Delta Air Lines Stock: A Buy After Sell Off

Summary

- Delta Air Lines stock sold off after soft Q1 guidance and risk aversion in the stock market.

- There are risks to Delta's business, as there are risks for any airline, but I believe that Delta has a strong execution path ahead.

- Current share prices offer a compelling entry point.

- Looking for a helping hand in the market? Members of The Aerospace Forum get exclusive ideas and guidance to navigate any climate. Learn More »

Lukas Wunderlich

Delta Air Lines (NYSE:DAL) will be kicking off the Q1 earnings season for airlines on the 13th of April. While airlines are seeing capacity recovery toward pre-pandemic levels a complex demand and supply environment is putting a damper on share price performance. In this report, I will discuss the share price performance as well as the guidance, opportunities and risks for Delta Air Lines.

Is Delta Air Lines Stock A Buy?

Seeking Alpha

I have a buy rating on Delta Air Lines stock, but the reality is that since the last time I covered Delta, the stock has lost 11.8%. There are a couple of reasons for that. Specific to Delta Air Lines the guidance came in a bit on the light end due to higher maintenance costs as the airline prepares to further restore its network. More global factors are the problems at banks which do not directly impact Delta Air Lines, but put doubts on continued robust demand for air travel and made some investors more reserved. Airline stocks are not steady performers and so when the market sold off, travel related stocks took a bigger hit. Besides that central banks are continuing to increase interest rates, which is not necessarily a positive for airlines.

Delta Air Lines Q1 2023 Guidance Disappointed

For the quarter, Delta Air Lines expects $11.8 billion to $12.1 billion in adjusted revenues which is up 15% from the midpoint compared to the comparable pre-pandemic period while total revenues are guided in the $12.9 billion to $13.2 billion range, up 24%. Analysts are expecting $12.25 billion in revenues with a low estimate of $11.9 billion on the low end and $12.8 billion on the high end. The consensus is significantly lower than the adjusted revenue guidance provided.

Perhaps more important is the guidance for earnings per share, which is in the $0.15-$0.40 range whereas analysts were hoping to see $0.64 per share. Since providing guidance, the estimate has come down to $0.33 per share, slashing the estimate in half. On GAAP, Delta has projected a loss of $0.35 to $0.10 per share impacted mostly by one-time pilot agreement charges shaving off 6 percentage points off the operating margin. So, overall what we see is that analysts had previously expected a significantly stronger quarter. I wouldn’t necessarily characterize Q1 2023 as weak because it does include the one-time pilot agreement charges as well as the maintenance costs. Both of these items should help Delta restore its operations.

The earnings whisper numbers for Delta are $12.05 billion in revenues and $0.37 in earnings per share.

China As A Risk To Rebuilding Capacity

Delta Air Lines

China has been a good market for Delta, but at the JPMorgan 2023 Industrials Conference, Delta shared that it was restricted to just a few airports to restart operations and Sino-American relations plays a role in that. So, that's certainly a risk to Delta. I don’t expect it to a major risk to Delta in 2023, but it's something to keep in mind.

A Complex Supply And Demand Environment

From multiple perspectives the supply and demand mechanisms remain challenging. Pilot shortages are less of a problem for Delta Air Lines, but the entire training procedure of new hired pilots does put pressure on how much Delta can realistically restore its network as it requires experienced pilots to instruct and train new pilots. There also remain challenges at the OEMs, which pushes deliveries to the right. How much this impacts Delta specifically is not clear, but it's something that keeps the industry as a whole constrained. Although this is not necessarily a bad thing given the shortage of pilots and the need to efficiently restore the network without throwing in capacity left and right just because the planes and/or pilots are there.

On oil, I do believe that Delta has somewhat of an advantage as it runs its own refinery and it continuously invests in new technology aircraft and it also carefully considers absorbing older aircraft at the right price point. Recently, OPEC+ announced that it would be cutting production by 1.6 million barrels a day which sent oil prices higher. So, the fuel price environment remains a watch item.

When it comes to air travel demand, airlines are seeing that travelers are booking closer to their travel date instead of months in advance. With inflation and higher interest rates, it's not quite known what air travel demand will look like. Airlines generally only have a strong sense of demand for 90 to 100 days, but even despite the uncertainties ahead a strong year is still expected with Delta aiming to realize $5 to $6 in earnings per share for 2023.

The Opportunities For Delta Air Lines

One thing that I like about Delta Air Lines is their approach to the business. When it comes to airplanes they don’t necessarily take the most fuel efficient airplane but they let each plane go through a full cost cycle analysis and base their purchasing plan on that. Beyond that they also place orders in such a way that their maintenance division can expand. The order with Boeing (BA) announced in July last year is an example of how Delta likely got a good price on the airplane order and also secured additional MRO capabilities.

I view corporate travel also as an opportunity for Delta Air Lines. During the pandemic Delta was one of the first or maybe even the first airline claiming corporate travel would never come back. We now see that corporate travel on the domestic network has returned to 80% of pre-pandemic travel and that gives some confidence in a full recovery as well as an international recovery. The international recovery for the full business is also an opportunity for the airline. China is of course a risk, but it also provides an opportunity.

Conclusion: Delta Air Lines Stock Remains A Buy

I think that Delta Air Lines remains a buy. Q1 will be a bit light, but 2023 remains strong with clear opportunities as well as risks for the business which gives the airline the awareness on where it can shield itself and where it can benefit from demand strength. Delta Air Lines aims to get to more than $4 billion in free cash flow, and given how management approaches things I don’t think that's a moonshot despite several uncertainties faced.

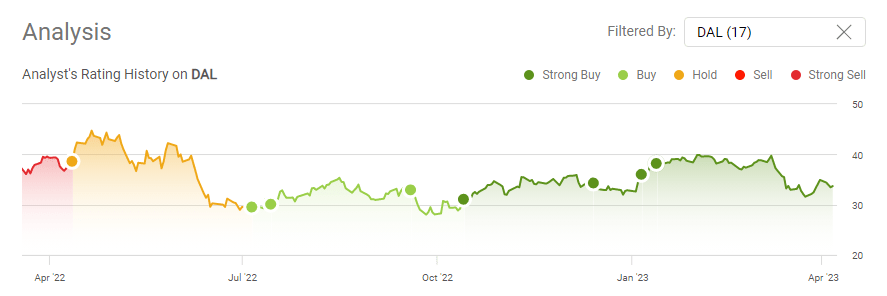

Delta stock is currently trading in the range where it traded for much of H2 2022 and even lower than H1 2022 and 2021. Given that the company is restoring its operations and there currently is a demand environment where costs can be passed through coupled with a strong management execution I don’t think that the current price is reflective of the 2023 performance and beyond and Wall Street analysts seem to agree with a $51.42 price target giving Delta Air Lines stock 52.6% upside.

If you want full access to all our reports, data and investing ideas, join The Aerospace Forum for the #1 aerospace, defense and airline investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.

This article was written by

His reports have been cited by CNBC, the Puget Sound Business Journal, the Wichita Business Journal and National Public Radio. His expertise is also leveraged in Luchtvaartnieuws Magazine, the biggest aviation magazine in the Benelux.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.