Why Silicon Motion Technology's Stock Is A Good Hedge Against Potential Downside

Summary

- Silicon Motion's stock has nearly 80% upside if the MaxLinear deal goes through this year.

- The stock appears to have strong levels of support in the mid to low $50 range hinting at just 20% downside.

- This combination of relative valuation and M&A upside make SIMO a terrific investment in what may be tough investment times ahead in 2023.

GarysFRP

Silicon Motion Is A Buy Whether the Merger Deal Goes Through Or Not

Silicon Motion Technology's (NASDAQ:SIMO) stock has been on a tear over the past decade delivering nearly 500% returns since 2014. The company, based out of Hong Kong, is a leading developer of NAND flash controllers, which are used in a wide range of consumer and industrial applications as well as a leader in SSDs. Despite their strong performance, the stock is still attractively valued at current levels, trading well below sector averages. The company continues to benefit from robust demand for NAND flash memory, as well as favorable industry trends such as the transition to 3D NAND and the growth of IoT.

Figure 1. Silicon Motion operates throughout Asia creating innovative components under a variety of brands (Silicon Motion Webpage)

SIMO stock has significant upside if MaxLinear (MXL) can close on their deal in 2023 to merge the two entities with upside as high as ~75-80%, with an approximately $106 purchase price possible. The stock trades as if the deal has already fallen through with Silicon Motion trading at just a 10x price to earnings ratio, well below its historical average. In addition, the company is benefiting from strong customer demand, driven by the growth of mobile, IoT, and edge computing applications to top things off. The company is also focused on emerging markets such as automotive, industrial, and edge AI which could act as future catalysts. These markets are expected to drive future growth and the company is well-positioned to benefit from the increasing demand, despite analysts' predictions of a decline in earnings in 2023. We believe this combination of value, growth, and potential for short-term gain if the MaxLinear deal passes through is a fantastic bet in a bearish environment where any upside can be hard to find.

Valuation & Analyst Recommendations

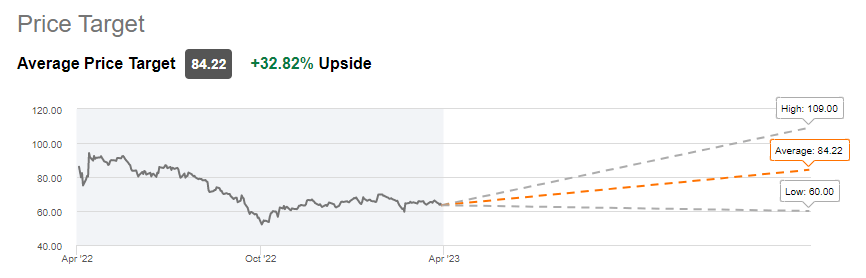

Analysts across Wall Street have given Silicon Motion a rating of hold or better with an average price target of $84.22, 35% above current prices (Figure 2). The company is widely seen as one of the most attractive foreign investments in the semiconductor sector if the buyout deal is successful, and as a fair investment even if the deal falls through. Analysts at Susquehanna have an optimistic outlook on the stock, with a bullish rating based on an attractive risk-reward profile. Similar sentiments have been expressed by Seeking Alpha contributors as well with 3.5, or buy, rating on the stock.

Figure 2. Wall Street analyst price targets put SIMO at a buy in tough investment climates for semis (Seeking Alpha Ratings)

The valuation of Silicon Motion Technology is positive on account of its strong performance in the semiconductor sector. As mentioned the stock is currently trading at a P/E of 10x earnings and has a price-to-sales (P/S) ratio of just 2.2x revenue which is considered to be attractive from both a historical average aspect as well as side by side to peers as well. Historically SIMO trades closer to a 14x P/E ratio looking at their 5 year average or closer to a 17x P/E looking further out at a 10+ year average. This would hint at 40-80% upside and lines up well with both price targets and the information technology sector median of 17.8x earnings. This unique combination of relatively fair valuation and merger upside makes SIMO a strong buy in what could be a rough 2nd half to the year with recession talks looming.

Risks To Consider

Silicon Motion's stock carries a few risks which potential investors should be aware of. A large chunk of the company's revenue is derived from its operations in China, making it exposed to ever present tensions between the US and China. The trade war between the two countries has had an impact on Silicon Motion's operations in the past, so if tensions between the two countries continue to increase, it will likely have a negative effect on the company's performance. In addition, the company's success is dependent on the success of its clients. If its clients decide to switch to other providers or cancel their contracts with Silicon Motion, the company's profitability could be adversely affected. Growth is anticipated to slow in 2023 which could indicate the stock is a bit of a value trap if the merger with MaxLinear does not go through. Silicon Motion's success is also dependent on the success of its new products. If the company is unable to effectively bring its products to market, it could limit the company's growth.

SIMO has little to no debt according to their balance sheet. This is a major positive in a high interest environment and is one less risk to weigh going forward. Downside if the merger deal falls through is likely less than 20% with 52-week lows around the $52 range providing support. That sets up a very nice nearly 1:4 risk vs. reward ratio for the stock trading around the low $60 range. Even if the merger is drug out we see this as a very strong buy in the current macroeconomic environment.

Conclusion

As previously stated, Silicon Motion is a company that is well positioned for future growth. Its focus on developing innovative products and services in the consumer electronics market has paid off for shareholders and is likely to continue to do so in the future. It is a company that is well positioned to benefit from the ever-expanding demand for consumer electronics. The company has tremendous upside (~75-80%) if the MaxLinear deal goes through. Even if the deal is denied or drug out, downside risk is likely less than 20% due to the intrinsic value of the stock at current prices.

Nevertheless, there are some risks that potential investors should consider. The company's dependence on China and its customers, as well as its ability to compete with other companies in this rapidly-evolving sector, could have an impact on the company's performance in the future and in turn how the stock is perceived. In conclusion, Silicon Motion's stock is a good buy at current levels for investors who understand the company's business and are comfortable with the risks associated with it. Support by Silicon Motion's proven execution and ongoing product innovation should help it weather any potential headwinds in the future and we believe the stock is set up to perform no matter what macroeconomic market conditions are thrown its way.

Editor's Note: This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SIMO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.