KBWB: The Big Bank Trade Is On

Summary

- The large bank sector and the regional bank sector (priced via KBWB and KBWR) have depreciated by similar levels year-to-date.

- Yet, it appears that deposits are flowing to larger banks because of a 'flight to safety' in the banking sector; JPM's latest earnings report was hard proof of this.

- As this effect continues, large, diversified banks should steadily accrue a larger portion of overall deposits and outperform their regional peers by a larger margin.

- All of this will occur against the backdrop of rising rates, which is a major profitability driver for banks - indicating a secular bull case in addition to the relative value shift.

- Taken together, this constitutes what I am calling the 'big bank trade' for this year, which can be implemented readily through the ETFs KBWB and KBWR.

scanrail

Overview

Earlier today, JPMorgan (JPM) and Citigroup (C) smashed earnings, indicating that there is still plenty of action to be found in the banking sector. This has led to immediate appreciation in Invesco KBW Bank (NASDAQ:KBWB), an ETF tracking large banks in particular. This article will compare it to KBWR, an ETF tracking regional banks and posit a trade that takes both of these into account.

This earnings beat may have surprised many investors I thought that it makes perfect sense. This is because of my belief that we are undergoing a wholesale deposit transfer and overall customer preference shift towards the largest banks - a 'flight to safety', if you will. This was of course catalyzed by the failure of Silicon Valley Bank.

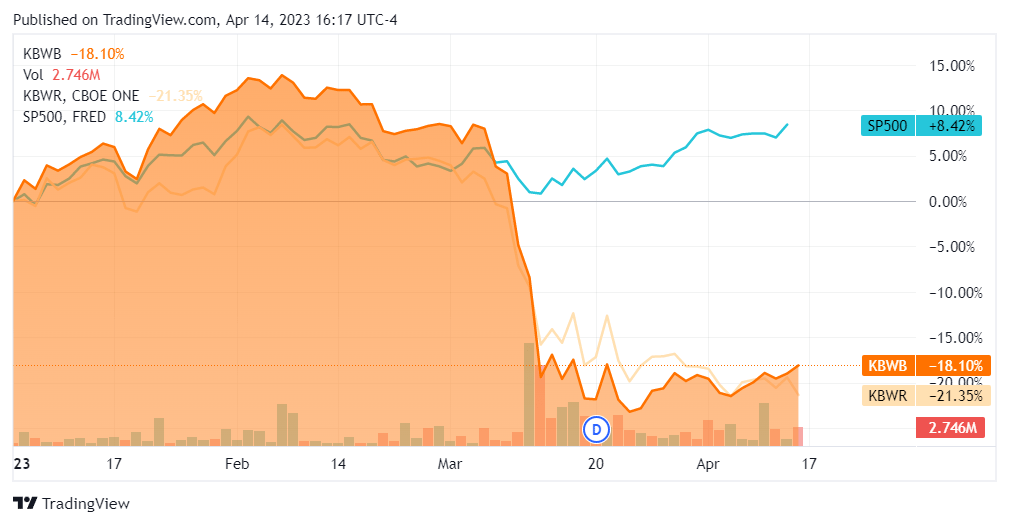

The markets response to this event, however, appears to have been relatively blunt thus far. The banking sector as a whole has been strongly affected by the news cycle so far this year and has depreciated across the board. This is evidenced by the fact both the Invesco Bank ETF as well as the Invesco Regional Bank ETF have been sold off well in excess of the S&P 500.

Notice, however, that the big bank ETF and the regional bank ETF are only 3.25% apart in terms of price performance (as of market close Friday). That's not an overly significant discount; in fact, we could even consider it statistical noise for a relatively busy trading day.

Seeking Alpha

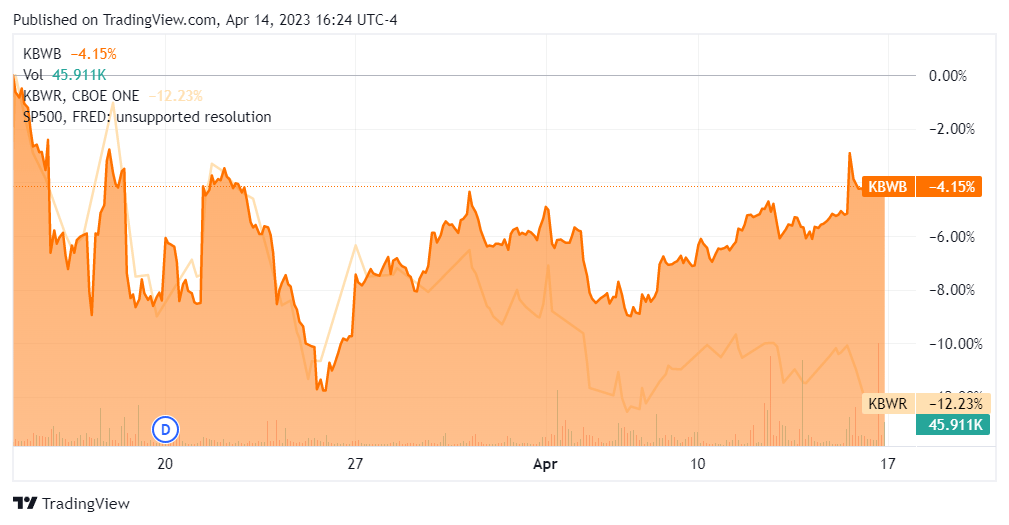

Looking at these two ETFs over the past month, things start to look a bit more refined; the regionals have actually depreciated 3 times as much as the large banks.

Seeking Alpha

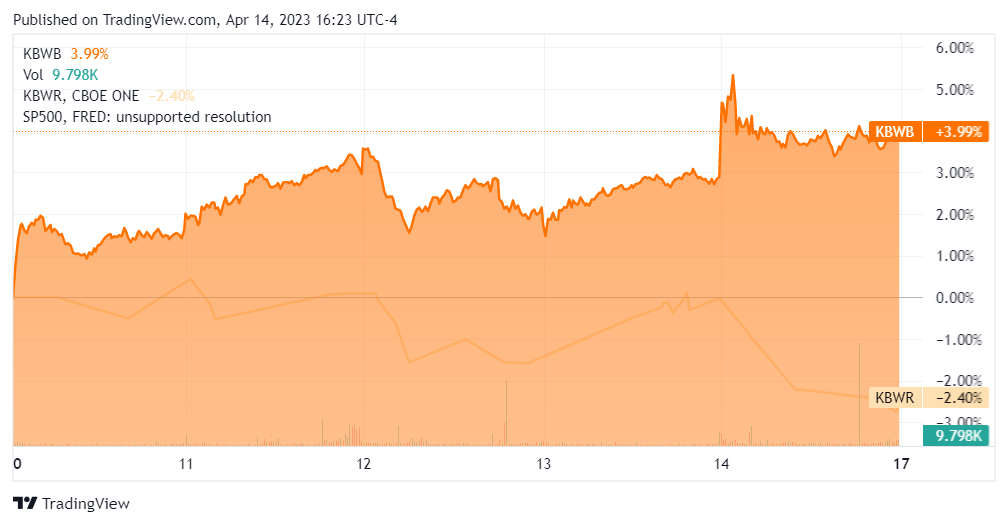

When we then zoom in even further and look at trading over this past week, the difference becomes even more stark. In the wake of JPM's and Citigroup's earnings, there is now a directional difference between the two ETF's. KBWB is up, while KBWR is down. This is because JPM and Citigroup are KBWB's top 2 holdings and 19.01% of their total market capitalization. This looks like the beginning of 'the big bank trade' to me.

Seeking Alpha

The Rationale Against Regionals

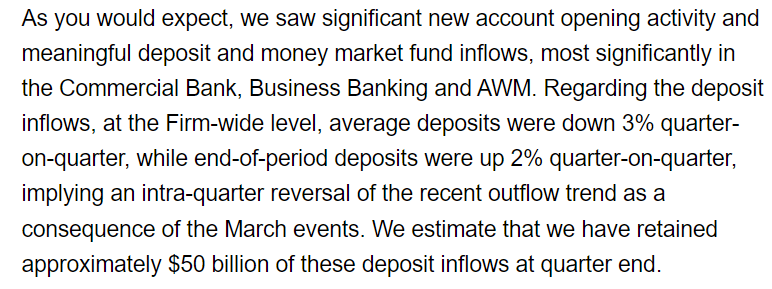

As I mentioned, I think there is an ongoing deposit rebalancing occurring in the banking sector. Businesses, and perhaps even some consumers, were rightfully spooked by the blow-up of SVB. Now they are looking to transfer their assets into entities that they can trust. For banks, that means the bigger, the better. We can corroborate this by reviewing a snippet from the JPM earnings transcript. Here, the CFO details exactly what occurred:

'an intra-quarter reversal of the recent outflow trend as a consequence of the March events'

Seeking Alpha

Basically, this means that JPM got hit with the same deposit drawdowns that everyone else did - but saw its situation reverse. Furthermore, it ended the quarter up on deposits, with end-of-period deposits having increased 2% quarter-over-quarter. While JPM is known as a standout and a 'fortress', I think some of this is due to its sheer size and diversification - the 'size factor'.

The size factor is something that other megabanks can claim - and they should be seeing a similar pattern in their flows for this past quarter and throughout this year. Indeed, Citigroup came in flat on deposits for Q1 2023. While this wasn't as good as JPM, I am willing to bet it was a lot better than sector average. I expect to see something similar across the large banks as they release earnings over the next 2 weeks.

Citigroup

I believe this deposit activity will continue as such throughout the year. We are undoubtedly in a period of increased economic uncertainty; inflation is consistently high and a lot of the smart money expects us to enter a technical recession in Q3 or Q4 of this year. This negative economic backdrop, combined with the recent SVB catalyst, makes it quite sensible for businesses and high-net-worth individuals to move their deposits into institutions that they can trust.

Furthermore, we should consider the fact that rising rates are actually good for banks: they mean higher interest rates on credit cards and usually a higher spread on other products. JPMorgan's net interest income went up a whopping 78% YoY. Consequently, this makes the sector a good one from a macroeconomic perspective - but only if you can hold on to your deposits.

Seeking Alpha

Conclusion

The trade here is clear-cut from my view. Big banks are going to get a larger proportion of deposits throughout the year. They will also continue to profit from the increase in interest rates, while also continuing to capture economies of scale inherent in their business. All of this will lead to a larger spread between the prices of the big banks and the regionals, which will be neatly reflected in their respective ETFs. As such, I am calling KBWB a buy and KBWR a sell.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.