VBR: Small Cap Value Too Cheap To Ignore

Summary

- With a PE ratio of 12.2x, the Vanguard Small-Cap Value Index Fund ETF trades at a near 40% discount to the S&P 500, which is the largest discount seen over the past decade.

- I expect to see the VBR outperform the S&P 500 by around 1-4pp per year over the long term, depending on the extent of valuation mean reversion.

- While heavy financials exposure leaves the VBR susceptible to renewed credit stress, the intense underperformance already seen, combined with the steepening yield curve, has improved the outlook for the sector.

syahrir maulana

While I am bearish towards US large cap stocks, the small cap segment is actually attractively valued, and the small cap value segment is even more appealing. With a PE ratio of 12.2x, the Vanguard Small-Cap Value Index Fund ETF Shares (NYSEARCA:VBR) trades at a near 40% discount to the S&P 500, which is the largest discount seen over the past decade. Small cap value stocks are highly sensitive to recessions and credit stress due to their high exposure to financials, but at current valuations we should expect outperformance versus the broader market over the coming years.

The VBR ETF

The VBR seeks to track the performance of the CRSP US Small Cap Value index. The fund is dominated by industrials, which have a 23% weighting, and has an outsized weighting of financials at 20%. Consumer discretionary stocks make up a further 16%, followed by real estate at 9%. Technology has a weighting of just 6%, which is significantly lower than the S&P 500's 25%. The dividend yield on the ETF sits at 2.2%, which reflects an extremely low payout ratio of just 31% for the CRSP US Small Cap Value index. The expense ratio is just 0.07%, which is low for a targeted equity fund.

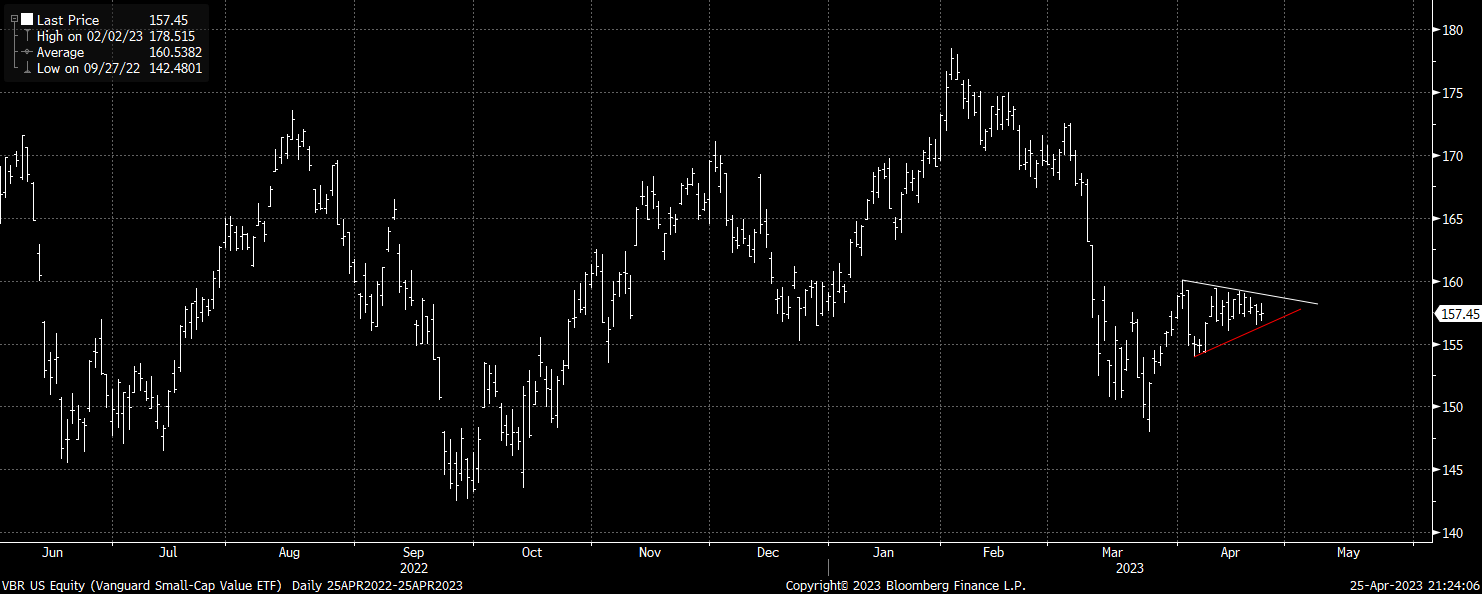

After trading at two-year highs versus the S&P 500 in early March, the VBR has since fallen to 14-month lows, weighed down by weakness in the financial sector. From a short-term perspective the VBR is trading in a tight contracting range, suggesting a breakout is likely. A close above $160 would suggest a resumption of the recovery, opening up a return to the $170 area, while a downside break would put the March lows at $148 in focus.

VBR ETF (Bloomberg)

Valuations Are 40% Below The S&P 500

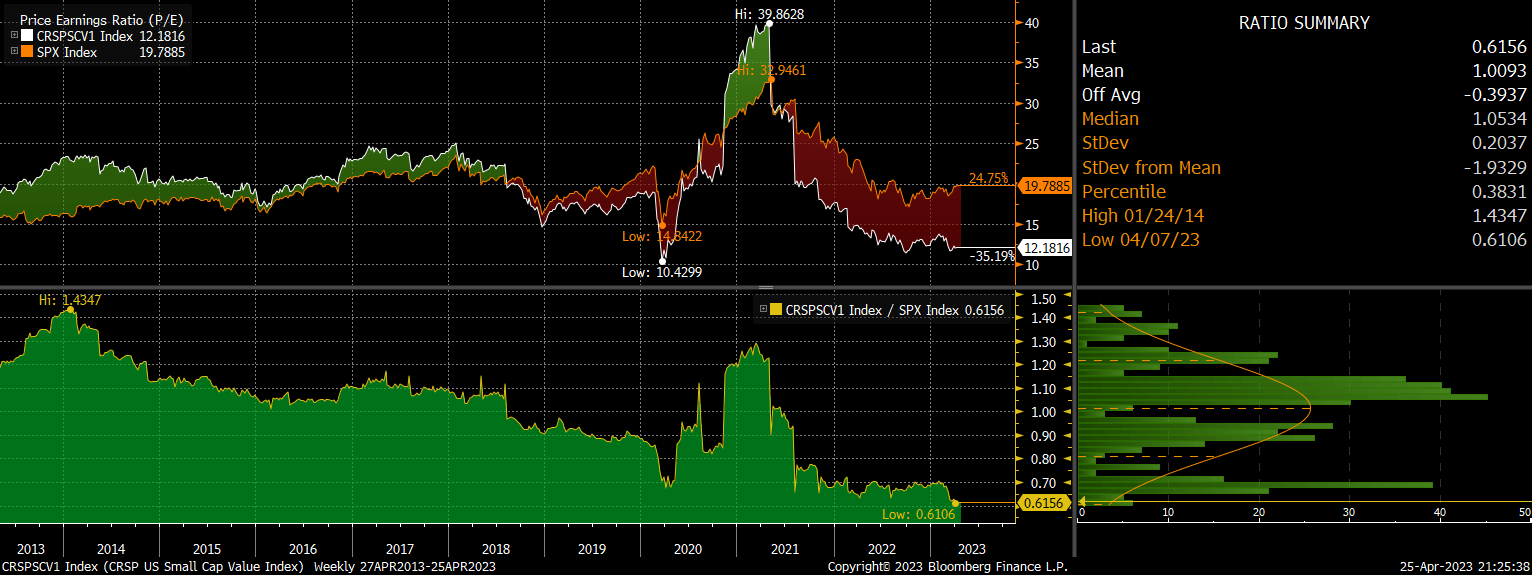

The trailing PE ratio on the CRSP US Small Cap Value index remains near its Covid crash lows at just 12.2x, which is almost 40% lower than the S&P 500. The EV/EBITDA ratio shows that small cap value is similarly undervalued relative to large cap stocks. As the chart below shows, this is the largest discount seen over the past decade.

VBR vs S&P 500 PE Ratio (Bloomberg)

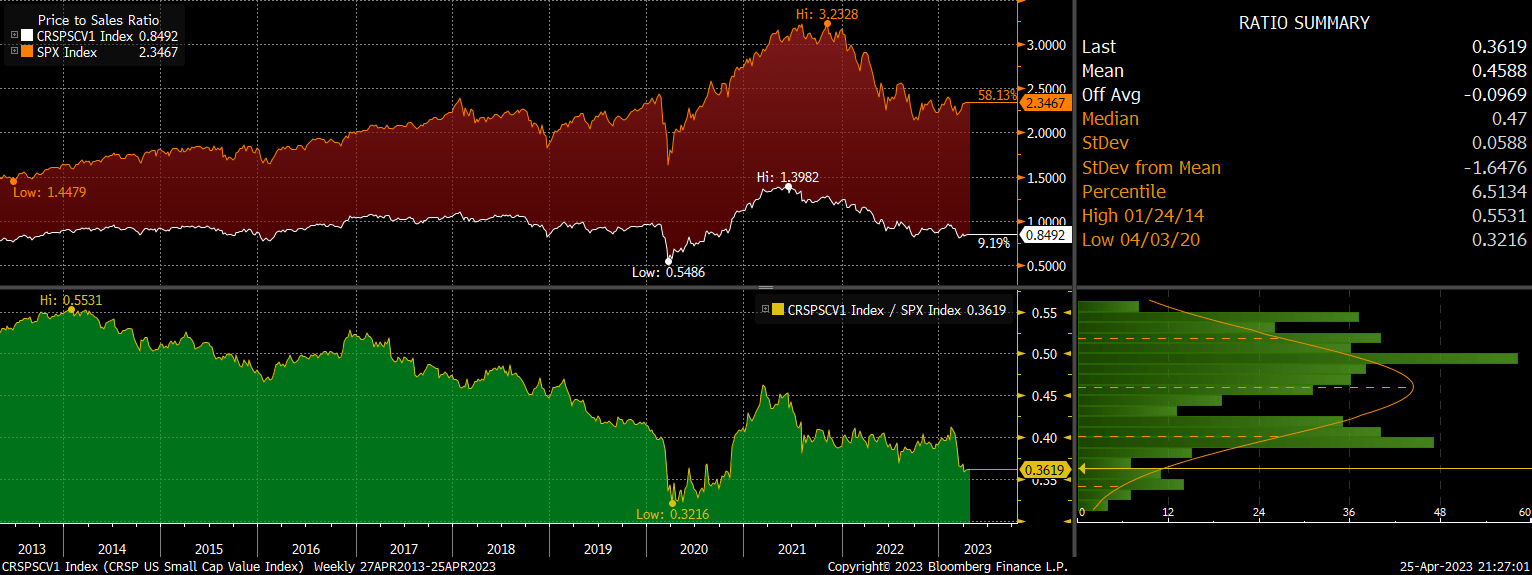

In part this deep discount on an earnings basis reflects the surge in profit margins seen over recent years, which have closed the gap relative to the S&P 500. However, even on a price/sales basis, the CRSP US Small Cap Value index trades at depressed levels on a relative basis. Even if we factor in downside mean reversion in profit margins over the coming years, we should still see small cap value outperform significantly on the basis of valuations.

VBR Vs S&P 500 PS Ratio (Bloomberg)

Even if the valuation discount remains in place, the SRCP US small Cap Value index should benefit from its higher dividend yield, which is 0.9pp higher than the S&P 500. Dividend growth for both indices has averaged around 7.5% annually over the past decade, and if both were to see the same growth rates in the future, small cap value should outperform by 0.9% annually. However, if valuations were to mean revert back to their 10-year average over the next decade, this would provide an additional 3pp annual outperformance in the VBR.

High Weighting Of Financials Poses A Risk But Outlook Improving

One of the key reasons for the extreme undervaluation in the VBR relative to the S&P 500 is the weakness in regional banks. With a weighting of 20% in the VBR, the performance of the financial sector is a key driver of the ETF. Small caps have a long history of underperforming during periods of recession and credit stress, and near-term risks are heightened as a result. However, after losing almost one third of its value relative to the S&P 500 over the past two months, regional banks have underperformed to a greater extent than during the global financial crisis and the Covid crash, suggesting the worst may be over for the sector. The steepening of the US yield curve over the past two months, thanks to the 100bps fall in 2-year Treasuries, may suggest easier financial conditions for US banks are on their way.

Summary

The VBR is too cheap to ignore, with a PE ratio of just 12.2x leaving the ETF extremely undervalued relative to the S&P 500. The weakness in the financial sector over the past few months has reversed much of the outperformance seen over the past two years and has provided another opportunity to take advantage of cheap valuations. While the heavy weighting of financials in the index leaves the VBR susceptible to renewed credit stress, the intense underperformance already seen, combined with the steepening yield curve, has improved the outlook for the sector. I expect to see the VBR outperform the S&P 500 by around 1-4pp per year over the long term, depending on the extent of valuation mean reversion.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of VBR either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.