SPY: Early CPI Euphoria Dissipated

Summary

- The early euphoria in pre-market trading about the March CPI report has dissipated as the S&P 500's near-term momentum stalled (again) at a critical juncture.

- We assess that the tech sector (26% of SPY's weighting) is looking increasingly likely to pull back soon.

- Investors need to be tactical with the SPY and consider well-battered sectors that have yet to see their valuations normalize.

- We view the S&P 500 as fairly-balanced for now.

- I do much more than just articles at Ultimate Growth Investing: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Torsten Asmus

Today's (April 12) CPI release led to an initial wave of optimism in pre-market trading that quickly dissipated. The S&P 500 Index (SP500) has continued to stall at its December 2022 bull trap highs or false upside breakout.

The 410 level on the SPDR® S&P 500 ETF Trust (NYSEARCA:SPY) rejected bullish advances in February and has stalled the SPY's advance since last week. While a near-term top cannot be ruled out, the risk/reward of a sell signal doesn't seem to be favorable enough.

What drove the initial pre-market optimism that saw the S&P futures up more than 1% in pre-market trading before the sellers returned for a reality check?

March's CPI release by the Bureau of Labor Statistics or BLS showed that headline inflation had moderated further to a below-consensus 5% YoY, down from last month's 6% uptick.

However, core inflation remains high, as seen by the 5.6% YoY increase relative to February's 5.5% growth. Despite that, the market cheered initially, as it saw a consistent decline in the headline metric, corroborating a downtrend in inflation rates since June 2022's highs.

But, sellers returned to take profit, including hedgers who were likely covering their positions in anticipation of a worse release. Buyers caught up in the early optimism should have seen it coming. Why?

Market operators have likely anticipated a better-than-expected release since the SPY bottomed out in mid-March as the banking crisis peaked.

Therefore, the current levels (against a critical resistance zone) represent a solid opportunity to cut exposure, as underlying sector rotation could soon occur, with risk/reward fairly balanced, leaning to the downside in the near term.

Despite that, we don't expect a re-test of the SPY's October 2022 lows. The underlying breadth of risk-on plays, such as technology (XLK) and the Nasdaq (QQQ), has already climbed well above levels, inconsistent with a continuation of bear market behavior.

Investors considering adding exposure to the SPY are urged to be tactical, as we believe overheated sectors could see a rotation to undervalued ones, which could mitigate the potential upside at the current levels.

Why?

| Sector | Percentage |

|---|---|

| Technology | 26.32% |

| Health Care (XLV) | 14.71% |

| Financials (XLF) | 12.40% |

| Consumer Discretionary (XLY) | 10.16% |

| Communication (XLC) | 8.24% |

| Industrials (XLI) | 8.21% |

| Consumer Staples (XLP) | 7.24% |

| Energy (XLE) | 4.78% |

| Utilities (XLU) | 2.94% |

| Real Estate (XLRE) | 2.63% |

| Basic Material (XLB) | 2.37% |

SPY sector weightings. Data source: S&P Cap IQ.

As a reminder, the tech sector accounts for about 26% of the SPY's weighting. Therefore, anticipating the price action of tech and its relative valuation will likely be critical to assess the SPY's directional bias.

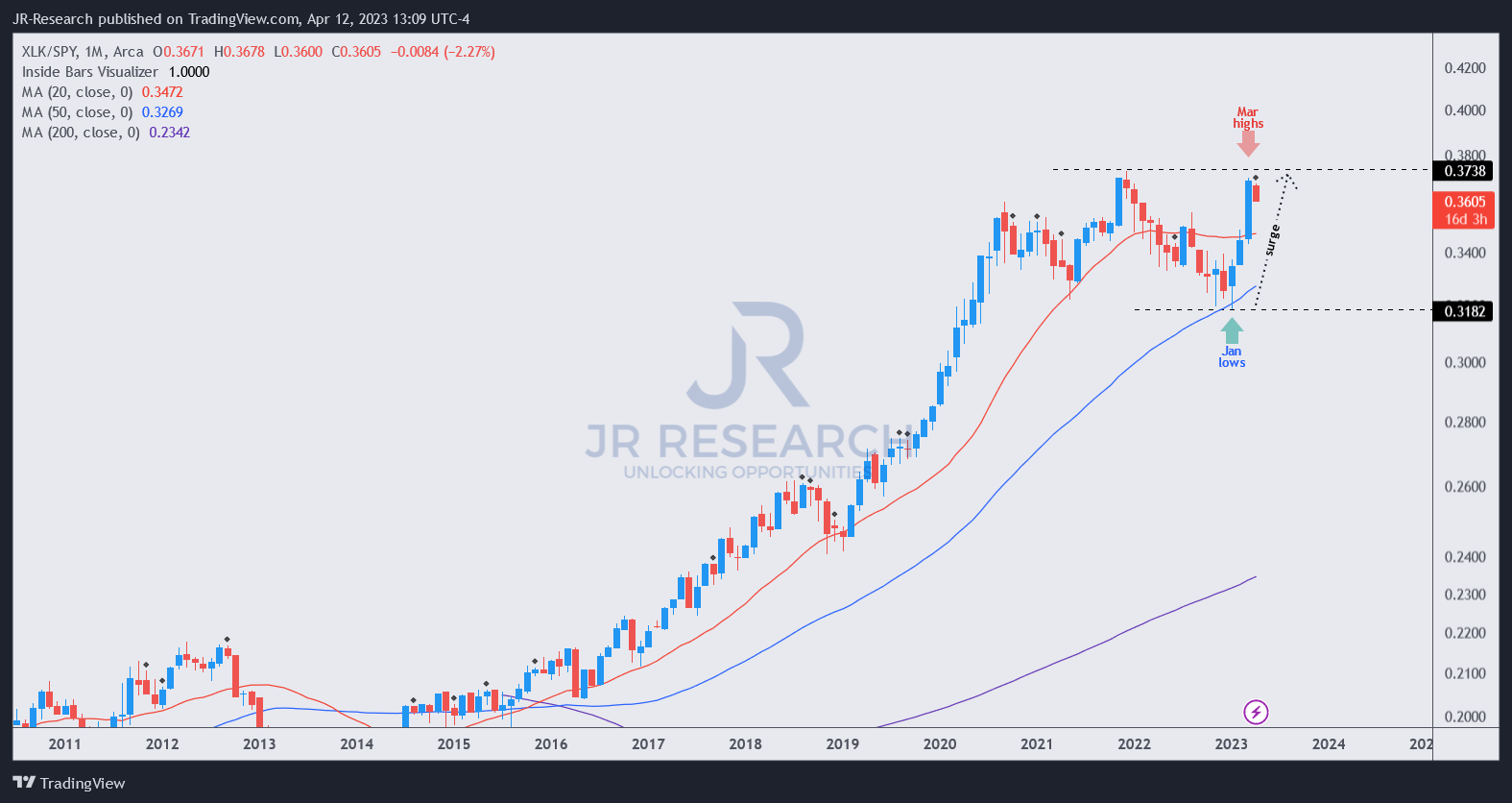

We assessed that the valuation dislocation of the XLK against its 10Y average has normalized. It last traded at a normalized P/E of 24.3x, in line with its 10Y average of 25.4x. So, while it's not expensive, it's also no longer that cheap.

XLK/SPY price chart (monthly) (TradingView)

Moreover, XLK/SPY's long-term price action could stall at the current levels, even though we are still short of a definitive bull trap. Despite that, caution is warranted, suggesting investors should not expect XLK to drive SPY's near-term momentum.

However, we gleaned opportunities in sectors such as XLV and XLF. The XLF is particularly attractive, suggesting that investors should find the opportunity for alpha after sellers went out through a stampede in March.

XLY and XLC remain well-battered as they continue to trade well below their long-term moving averages. Despite that, their near-term recovery momentum has seemed to stall after a remarkable turnaround since the start of 2023.

Takeaway

After a remarkable U-turn from its March lows, the SPY has reached the critical resistance zone again. Despite a better-than-expected headline CPI metric, the initial euphoria quickly ended as sellers returned to cut exposure.

With that in mind, we expect the SPY's near-term bias to continue facing resistance, with a pullback looking increasingly likely. However, we don't expect a return to a bear market, so investors with exposure can consider holding out through the volatility.

Investors looking to add more positions should be tactical and consider sectors within the SPDR® S&P 500 ETF Trust that offer a more favorable reward/risk upside.

Rating: Hold (Reiterated).

Important note: Investors are reminded to do their own due diligence and not rely on the information provided as financial advice. The rating is also not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have additional commentary to improve our thesis? Spotted a critical gap in our thesis? Saw something important that we didn't? Agree or disagree? Comment below and let us know why, and help everyone to learn better!

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA's bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!

This article was written by

JR research was featured as one of Seeking Alpha's leading contributors in 2022. See: https://seekingalpha.com/article/4578688-seeking-alpha-contributor-community-2022-by-the-numbers

Unlock the key insights to growth investing with JR Research - led by founder and lead writer JR. Our dedicated team is focused on providing you with the clarity you need to make confident investment decisions.

Transform your investment strategy with our popular Investing Groups service.

Ultimate Growth Investing specializes in a price action-based approach to uncovering the opportunities in growth and technology stocks, backed by actionable fundamental analysis.

We believe price action is a leading indicator.

Price action analysis is a powerful and versatile toolkit for the informed investor because it can be used to analyze any publicly traded security. As such, it offers investors with invaluable insights into understanding market behavior and sentiments.

Plus, stay ahead of the game with our general stock analysis across a wide range of sectors and industries.

Improve your returns and stay ahead of the curve with our short- to medium-term stock analysis.

We not only identify long-term potential but also seize opportunities to profit from short-term market swings, using a combination of long and short set-ups.

Join us and start seeing experiencing the quality of our service today.

Lead writer JR's profile:

I was previously an Executive Director with a global financial services corporation. I led company-wide award-winning wealth management teams that were consistently ranked among the best in the company.

I graduated with an Economics Degree from National University of Singapore [NUS]. NUS is Asia's #1 university according to Quacquarelli Symonds [QS] annual higher education ranking. It also held the #11 position in QS World University Rankings 2022.

I'm also a Commissioned Officer (Reservist) with the Singapore Armed Forces. I was the Battalion Second-in-command of an Armored Regiment. I currently hold the rank of Major. I graduated as the Distinguished Honor Graduate from the Armor Officers' Advanced Course as I finished first in my cohort of Armor officers. I was also conferred the Best in Knowledge award.

My LinkedIn: www.linkedin.com/in/seekjo

Analyst’s Disclosure: I/we have a beneficial long position in the shares of XLF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.