BLV: Balance Of Treasuries And Credit Risk Provides High Yield Relative To Risk

Summary

- The Vanguard Long-Term Bond ETF offers exposure to long-term US Treasuries and US credit in roughly equal measures, helping to reduce volatility relative to each component asset.

- The best-case scenario for BLV would be a decline in yields and continued narrowing of credit spreads, as we saw in 2019, when the fund returned 20%.

- Even in the event of a credit crunch, the BLV should still rise, as the impact of falling Treasury yields outweighs the impact of rising credit risk.

Andres Victorero

The Vanguard Long-Term Bond ETF (NYSEARCA:BLV) offers exposure to long-term US Treasuries and long-term US credit in roughly equal measures. With a 30-day SEC yield of 4.5%, the ETF is likely to post strong real returns over the coming years and should outperform its peers if we see mild declines in Treasury yields and narrowing credit spreads. Even in the event of a credit crunch, the BLV should still rise, as the impact of falling Treasury yields outweighs the impact of rising credit risk. Stagflation is the main risk as we could see rising bond yields coincide with widening credit spreads, but this is a remote possibility and the high real yield is ample compensation for such risks.

The BLV ETF

The BLV ETF seeks to track the performance of the Bloomberg US Long Government/Credit Float Adjusted Index. The fund has high maturity of 22.9 years, which is high for a bond fund. The duration is lower at 14.4 years, which partly reflects the impact of corporate bonds. 46% of the fund is invested in US Treasuries, 33% in industrial credit, and the remainder is spread across foreign, finance, and utility sector bonds. The current yield is 4.5%, which is around 75bps above equivalent maturity US Treasuries and 2.2% above long-term inflation expectations. The BLV is less volatile than similar maturity Treasury funds due to the lower duration of the fund and the tendency for credit spreads to move inversely with bond yields. The expense ratio is just 0.04%.

Balanced Portfolio Reduces Volatility And Downside Risks

High-grade corporate bonds have outperformed Treasuries by around 90bps annually over the past 20 years and should continue to outperform over the long term. However, this outperformance has come at the cost of higher downside volatility, with the Bloomberg US Corporate Credit Index losing in excess of 20% during the global financial crisis and again in the Covid crash. This downside risk during periods of financial crisis is typically not desirable for a bond fund, as most investors use bonds as a way to hedge against downside risk in equities and other risk assets.

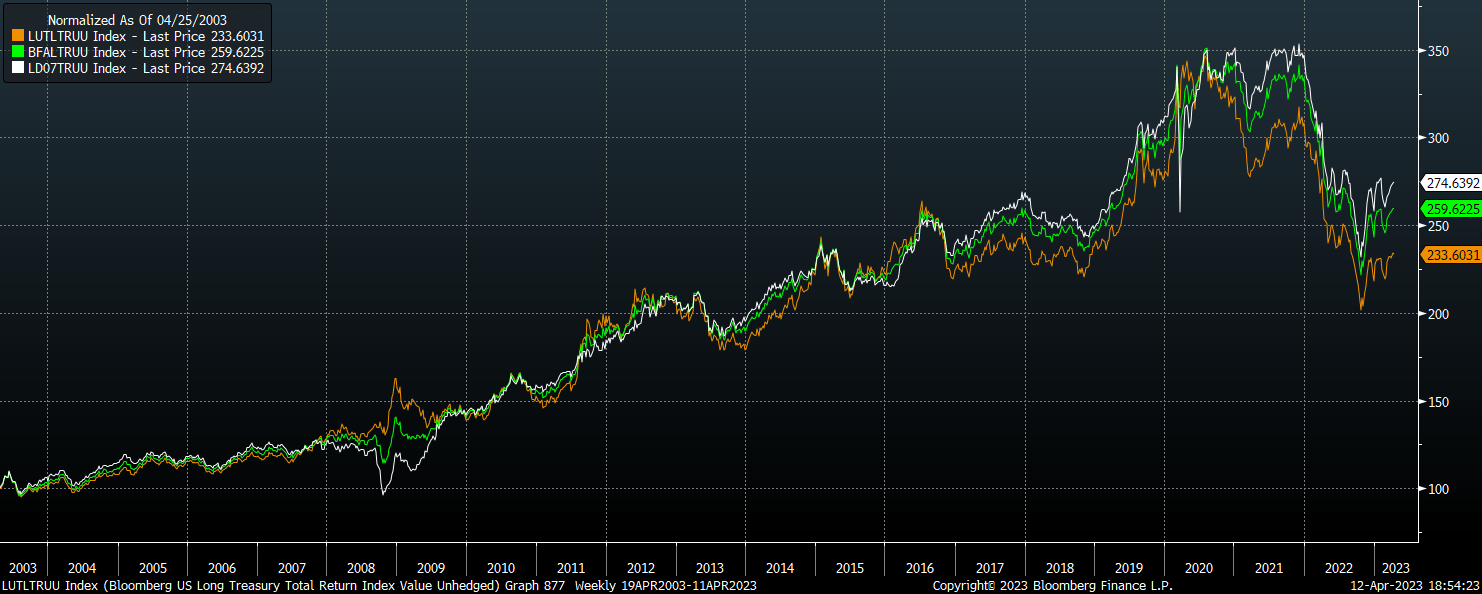

Orange: US Long Treasury Index. Green: US Long Government/Credit Index. White: US Corporate Index (Bloomberg)

In contrast, long-term US Treasuries have shown higher downside volatility during periods of rising yields, as the lack of exposure to credit risk has reduced the support of improved risk appetite on corporate bond prices. The Bloomberg Long Treasury Index lost a whopping 43% from March 2020 to October 2022, and any renewed upside in inflation expectations could cause long-term Treasuries to continue underperforming.

The Bloomberg US Long Government/Credit is a good middle ground, exposing investors to less credit risk relative to corporate bonds in the event of a credit crunch and less interest rate risk compared to Treasuries in the event of a renewed rise in yields. The best-case scenario for the BLV to outperform would be a gradual decline in yields and continued narrowing of credit spreads. From an economic perspective, we would likely need to see weak but still-positive real economic growth and continued declines in inflation. I believe the risks are tilted to the downside as high debt levels, weakening growth, and still-high real borrowing costs raise the risk of a credit crunch. However, even in the event of a credit crunch, the BLV should still rise as the impact of falling Treasury yields outweighs the impact of rising credit risk, as was the case during the global financial crisis in 2008 and the Covid crash of 2020.

Stagflation Is The Main Risk, But High Yield Provides Ample Margin For Error

The main risk comes from stagflation, which would be negative for both US Treasuries and corporate bonds. Stagflation is characterized broadly by low or falling real economic growth combined with high and rising inflation. While this dynamic was in play for much of the 2021-2022 period, and most of the 1970s, it is unlikely to be a dominant trend over the coming years. Periods of economic contraction tend to occur alongside declining demand for credit and a rise in demand for cash and government bonds, which tends to drive down inflation, outweighing the inflationary impact of reduced real output.

While I can foresee that continued high government spending may eventually lead people to view cash and government bonds as a superior asset even during periods of financial panic, there is no evidence that the link between inflation and risk appetite will break down any time soon. Even if we do see rising inflation and rising credit spreads, the BLV's 4.5% yield is already 2.2% above 20-year breakeven inflation expectations, which is 50bps above its 10-year average. It would therefore take a significant rise in inflation expectations in order for real returns on the BLV to be negative over the coming years. In a best-case scenario, on the other hand, continued declines in UST yields and narrowing credit spreads could easily see the BLV return 20% over the next 12 months, as was the case in 2019.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.