Microsoft Q3 Earnings: AI Speech Steals The Show

Summary

- Microsoft's AI prospects, the moment investors had been waiting for.

- Microsoft results remind investors of ''2023, The Year of the Stock Picker''

- Microsoft is clearly not cheap, but as long as it can continue delivering high single digits growth rates, investors will continue to pay up a high multiple for MSFT stock.

- Looking for a helping hand in the market? Members of Deep Value Returns get exclusive ideas and guidance to navigate any climate. Learn More »

Olivier Le Moal

Investment Thesis

Microsoft (NASDAQ:MSFT) had been buzzing since the start of 2023 for being a pioneer in its partnership with OpenAI. And as you'd expect investors and analysts were eagerly listening to every word and nuance of the earnings call with bated breath.

Masterfully, Microsoft came out to show a ''little leg'' of its prospects around AI but was quick to resume to remind investors that there's a lot more to Microsoft than future prospects around AI.

The message from these earnings results was clear, Microsoft isn't seeing the dreaded slowdown in IT spend. Microsoft is still in growth mode.

AI Prospects, the Showdown? Tune in For the Next Episode

Microsoft's Intelligent Cloud segment takes the limelight again. For investors, this was absolutely terrific news. Not only does this show that Microsoft's growth engine is still intact.

But on top of this, it has a multiplier effect that highlights that despite all the investor concerns about the IT segment seeing a slowing down in IT spend turns out not to be quite as accurate as many had presumed.

To put it another way, throughout 2023 we've all heard that 2023 is the ''Year of the Stock Picker'' and I believe Microsoft's outperformance after hours goes some way to reaffirm that assertion. That detail and nuance matter again in investing.

From Coursera and Grammarly to Mercedes-Benz and Shell, we now have more than 2,500 Azure OpenAI Service customers, up 10x quarter-over-quarter.

Microsoft's CEO Satya Nadella started the earnings call by whetting investors' appetite toward Microsoft's next wave of growth, Azure OpenAI Service. But the takeaway from the earnings call was more than just silver narratives over AI's future prospects.

The message was abundantly clear, that 2023 is shaping up to resume the cloudification and digitalization of businesses.

Teams usage is at an all-time high and surpassed 300 million monthly active users this quarter, and we once again took share across every category from collaboration to chat to meetings to calling

Consider the quote above. Presently, Teams reached an all-time high. At a time when we are being told that employees were returning back to the office and that the Work From Anywhere element of working was retracing. It appears that Wall Street's narrative didn't line up with the facts. Again, nuance matters, which we'll discuss in the next section.

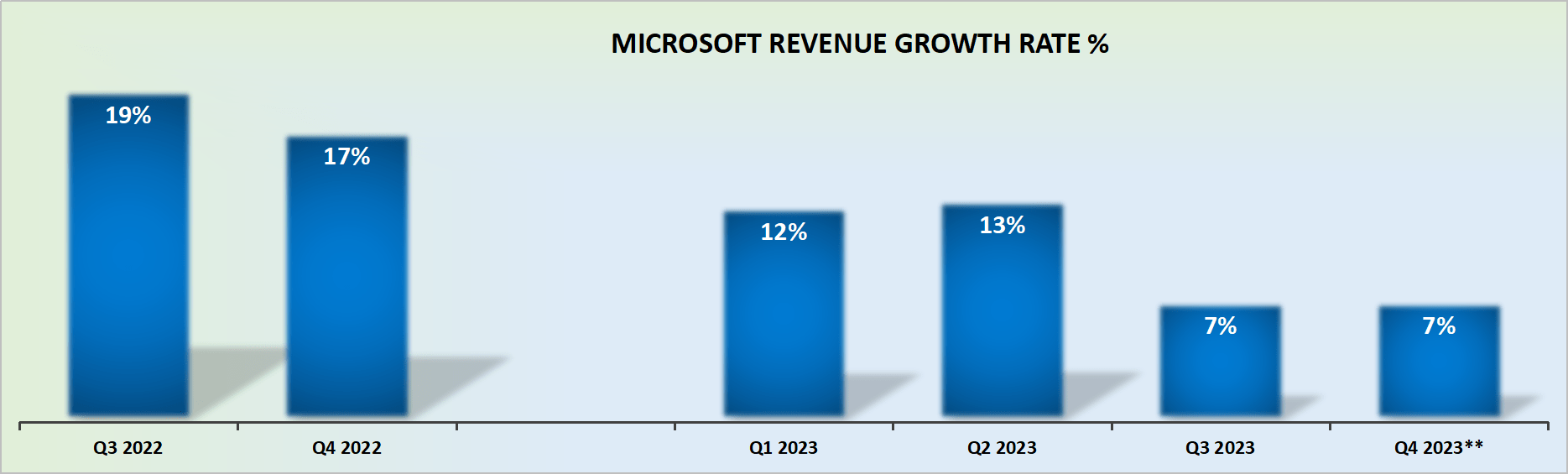

Revenue Growth Rates, Still in Growth Mode

MSFT revenue growth rates

Microsoft took investors by surprise with its solid guidance for the quarter ahead.

Investors had been fearing that Microsoft's growth rates would be grinding to a halt. Case in point, consider the path that analysts had been facing as we headed into the earnings results.

SA Premium

Since the start of 2023, analysts had been steadily downgrading Microsoft's consensus revenues, at the same time as investors were clamoring for its stock. And now?

I believe that in the coming few days, we'll see countless analysts upwards revising Microsoft's price targets.

Printing Free Cash Flows

Why is Microsoft one of the most valuable companies in the world? Not because of its ability to spin a carefully woven narrative. Rather, because of its ability to print impressive free cash flows.

More specifically, Microsoft's free cash flow margins reached 33%. Put another way, out of every $1 of revenues, Microsoft takes out of the business 33 cents of cash.

And unlike other tech businesses where management is taking home all that free cash flow as stock-based compensation, 85% of Microsoft's free cash flow is ''actual free cash flow'', after stock-based compensation, for shareholders.

The Bottom Line

The rapid takeaway here is that Microsoft is still in growth mode, being led by AI.

The more nuanced analysis would be quick to remark that investors are being asked to pay around 27x next year's EPS (ending June 2024). Obviously, that's not a cheap valuation.

But as you know extremely well, you don't get high-quality compounders cheaply. The investment is not a no-brainer, because everyone can understand that paying close to 30x forward earnings for a business whose bottom line is growing at roughly half of that, is not a cheap valuation.

But at the same time, unlike nearly all businesses I know, very few can turn their revenues into free cash flows at such a high margin. Perhaps there are about 5 businesses I know that can do this, but very few of those businesses are as nicely diversified and well-positioned for future sustainable growth.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities - stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

- Deep Value Returns' Marketplace continues to rapidly grow.

- Check out members' reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.

This article was written by

DEEP VALUE RETURNS: The only Marketplace with real performance. No gimmicks. I provide a hand-holding service. Plus regular stock updates.

We are all working together to compound returns.

WARNING: Any stocks that you feel like buying after discussions with me are your responsibility.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.