Farnam Street Investments April 2023 Client Letter

Summary

- Farnam Street Investments is a Registered Investment Advisor with the State of CA. We are always challenging the status quo and bring independence of thought to everything we do.

- With interest rates rising, stubborn inflation, and surprise bank runs, markets are rightfully a little wobbly.

- Below is a list of core investment principles I’ve collected so far - I hope to keep adding as I gain a better understanding of the world.

Dragos Condrea/iStock via Getty Images

With interest rates rising, stubborn inflation, and surprise bank runs, markets are rightfully a little wobbly. Whenever the fear of panic is in the air, it’s best to get back to basics. Focus on what we can control. Prepare for opportunity.

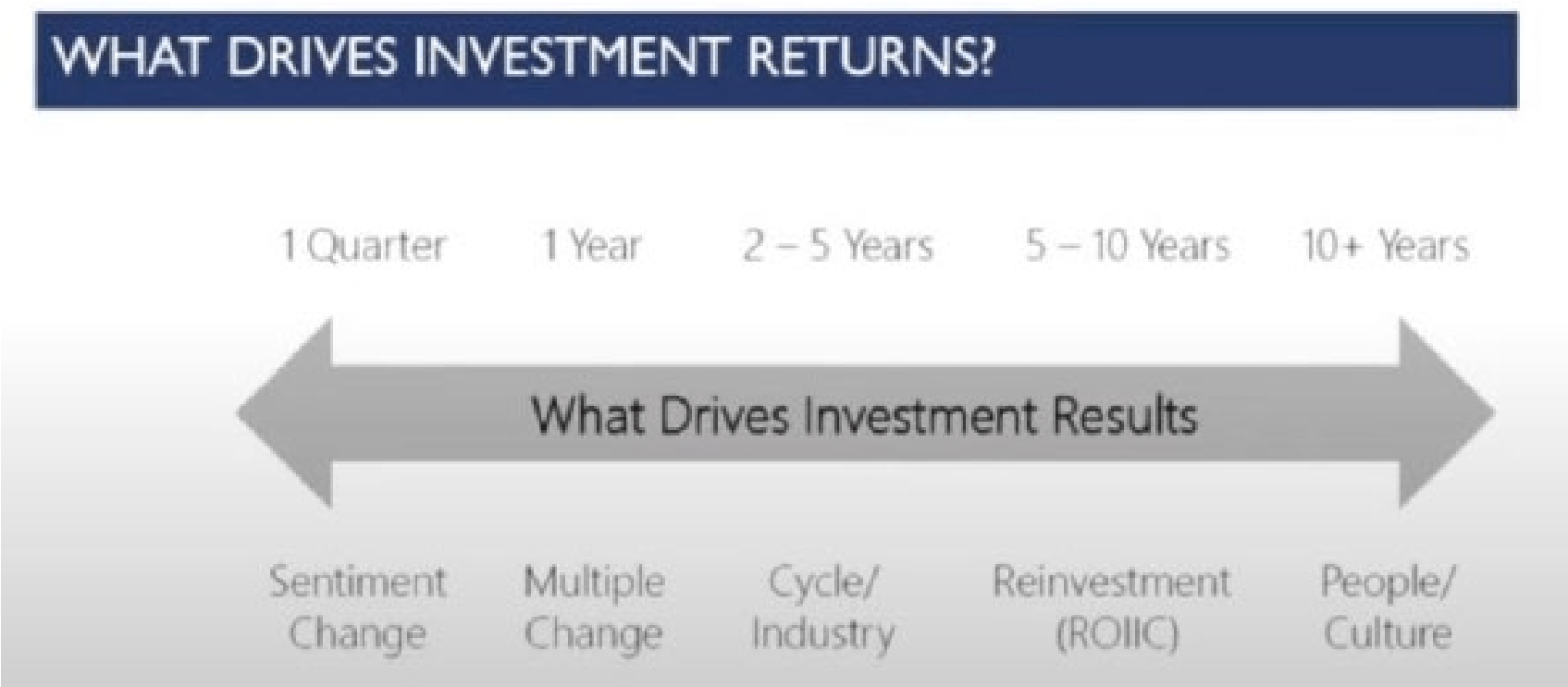

Below is a list of core investment principles I’ve collected… so far. I hope to keep adding as I gain a better understanding of the world.

Core Investment Principles

Defense wins championships. Financial defense means spending less than you earn. Keep realistic lifestyle expectations to create incredible resilience to life’s vicissitudes. Don’t expect the offense of outsized returns or income to bail out profligate spending.

Stocks aren’t squiggly lines. They represent ownership of businesses.

Owning productive assets is the most consistent way to maintain and increase your global purchasing power. Real businesses, providing real goods and services which forge the material progress of man, will always be the fountain of wealth.

Investment is most intelligent when it is conducted in a businesslike fashion.

Buy at the right price to gain the most dependable margin of safety. The catch is, there will be long stretches where you can feel out-of-step and have little to buy when prices appear high. Maintain vigilance; opportunities always return eventually.

Everything in markets happens in cycles. Never forget, or your reminder will be expensive. Human fear and greed drive these cycles.

You’ll hear “Cash is trash!” as often as you’ll hear “Cash is king!” Ignore these extreme proclamations. Cash represents a call option on buying future business value.

Markets can be stimulating, but your investing should be boring. Excitement is an expensive request of any portfolio.

An asset is worth the sum of the cash flow returned to its owner from now until Judgement Day, discounted by an appropriate rate. Don’t let ephemeral low rates drop your internal hurdle rate.

A “win-win” mentality for all constituents (customers, suppliers, employees, regulators, communities they operate in, owners) represents the only path toward corporate survival. If a company cheats any of those parties, eventually there will be a defection and the consequences will risk the company.

Most public companies fail at “win-win” relations and are therefore ineligible for long-term ownership.

Beware of agency costs and institutional imperatives. Much apparent irrationality you see can be explained by poorly aligned incentives and “But everyone else was doing it…”.

Stay within your circle of competence. If you have to ask if something is in your circle, then it isn’t.

Sometimes assets trade like apartments (based on cash flow), sometimes like Rembrandts (what the next person is willing to pay).

Bonds are sensitive to changes in interest rates. The longer the duration, the greater the impact of rates. Bonds are also subject to credit risk. Return of principal is as important as return on principal.

Most of the time, the stock market is reasonably efficient. Yet there are times when it completely disconnects from reality. Therefore, it’s important to remember that the market doesn’t tell you what your assets are worth. It only provides the most recent price, and the crowd’s implied expectations about the future. It’s your job to surmise what assets are worth based on the prospects of the business.

Markets are forward looking. This makes them capable of incredible, seemingly-illogical movements, especially over the short run. Keep a healthy emotional distance. Panic is contagious.

Buying with the intention of selling to someone later at a higher price is speculation. This strategy can appear to work for quite some time, but eventually you run out of greater fools. Avoid these zero-sum situations.

Any impressive string of returns multiplied by zero still equals zero. Follow “Buffett’s Rule #1: Don’t lose money” as much as possible. Never unnecessarily interrupt the power of compounding.

There are five “Deep Risks” that lead to the permanent loss of wealth.

- Severe and prolonged inflation.

- Severe deflation from economic depressions.

- Confiscation via taxes and nationalization.

- Devastation from acts of God.

- Business failure.

| Note: Quotational price movements are not on the above list. |

Short-termism is the human condition. There’s less competition when looking at 5+ year time horizons. But don’t underestimate the difficulty in being alone while focusing on that long-term.

Technology is amazing, but in the long run, everything is a toaster. Capitalism is relentless at stealing producer surplus and turning it into consumer surplus.

There’s a constant struggle between the overconfidence of significant position concentration and watering down a portfolio with too much diversification. Do the best you can to find the sweet spot.

Regression to the mean is a force of nature. On rare occasions, it really is different this time though. But it doesn’t typically pay to bet that way.

Sell criteria are hard, but here are four possible reasons to sell:

- The facts no longer support your thesis. Or your initial thesis was just plain wrong.

- The price advances so far ahead of the business results that future returns have been pulled forward already.

- The position has grown to be so large in the portfolio that you can’t sleep well at night.

- A more attractive opportunity deserves the capital.

Macroeconomics belongs in the “Too Hard” pile. Yes, it’s vitally important, but it’s too unpredictable to be depended upon for decision-making.

The markets and the economy are complex adaptive systems, more akin to a forest than a washing machine. Emergent behavior exists on the edge of chaos and is practically impossible to predict. There are non-linearities, tipping points, sand-pile effects. Something that doesn’t appear sustainable can go on for longer than you’d ever imagine, and then suddenly collapse.

You can’t know when the avalanche will kick off. But you can usually avoid standing below a huge pile of snow.

Markets and economics don’t fit “normal” Gaussian distribution curves. The tails are fatter, meaning there are more surprises lurking than most anticipate. Once-in-a-thousand-year events occur regularly. Hence conservative positioning with the aim of resilience is the winning approach.

Said more simply, select resilience over optimization. Survival is the supreme goal.

Complexity is the enemy. Avoiding obvious stupidity is easier than striving for genius.

Journaling provides an antidote to all sorts of behavioral biases. Crystalizing your thoughts suppresses hindsight bias.

Patience is the only sustainable competitive advantage. Whoever has the longest timeline wins.

Always conduct your affairs so you can play out your hand. That means never employing leverage, even if you have to forego “obvious” opportunities. You may be eventually right, but the path to get there can take you out of the game.

As race car driver Niki Lauda said, “The secret is to win going as slowly as possible.”

Have a “Man Overboard” plan ready. You will be tested. Use procedures to keep your head when others are losing theirs. “This too shall pass” is sage advice.

No one style of investment management stays in fashion forever. Lose with equanimity, stay humble when you’re winning.

Small, cheap, quality, and momentum are promising statistical factors which arbitrage human behavior. They have a long history of working better than average, but they don’t work all the time. Simple models regularly beat experts.

Absolute returns are lost chasing relative returns. Don’t reach for yield.

No position should ever be so large you can’t sleep well at night.

Take no one’s word for it. Trust, but verify.

Once you’re over an IQ of 120, your EQ becomes much more important. Temperament wins the investment game. Proper habits, environment, process, structure, mindset, and biological inputs can maximize your temperament.

Think more than you calculate. Higher math is never necessary.

There’s no special scoring for degree of difficulty in the investment world. Great returns can come from clearing 1-foot bars.

There’s always something to work on, but your buying and selling activity should be very infrequent. If it isn’t a no-brainer, take a pass.

Jason Zweig’s Seven Virtues of Great Investors

- Curiosity

- Skepticism

- Independence

- Humility

- Discipline

- Patience

- Courage

Quick Housekeeping Item

Part of being a registered investment advisor with the State of California means providing compliance updates and disclosures annually. Here’s where we keep the most up-to-date documents for our clients.

As always, we’re thankful to have such great partners in this wealth creation journey.

Jake

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.