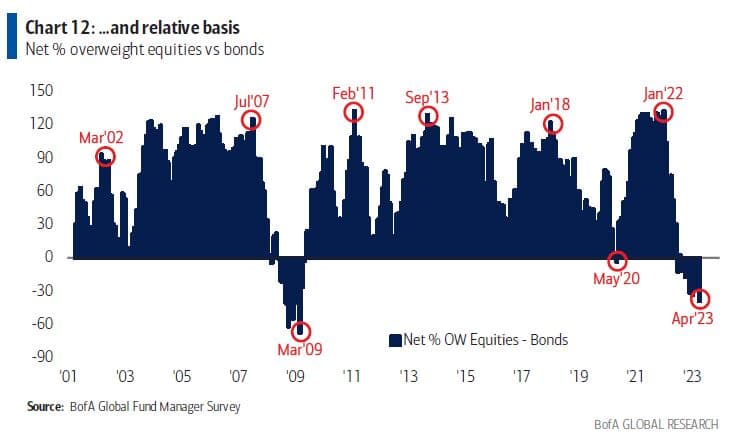

Investors' allocation to equities relative to bonds has dropped to its lowest level since the global financial crisis as worries about a recession take hold, according to Bank of America Corp.’s global fund manager survey.

In the most bearish survey of this year — the first after banking turmoil roiled markets last month — investors indicated that fears of a credit crunch had driven up bond allocation to a net 10 percent overweight — the highest since March 2009. A net 63 percent of participants now expect a weaker economy, the most pessimistic reading since December 2022.

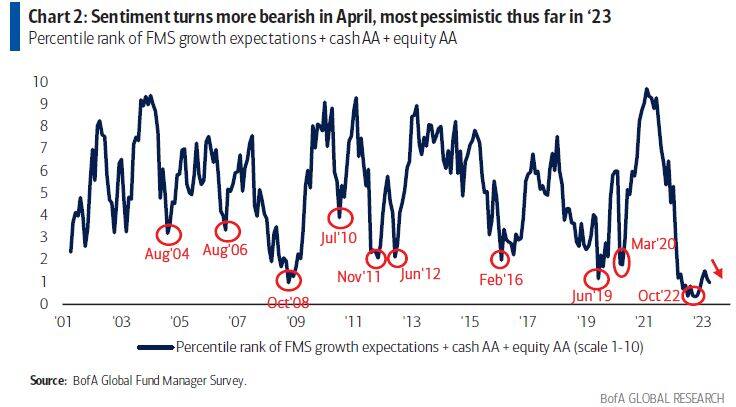

Still, the bearish turn in sentiment is a contrarian signal for risk assets, strategist Michael Hartnett wrote in the note. If “consensus lust for recession” isn’t satisfied in the second quarter, the “pain trade” would be a rally in bond yields and bank stocks, he said. Hartnett was correctly bearish through last year, warning that growth fears would fuel a stock exodus.

US stocks have bounced back from last month’s lows that were sparked by the collapse of some regional US lenders, including Silicon Valley Bank. Still, the rally has moderated this month as data show a softening in the labour market, fueling worries that the economy could contract later this year.

US stocks have bounced back from last month’s lows.

US stocks have bounced back from last month’s lows.

A credit crunch and a global recession are seen as the biggest tail risks to markets, followed by high inflation that keeps central banks hawkish. A systemic credit event and worsening geopolitics are also among the risks, according to the survey, which ran between April 6 to 13 and canvassed 249 participants with $641 billion in assets under management.

Other highlights from the survey include:

- About 84 percent of respondents see a pullback in global consumer price inflation, while 58 percent predict lower short-term rates, the most since November 2008

- About 80 percent expect the US debt ceiling to be raised by September

Cash allocation has remained above 5 percent for 17 consecutive months — second only to the 32-month dot-com bear market - A net 49 percent of investors expect IG bonds to outperform HY bonds over the next 12 months — the most on record

- US/European commercial real estate is seen as the most likely source of a credit event, followed by US shadow banking, US corporate debt and a Treasury debt downgrade

- Most crowded trades: long big tech stocks (30 percent), short US banks (18 percent), long China equities (13 percent), short REITs (12 percent), long European equities (11 percent), long US dollar (5 percent).