Valero Energy: A Strong Undervalued Refiner

Summary

- Valero Energy Corporation is a leading refiner with strategic locations, a strong focus on renewable diesel, and refinery complexity, enabling it to capitalize on cost advantages.

- Valero Energy's proactive investments in renewable diesel and refining optimization projects aim to increase annual EBITDA by up to $1.7 billion without relying on improved market conditions.

- Valero has a consistent strategy of returning cash to its shareholders through dividends and share buybacks.

- A potential catalyst in obtaining an exemption to import Venezuelan crude oil could further enhance Valero Energy Corporation's competitive edge and boost profitability.

- I value the shares at $189.

zorazhuang

In this article, I will discuss the Valero Energy Corporation (NYSE:VLO) competitive advantage in the refining industry thanks to its high-quality refining assets. As the largest independent refiner and a leading renewable diesel and ethanol producer, VLO's ability to process different types of crude oil, its focus on renewable diesel and margin improvement projects, and VLO's dedication to delivering shareholder value are some of the key aspects that make it an attractive investment opportunity. Furthermore, the potential catalyst of gaining a Chevron-style exemption to purchase Venezuelan crude oil could significantly impact VLO's profitability. I value Valero Energy Corporation shares at $189.

High-Quality Refining Assets and Strategic Location

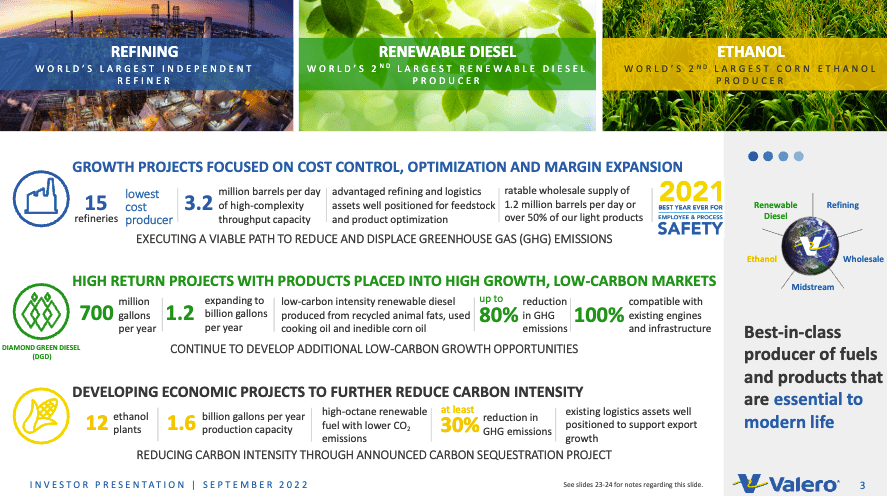

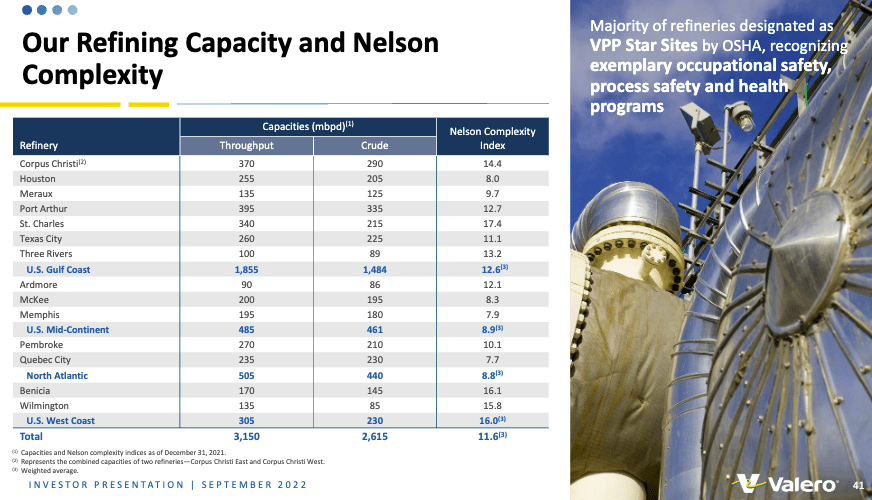

Valero Energy Corporation is the largest independent refiner globally, managing 15 refineries in the U.S., Canada, and the UK. Its daily throughput capacity reaches 3.2 million barrels. Moreover, VLO is the second biggest renewable diesel producer worldwide, generating 700 million gallons annually. Additionally, it boasts 12 ethanol plants, making it the second-largest corn ethanol producer globally.

Company presentation

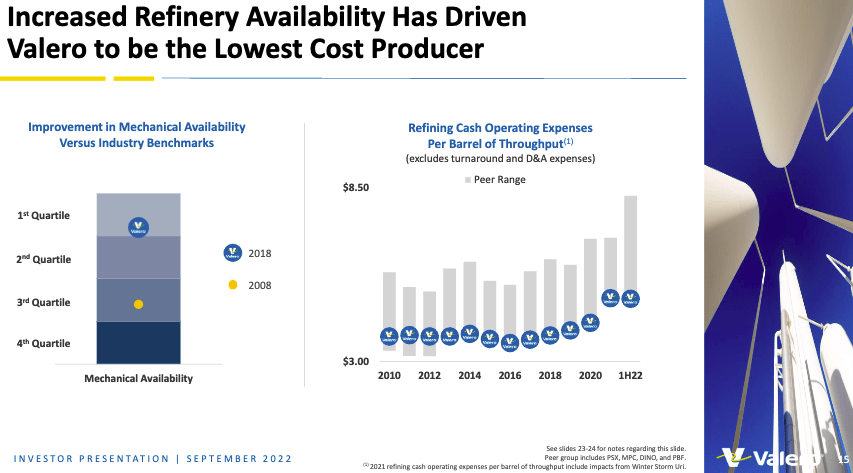

VLO's strategic location near cost-advantaged light crude oil sources and its ability to process discount heavy sour crude, combined with low operating costs from lower domestic natural gas prices, enables VLO to enjoy a cost advantage in the refining market. VLO's access to lower-quality feedstock and its complex assets concentrated in the Gulf Coast region enables it to process light or heavy crude, depending on which offers the greatest discount or optimal economics. This flexibility allows VLO to thrive in various market conditions and capitalize on the crude differentials that give U.S. refiners a cost advantage.

Company presentation

Focus on Renewable Diesel and Margin Improvement Projects

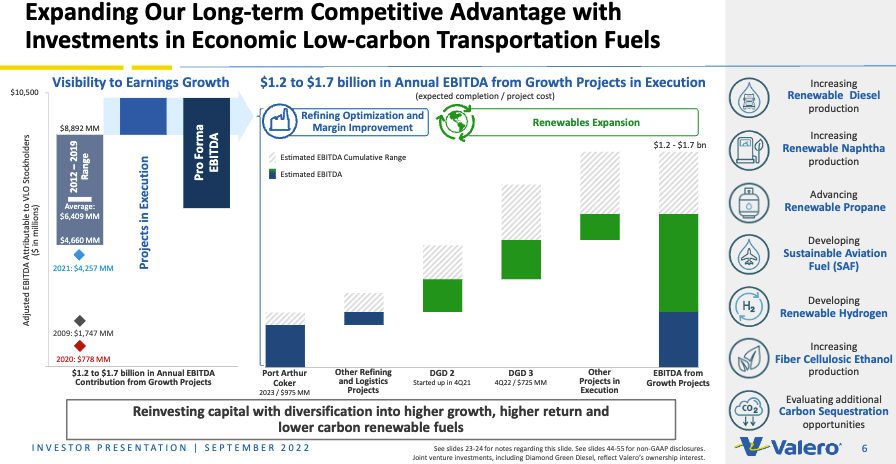

VLO has proactively invested in renewable diesel to increase volumes and capture attractive returns. By focusing on the growth of the renewable diesel business and refining optimization projects, VLO aims to increase its annual EBITDA by up to $1.7 billion a year without the need for improved market conditions.

Company presentation

Refinery Complexity - a competitive advantage

VLO's weighted average complexity of 11.6 makes it the most complex refiner in the U.S. where the average complexity is 9.5, allowing it to realize a cost advantage by processing cheaper, lower-quality crude as feedstock and increasing realized margins. Crude oil expense is the primary cost for refineries. They can boost profit margins by transforming lower-cost heavy crude oil into higher-value refined products. While heavy crude oil is cheaper to purchase, it is costlier to process. Refineries capable of handling inferior-quality oil can take advantage of the price gap between heavy and light crude oil, leading to increased profits.

Company presentation

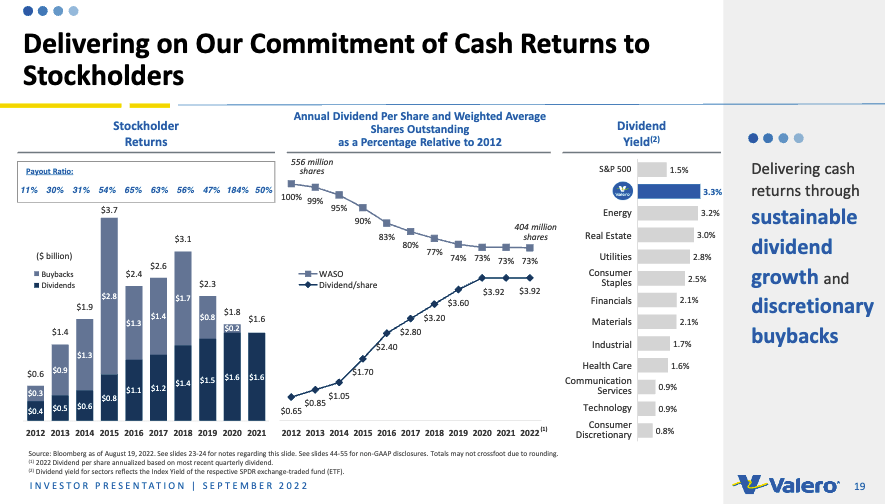

Consistent cash return to shareholders

VLO focuses on returning cash to shareholders through dividends and stock buybacks. Since 2012, outstanding shares have decreased by 27%, from 556 million to 404 million. Meanwhile, the annual dividend rose from 65 cents to $3.92.

Company presentation

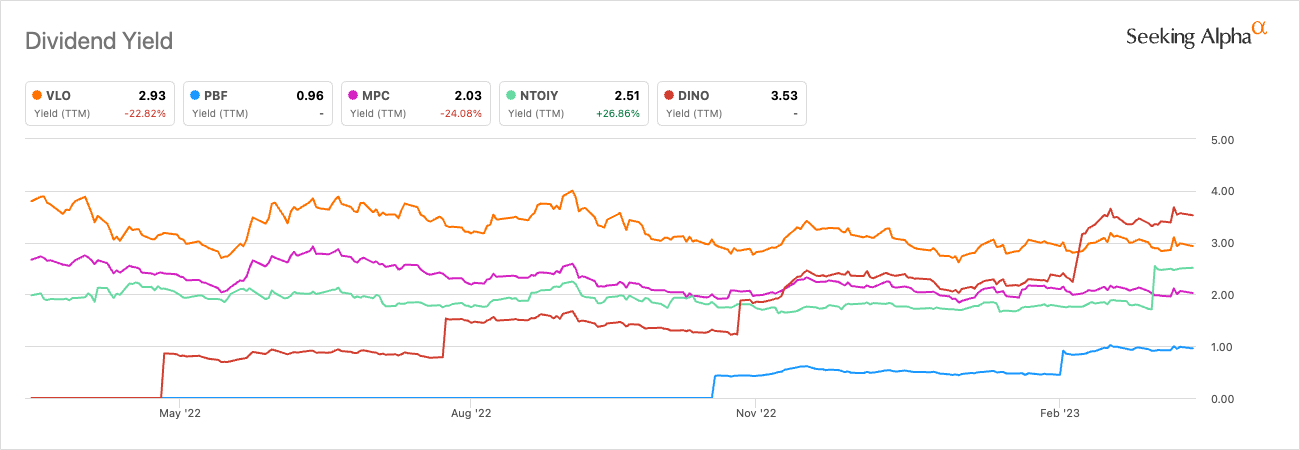

With a current dividend yield of 2.9%, VLO ranks among the highest compared to its competitors.

Seeking Alpha

Potential catalyst

VLO is seeking a Chevron-style exemption from sanctions that would allow it to purchase crude directly from Venezuela's state-run oil company PDVSA, hoping for a similar approval after a four-year ban. However, the US Treasury Department has not made any decision yet, indicating that the US government is not willing to ease Venezuela sanctions until President Nicolas Maduro makes political concessions to the opposition. Before the PDVSA oil sanctions were imposed in 2019, VLO received Venezuelan crude through long-term supply contracts that have not expired, making it one of the top three U.S. receivers of this oil. If VLO is allowed to process Venezuela's extra-heavy crude oil, which requires specialized refineries, it could reduce its main input costs and expand its profit margins.

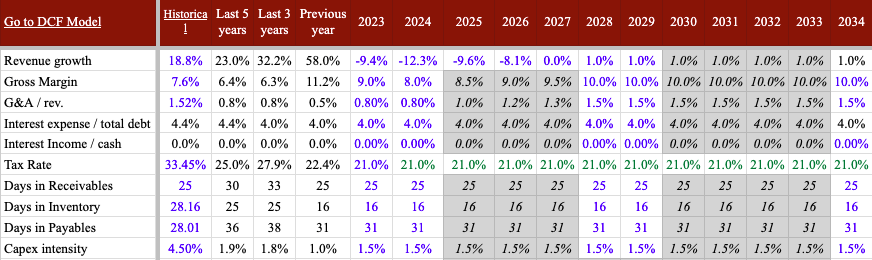

Valuation

I value the shares at $196 based on a discounted cash flow ("DCF") valuation. I use a cost of capital of 8.6%. While I expect revenues to decline in the medium term, I expect margins to improve as investments in improving yield and increased throughput of low-cost feedstock is completed. Below are my main assumptions:

Author estimates & company filings

Conclusion

Valero Energy Corporation has a competitive edge in the industry due to its high-quality refining assets, strategic location, and focus on renewable diesel and margin improvement projects. VLO is committed to returning cash to its shareholders through dividends and share buybacks. If Valero Energy Corporation is granted an exemption to import Venezuelan crude oil, it could unlock new opportunities and leverage its refining capabilities, further enhancing its competitive advantage in the market. I value Valero Energy Corporation shares at $189.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of VLO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.