 10% two months in a row, at the end of the second month, it is up 21%:

(1 + 0.1) * (1 + 0.1) = 1.21

Then, the perfect 2x leveraged product is up 44%:

(1 + 0.2) * (1 + 0.2) = 1.44

The drift is path-dependent. If the underlying index gains 50% on month 1 and loses 33.33% on month 2, it is back to its initial value, like in the first example. However, the 2x product loses one-third of its value, instead of 10% in the first case:

(1 + 1) x (1 - 0.6667) = 0.6667

Without a demonstration, it shows that the higher the volatility in monthly time units, the higher the decay.

Risk #3: Forced redemption

As a consequence, if the underlying index goes down more than 50% in one month due to a market crash, the face value may theoretically become negative. To avoid losses, UBS may force the redemption overnight. As described in a prospectus supplement:

If the intraday indicative value of the Securities equals $2.00 or less (as adjusted in the event the Securities undergo a split or reverse split) on any Index Business Day, the Securities may be accelerated and redeemed by UBS (...)

In fact, as written in the same document, UBS may force the redemption for any reason with an 18-day prior notice:

On any Business Day on or after November 15, 2019 through and including the Maturity Date (the "Call Settlement Date"), UBS may at its option redeem all, but not less than all, issued and outstanding Securities. To exercise its Call Right, UBS must provide notice (which may be provided via press release) to the holders of the Securities not less than eighteen (18) calendar days prior to the Call Settlement Date.

In any case, if the calculated face value on the settlement date is negative, the redemption value for investors will be zero.

This is not just theory. There is already a long list of defunct high-yield monthly leveraged ETNs, most of them issued by UBS: CEFL, BDCL, SDYL, MLPQ, MORL, SMHD… You can't find them in financial websites anymore because they have been delisted, but you can see here an example of mandatory redemption. In fact, the question is not if such a product will be terminated, but when. Mandatory redemption has a high probability to happen when the underlying index has fallen hard, letting investors with little residual value and deep losses.

Risk #4: Past performance

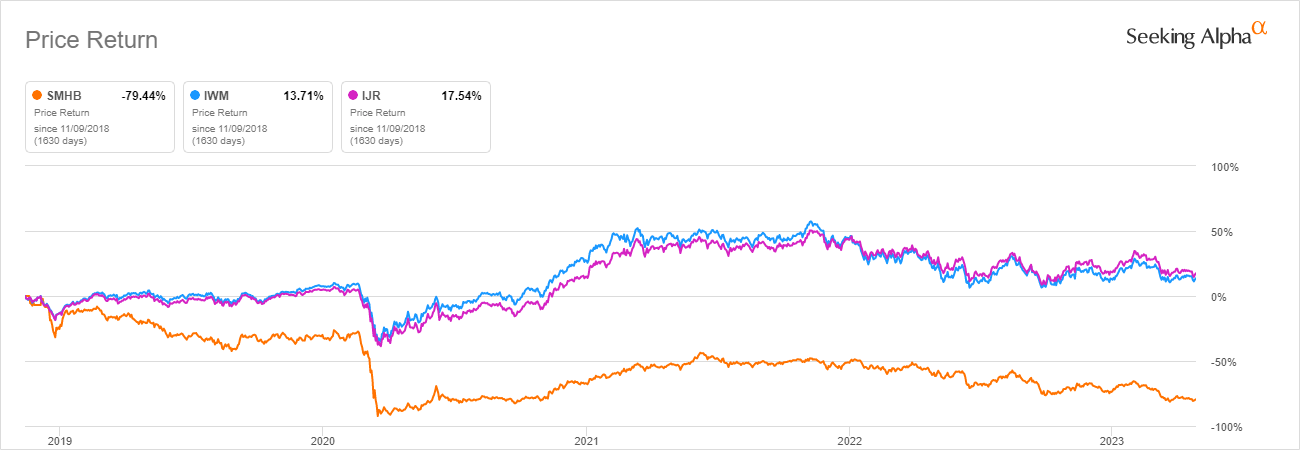

The next chart compares the total returns of SMHB and ETFs representing two small-cap benchmarks (non-leveraged): The iShares Russell 2000 ETF (IWM) and the iShares Core S&P Small-Cap ETF (IJR). The ETN performance is underwhelming in comparison.

SMHB vs Russell 2000, S&P 600 (Seeking Alpha)

SMHB has paid a high yield while its value has suffered a steep decay. In fact, the price has lost 78% since inception:

SMHB price history (Seeking Alpha)

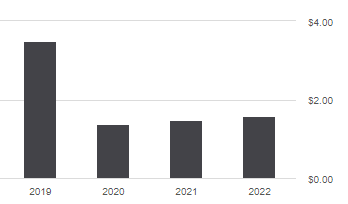

The ETN value and distribution may fall very hard in a market crash. Then, because of the monthly rebalancing, recovery is not guaranteed, even if the underlying index recovers. As a result of the 2020 market meltdown, the annual sum of distributions has decreased from $3.48 per share in 2019 to $1.58 in 2022. It means the income stream has shrunk by 54.6%, whereas the cumulative inflation has been about 15% at the same time (based on CPI).

SMHB distribution history (Seeking Alpha)

Takeaway

ETRACS 2xMonthly Pay Leveraged US Small Cap High Dividend ETN may be useful for swing trading or capturing some short-term market anomalies, but I don't see SMHB as a good long-term investment to preserve income and capital. It incurs 3 risks that plain vanilla ETFs don't have: counterparty risk, leveraged drift, and forced redemption. Moreover, the product's short history already shows a steep decay in both value and distribution. This last point is not specific to a leveraged ETN. Most financial products with a yield superior to 6% have suffered from a decay in share price and/or distribution since inception.

Quantitative Risk & Value (QRV) features data-driven strategies in stocks and closed-end funds outperforming their benchmarks since inception. Get started with a two-week free trial now.

This article was written by

Step up your investing experience: try Quantitative Risk & Value for free now (limited offer).

I am an individual investor and an IT professional, not a finance professional. My writings are data analysis and opinions, not investment advice. They may contain inaccurate information, despite all the effort I put in them. Readers are responsible for all consequences of using information included in my work, and are encouraged to do their own research from various sources.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.