The fund recently merged with IVH on a NAV for NAV basis.

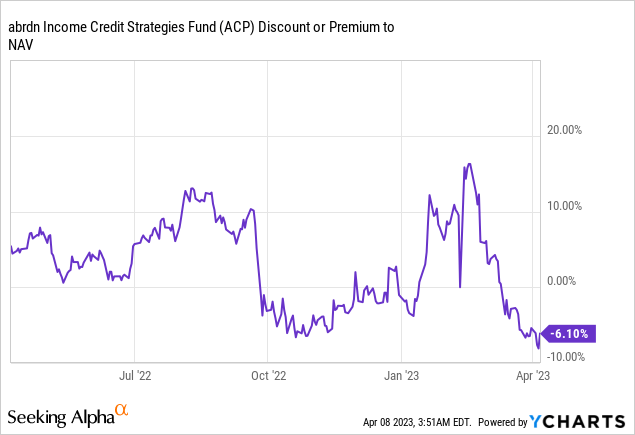

The market is now pricing the streamlining of the two platforms via a large -6% discount to NAV, down from a 10% premium earlier in the year.

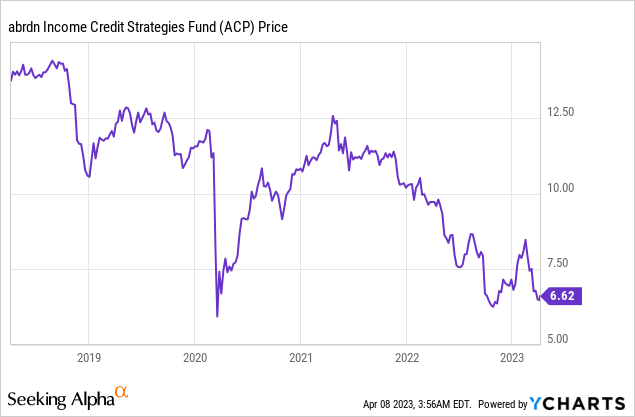

ACP is now approaching price levels close to its October 2022 lows.

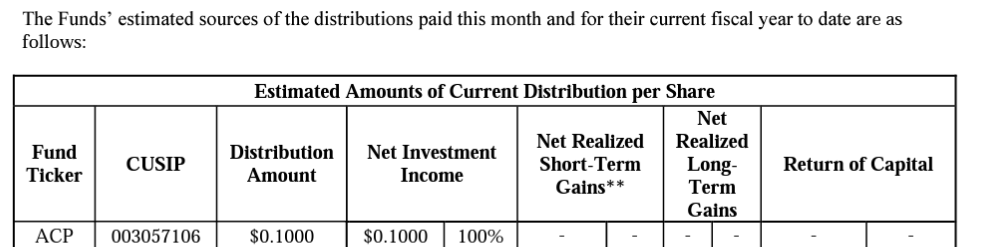

The fund's distribution is currently fully covered.

Torsten Asmus/iStock via Getty Images

Thesis

The abrdn Income Credit Strategies Fund (NYSE:ACP) is now larger. The fund finalized its merger with legacy IVH recently:

PHILADELPHIA--(BUSINESS WIRE)--Today, Delaware Ivy High Income Opportunities Fund (the “Fund”), a New York Stock Exchange-listed closed-end fund trading under the symbol “IVH,” announced that the acquisition of substantially all of the assets of the Fund by abrdn Income Credit Strategies Fund (the “Acquiring Fund”), a New York Stock Exchange-listed closed-end fund trading under the symbol “ACP,” was completed on March 10, 2023 at approximately 5:00 pm ET (the “Reorganization”). Fund shareholders approved an Agreement and Plan of Acquisition that provided for the Reorganization at a Special Meeting of Shareholders held on November 9, 2022.

Relevant details as of the closing of the Reorganization are as follows:

Merger (Fund)

As we speak managers are fighting for their roles in the new combined entity, and new plans are drawn out to merger the funding and assets of the combined entity under the abrdn platform. We think the combined entity will very much resemble the old ACP, but the market has now embedded this volatility:

We can now see a significant collapse of ACP's premium to NAV, that just a month ago was over 10%. It now stands at -6%! The market is basically nervous around the streamlining process and a unilateral modus operandi going forward, thus discounting the shares versus the NAV of the fund.

Back to the Lows

From a price perspective we are back to closing in on the October lows for the fund:

We can notice how volatile this CEF has been, rallying tremendously after its October low, only to re-trace that move now, even though spreads in the HY space have not blown out.

This CEF is a very volatile one, and we have said that before. In a recessionary environment like today's it pays off to trade around this position. As we have said before, we feel the merger with IVH is positive long term for ACP, thus there will be a massive rally here once the recession is over.

Is the distribution safe?

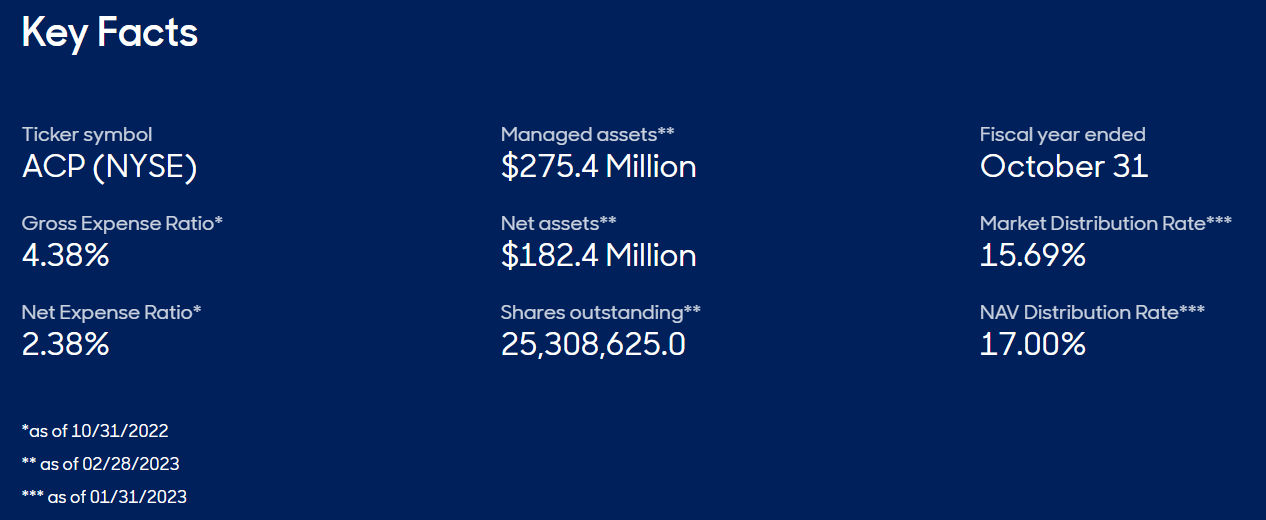

The fund's yield is currently over 15%:

Yield (Fund)

That is a pretty massive figure, but it is fully covered as of the latest Section 19a report:

Section 19a (Fund)

"If it is not broken, don't fix it" they say. We feel that as long as the fund will be able to cover its distribution there is no need to cut it. However, as we have seen from the recent market action, it is not all about the distribution. Once you get to yields above 12%, the exact figure matters less than what is perceived as a strong forward for the fund.

The CEF is now trading at a discount (basically a move of -15% in premium over the past month), not because of an unsupported yield, but because the market wants to see how the merger plays out.

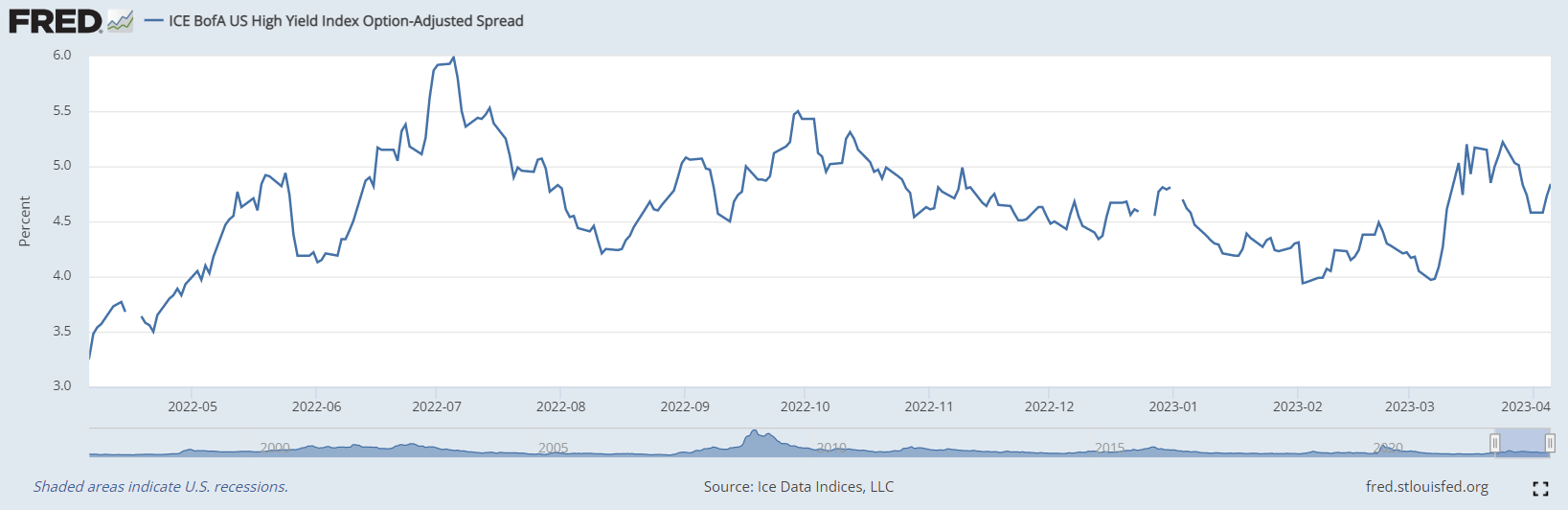

Where are we headed in the HY space?

HY Spreads are not back at their widest levels:

HY Spreads (The Fed)

While they have moved higher in the past month, they are not near their October wides. We might see them blow out if there is another significant risk-off event in the market.

One thing is for sure though - 2023 is going to be a great year for buying leveraged high yield. One has to stomach volatility though, and also watch out for other fundamental sign-posts.

ACP was not a buy when the premium was above 10%, and we told investors to trim exposure there. The CEF is now becoming interesting again, and taking small bites here and seeing how the price performs is not a bad idea, especially when from a price stand-point we are close to the lows again.

Conclusion

ACP is a closed end fund focused on the riskiest HY paper. The vehicle recently merged with IVH and is going through a platform streamlining process. We told investors to trim exposure when the fund was trading with a premium over 10% above NAV, and now the vehicle is trading at a -6% discount. This CEF is extremely volatile, especially in times of portfolio and market changes. With its price now approaching its October lows again, ACP is starting to look interesting again.

With a financial services cash and derivatives trading background, Binary Tree Analytics aims to provide transparency and analytics in respect to capital markets instruments and trades.We are reachable at BinaryTreeAnalytics@gmail.com_____________________________http://www.BinaryTreeAnalytics.com

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.