Vector Group Ltd.: Economic Adversity Persist, Diversify Into Consumer Staples With VGR

Summary

- The Consumer Staples Select Sector SPDR Fund was one of the best-performing sectors last year, falling by less than 1% compared to the 19% decline of the Russell 1000.

- With economic uncertainty lingering until 2023, diversifying into consumer staples is crucial for risk management.

- In times of uncertainty, investments in consumer staples tend to fare better. In light of this information, I think VGR is a smart investment due to its solid fundamentals.

Snezhana Kudryavtseva

Investment Thesis

Vector Group Ltd. (NYSE:VGR) is a consumer staple stock. As the Federal Reserve continued to raise the federal funds rate throughout 2022 to curb inflation, investors fled to safer, higher-yielding investments like bonds and cash equivalents. The Consumer Staples Select Sector SPDR Fund [XLP] was one of the best-performing sectors last year, falling by less than 1% compared to the 19% decline of the Russell 1000.

With economic uncertainty lingering until 2023, diversifying into consumer staples is crucial for risk management. In times of uncertainty, investments in consumer staples tend to fare better. In light of this information, I think VGR stock is a smart investment due to its solid fundamentals. The most exciting things about this company are its rising EPS and stable dividend despite being volatile. In addition, the company's ownership structure and business model make it more resilient to economic downturns. In light of these factors, I have a bullish outlook on this stock and recommend it to investors looking to add to their consumer staples holdings as part of a diversified portfolio.

Company Overview

Vector Group is the fourth-largest cigarette producer in the U.S. Its brands, such as Grand Prix, Liggett Select, and Pyramid, are aimed at the discount market. The company is also involved in real estate through its subsidiary, New Valley. However, the company's management considerably lowered its real estate risk by spinning off its New York real estate brokerage, Douglas Elliman, in late 2021.

The Business Model: A Hedge Against Economic Downturns

VGR's cost-focused business model is highly efficient. The company's strategy is to target the budget-conscious bargaining sector. In a downturn, VGR's business model makes it more likely that its products will sell than its competitors, which charge higher prices.

Even though Vector Group's management expects that the industry will see a long-term drop in cigarette sales because of health concerns, government limits, and the fact that smoking is becoming less popular, Vector Group can benefit from strong pricing power. Due to the habit-forming nature of tobacco products, manufacturers can raise prices without seeing a corresponding drop in demand, resulting in increased profit margins and revenue even when unit sales fall.

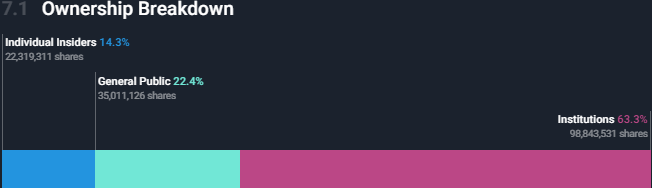

High Institution Ownership

We can identify who controls Vector Group Ltd. by looking at its shareholders. Institutions own the majority of the company's stock (63.3%). If the stock price goes up, the collective gains the most. (or lose the most if there is a downturn).

Wallstreet

High institution ownership matters. Many organizations use an index representing the regional market to evaluate their success. As a result, companies that are part of large indices tend to get more of their focus.

It is clear that Vector Group has institutional investors and that these investors own a sizable chunk of the company. Having some credibility amongst institutional investors is a good sign. Institutions, like people, sometimes make poor investment decisions, so we can't rely on that alone. There is always the possibility of a crowded transaction when numerous institutions hold the same stock. In a botched trade, several parties may rush to unload their shares.

Shareholders need to know that the company is owned by institutions that jointly hold more than 50% of the stock. It seems that hedge funds own 5.1% of Vector Group shares. That interests me because hedge funds are known to try to sway management and usher in policy shifts that will boost short-term returns for investors. In light of these statistics, optimism abounds for investors because of the many advantages associated with high institution ownership, including excellent liquidity and sound policies that maximize investors' returns in the short and long term.

Growing EPS

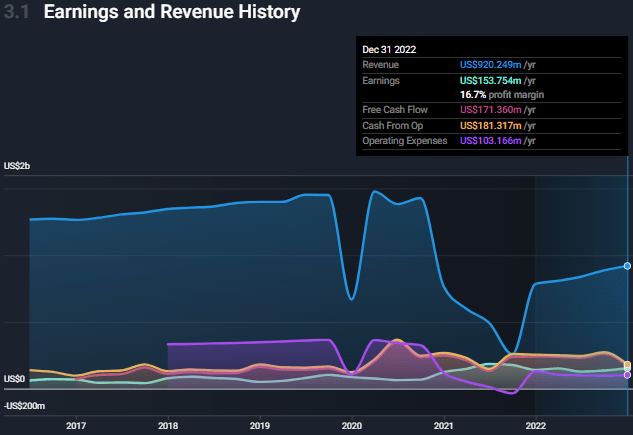

If a company can sustainably increase its EPS, the market should reward it with a higher share price. That's why most savvy long-term investors view earnings per share increase as a net positive. Over the past three years, Vector Group's earnings per share [EPS] has increased by a compound annual rate of 19%. Investors have a lot to cheer about if this growth rate persists into the foreseeable future.

Analysis of revenue expansion and earnings before interest and taxes [EBIT] margins can provide insight into whether current profit growth will likely be sustained. Vector Group did well to increase revenue during the past year, albeit at the expense of EBIT margins. If EBIT margins can be maintained, more expansion is possible.

Wall Street

Dividend

VGR declared a fresh dividend of $0.20 per share. With this dividend payment, the dividend yield will be 6.4%, which is about paring for this sector. Earnings Coverage of Vector Group's Payment Is Strong.

I prefer dividends to be stable over time; therefore, I always look into whether or not they can be maintained. While the most recent payment represented 79% of earnings, cash flows were significantly higher. The cash payout ratio is more important than the dividend payout ratio because the dividend is essentially cash being distributed to shareholders.

If the previous year's tendency continues, profits per share could increase by 12.9% in the coming year. Assuming the dividend keeps rising as it has done, the payout ratio is expected to be around 66%, well inside a safe zone.

Risks

Although I have an optimistic outlook on this stock, it is not without its risks. Tobacco businesses may soon be subject to new regulations proposed by the Biden administration that aim to reduce nicotine levels in cigarettes to non-addictive levels. Investors should view regulation as a long-term problem for the industry, even though such a dramatic policy reform may take years. Also, long-term declines in cigarette sales are possible due to health concerns and the declining appeal of cigarettes. These risks may affect my bull thesis; therefore, I advise potential investors to be wary of such risks.

Conclusion

I think VGR is a fantastic investment opportunity because of its solid fundamentals, and I agree that diversifying into consumer staples is an excellent way to protect against economic downturns. However, investors should exercise caution since this opportunity is not without risks.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: The content of this article is intended solely for educational purposes. The information presented here is not intended as a recommendation to buy or sell any securities. Do your own due diligence and form your own opinion before making any stock trades, or talk to a financial expert. Capital loss is a possibility when investing.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.