Reaves Utility Income Trust: Not Built For The Current Investing Environment

Summary

- The outlook for the utility sector remains weak, these companies face tougher regulations as well as increasing consumer defaults.

- The Reaves Utility Income Trust's use of leverage isn't effective in a higher rate environment, this fund has been forced to use the principal to continue to pay monthly distributions.

- This Fund has consistently underperformed its peers and the broader indexes by a significant margin, there are better alternative income investments.

Daniel Balakov

Getting inflation adjusted returns and income isn't easy anymore. Since prices began to rise significantly in early 2021, the investing environment has changed significantly. Powell remains focused low lowering inflation to the Fed's stated goal of two percent, the Chairman has continued to raise rates even as the economic outlook has weakened. With rates continuing to rise and the increasing signs of business slow down, the investing environment has become more difficult to navigate.

One of the more popular areas of investment, particularly when rates were low, has been in utility companies. The Reaves Utility Income Trust Fund (NYSE:UTG) is a well-known exchange traded fund that invests almost exclusively in this sector. This fund has an expense ratio of 1.42%, $2.09 billion in assets under management, and a forward yield of 7.84%. The fund's holdings are 64.58% utilities, 19.12% communication, 8.83% real estate, 5.65% industrials, 1.82% energy. This closed ended fund defines a utility as any company that gets 50% or more of their revenues from that industry's business. This fund also reserves the right to use leverage up to 38% of the exchange traded fund's holdings. The current rate of use of leverage by this fund is 19.28%. This closed ended fund also only has 46 holdings, with most equity positions being around 4% of the overall fund's assets.

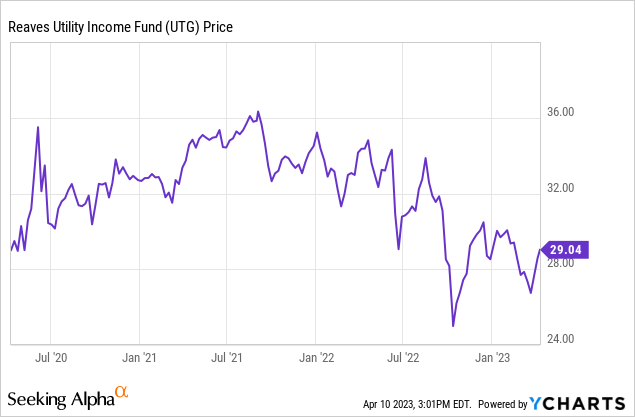

The Reaves Utility Income Trust Fund was hit hard over the last two years as increasing rates and rising costs hurt earnings and margins.

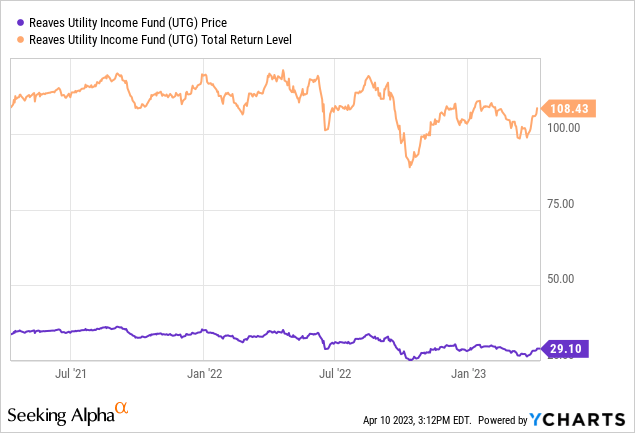

Even though the total return of this fund over the last three years was nearly 27%, the fund's total return over the last year was negative 8.3 percent.

Today, the Reaves Utility Income Trust Fund is a sell. The utility sector continues to see margin compression as costs rise and their significant debt levels continue to become more expensive to service. This CEF is also borrowing at a higher rate than the payouts being made monthly, the leverage this fund successfully used in a low-rate environment is no longer advantageous to consumers.

This fund was able to borrow cheaply and invest in companies with yields that were higher than the lending costs were, but the leverage this CEF uses has not worked in the current higher rate environment. This fund is now borrowing at a similar rate that the dividends being are being paid out at, and the CEF has been forced to sometimes pay out of the principle to maintain the high monthly distribution payments. The 5-year dividend growth of this fund is just 3.5%, and less than 25% of the monthly payouts are also from income or traditional dividends, the rest is from leverage, and the cost of borrowing has exceeded the monthly payouts this fund is making, this closed ended fund is making payments out of the principal. The actual dividend of this fund is below 2.5%. This is part of the reason the fund has underperformed the broader indexes as well as some of this company's peers, such as the Cohen and Steers Infrastructure Fund (UTF), and the John Hancock Tax-Advantaged Dividend Fund (HTD).

The utilities have been particularly heavily impacted by increasing prices and rising rates. This sector has been hit hard by rising expenses at a time when many utility companies are building out their networks. Consumer revenues have been falling as well. The warmer winter has resulted in less power usage per customer in many parts of the country as well, and the weakening economy as increased consumer default rates. Utility companies also tend to carry more debt than most companies, so rising rates have hit this leveraged fund in multiple ways.

The outlook for the Utility sector is remains negative as well. One in six Americans, or nearly 20 million people in the US, are behind on their utility bills, and the economic outlook continues to weaken as well. Many leading companies such as Disney (DIS) and Facebook (META) have already laid off large amounts of workers just in the past several months. The utility sector also faces stricter scrutiny form State Regulators as electricity prices continue to rise. With the presidential and congressional elections next year, politicians are likely to focus more on companies that are raising prices significantly on consumers as well.

Funds that have used leverage such as the Reaves Utility Fund were well positioned in a number of ways to take advantage of low rates for much of the last decade. These investments had unique appeal to investors because of the low-risk payouts they could offer in an investing environment where traditional assets, such as bonds, paid out minimal income. Today, the situation is reversed. Rising rates and increased costs have created added risks for leveraged investments at the same fixed income assets are paying out at more respectable levels. While the Reaves Utility Fund consistently offered solid total returns in a low-rate environment, this investment is not well-positioned in the current investing environment.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.