The PIMCO Active Bond ETF uses fundamental analysis with a bottom-up security-picking approach to create its portfolio.

While it benchmarks against the Bloomberg U.S. Aggregate Index, unlike most bond ETFs, it is not limited by the index in creating its portfolio.

This article will review the ETF's holdings and performance. I included some expert views on the bond market as that could influence when to buy into this ETF.

Recent history shows that active management hasn't outpaced its index-based competitors but in 10 years, it was the clear winner. Maybe that mojo will return.

As a Core Fixed Income ETF for the US market, I would give the BOND ETF a Buy rating based on its since-inception record.

Looking for more investing ideas like this one? Get them exclusively at Hoya Capital Income Builder. Learn More »

I came across the PIMCO Active Bond ETF (NYSE:BOND) while working on my AGG Vs. BND: Picking A Core ETF For US Bond Exposure article. Being actively-managed versus index based like iShares Core U.S. Aggregate Bond ETF (AGG) or the Vanguard Total Bond Market ETF (BND) and most other broad bond ETFs, I decided to take a deep dive into the BOND ETF. I was also intrigued by its superior 10-year CAGR, though recent results only match its competitors.

US Bond market overview

First overview is from Morgan Stanley, published before the banking crisis broke.

If the Fed's plan to durably stem inflation works, asset valuations may benefit over the longer term, offering several considerations for investors' fixed-income portfolios.

Asset-backed securities: Particularly in agency mortgage-backed securities (MBS) and some securitized credit products, yield spreads (the difference in the rate of return between these assets and U.S. Treasuries) have stayed wide compared to high-yield and investment-grade issues. Investors may still want a little extra yield compared to Treasuries, which would make MBS and securitized credit products attractive and draw asset flows.

High-yield credit: Without a major recession on the horizon and with high-yield indexes yielding around 8-9%, there is ample room for yield spreads (the difference in the rate of return between high-yield bonds and Treasury bonds) to widen and still generate mid-single digit returns, if not higher. Moreover, it would also be highly unusual to have two years of negative high-yield returns in a row, after a -11% return in 2022.

In fixed income investing, it doesn't necessarily pay to keep pressing by adding risk. Sometimes it's best to wait and, like Les Bleus, strike when the break is available.

While we expect more volatility this year, we see greater opportunity ahead for active management to shine. Active sector and security selection decisions should carry more weight in a market not overwhelmed by macroeconomic forces or dominated by central banks like in the wake of the 2008 global financial crisis (GFC). Bond investors will be paid to bear risks.

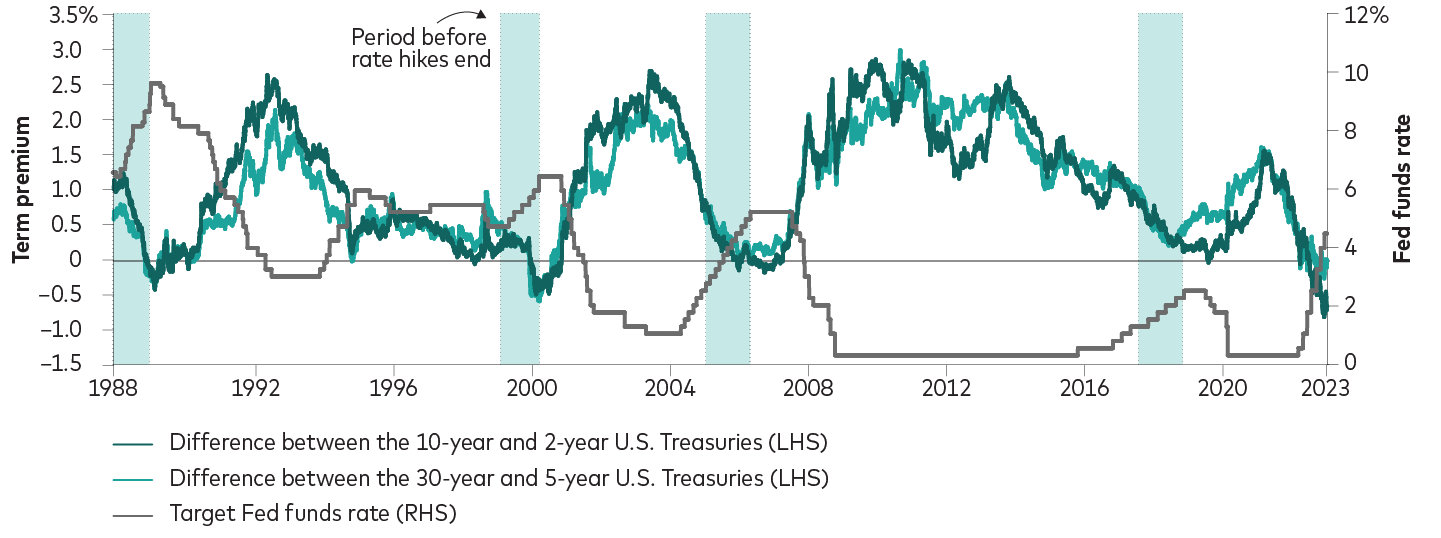

Historically, we note that the yield curve starts to steepen several months before the last Fed rate hike of the cycle, which we believe will be in the first half of the year. The outcome is likely a steeper Treasury curve offering more term premium. As we approach the end of the hiking cycle, we are positioned to benefit from the changing shape.

The yield curve tends to start steepening as rate hikes end

The investment seeks current income and long-term capital appreciation, consistent with prudent investment management. BOND has a diversified portfolio of Fixed Income Instruments of varying maturities, which may be represented by forwards or derivatives such as options, futures contracts, or swap agreement. It invests primarily in investment grade debt securities, but may invest up to 30% of its total assets in high yield securities.

BOND has $3.3b in AUM and provides investors a healthy 6.3% TTM Yield. Fees, at 56bps, are high compared to its non-actively bond ETF competitors. PIMCO says they emphasize higher-quality, intermediate-term bonds, selecting risk exposures that should produce strong returns in different markets.

Even actively managed ETFs have a benchmark they measure themselves against. Here it is the Bloomberg U.S. Aggregate Index, which has this description:

The Bloomberg US Aggregate Bond Index (ticker: LBUSTRUU), formerly known as the Lehman Aggregate Bond Index and the Barclays US Aggregate Index, was created in 1986 with backdated history going back to 1976. The index has been maintained by Bloomberg L.P. since August 24th 2016. The index is a predominant index benchmark for US bond investors, and is a benchmark index for many US index funds.

Overview

The Index is a composite of four major sub-indices: US Government Index; US Credit Index; US Mortgage Backed Securities Index (1986); and (beginning in 1992) US Asset Backed Securities Index. The index holds investment quality bonds. The ratings are based on S&P, Moody, and Fitch bond ratings. The index does not include high yield bonds, municipal bonds, inflation-indexed bonds, or foreign currency bonds.

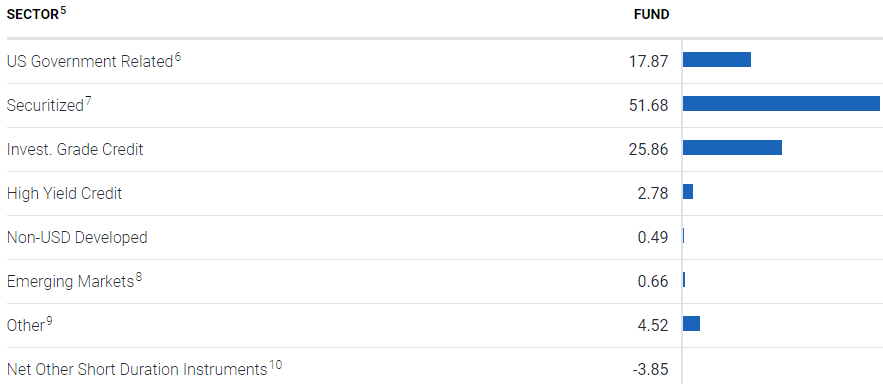

With the Securitized bucket including Agency MBS, non-Agency MBS, CMBS, ABS, CDO, CLO, and Pooled Funds, US government exposure is higher than the percent shown. The sector allocations translate into the follow credit allocations: 90% investment-grade. BOND is allowed to own up to 30% in BB or lower rated bonds.

pimco.com ratings

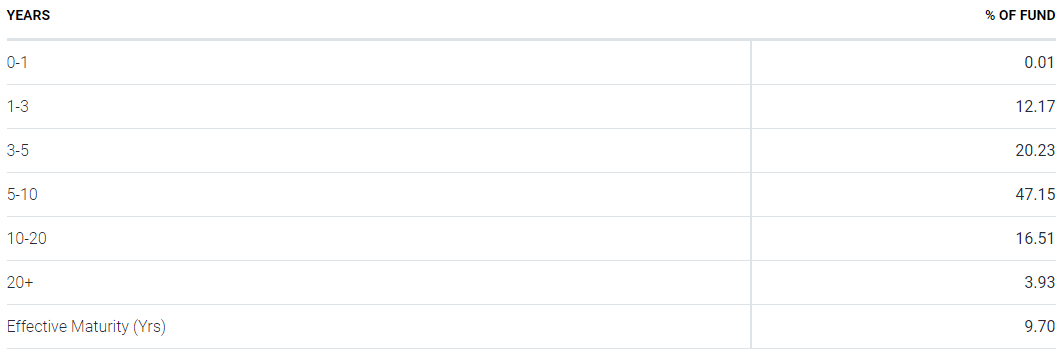

Besides the credit ratings, another allocation effecting risks to the investor is the maturity allocation.

pimco.com maturities

While the WAM is 9.7 years, the portfolio effective duration is only 6 years; that still translated into a potential 6% loss if rates climb 100bps. As the ETF is allowed to own USD-denominated bonds, there is a small percent issued from outside the US.

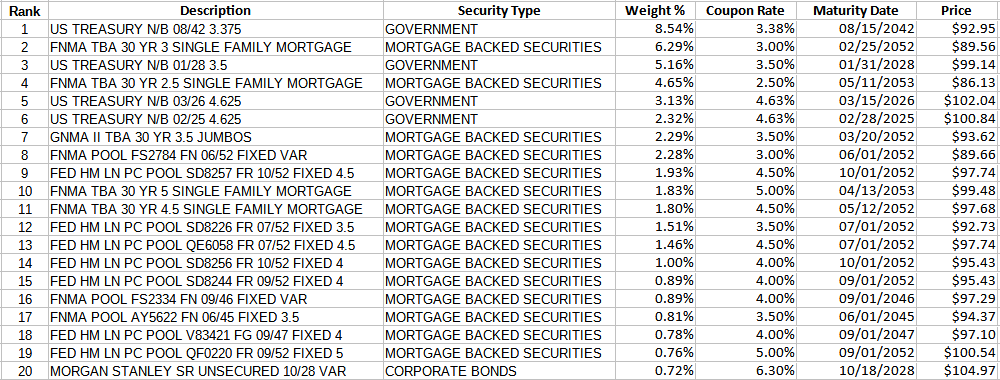

Top holdings

pimco.com; compiled by Author

Even with almost 1100 positions, the Top 20 account for 49% of the portfolio. That is somewhat misleading as there is a -17% allocation to something label Net Other Assets, which I found no explanation for. Other statements imply some of that is assets shorted to control the portfolio's duration.

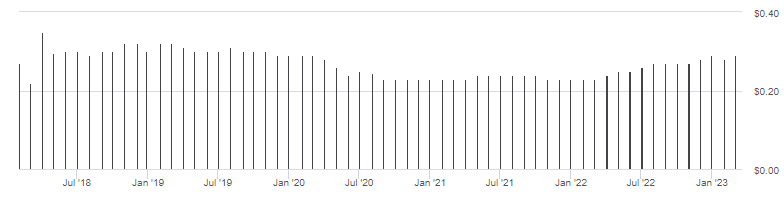

Distribution review

seekingalpha.com BOND DVDs

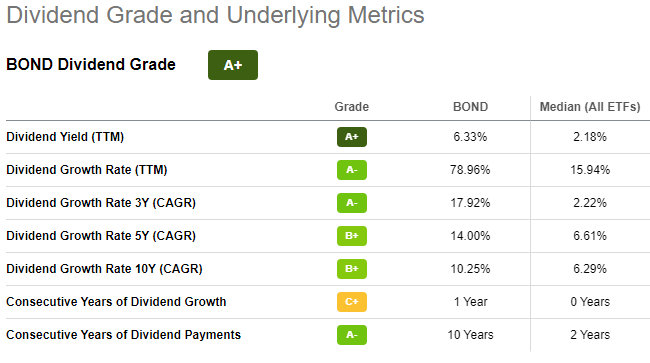

As expected, payouts have been climbing slowly as old bonds mature and new bonds are added with higher coupons. Seeking Alpha give BOND a "A+" rating for dividends.

seekingalpha.com BOND scorecard

Performance review

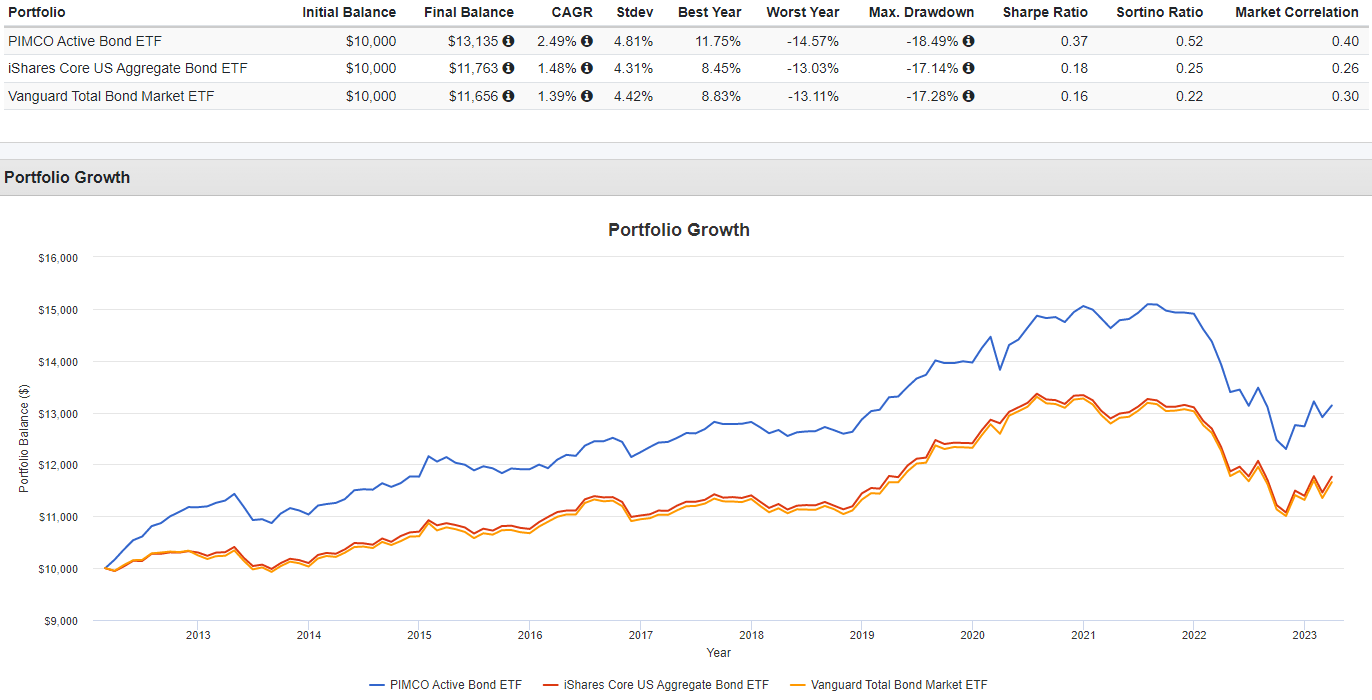

Since I mentioned both the AGG and BND ETFs earlier, I included them here to compare how this actively-managed ETF fared against two passively-managed ETFs.

PortfolioVisualizer.com

Since starting in 2012, the active strategy followed by BOND is clearly providing investors with a superior CAGR at little cost in higher StdDev, Worst Year, or Max Drawdown results. That edge has been less obvious in recent years.

Portfolio strategy

I like the concept of the Buy/Hold usage of Core funds as the bedrock an investor uses to build the rest of their portfolio on top of. This is especially true for seven-figure portfolios or for novice investors as they gain in their ability to allocate to more focused funds. BOND's advantage over its competitors is its active strategy. While it can go wrong, there is the possibility of it outperforming the funds that invest using broad indices.

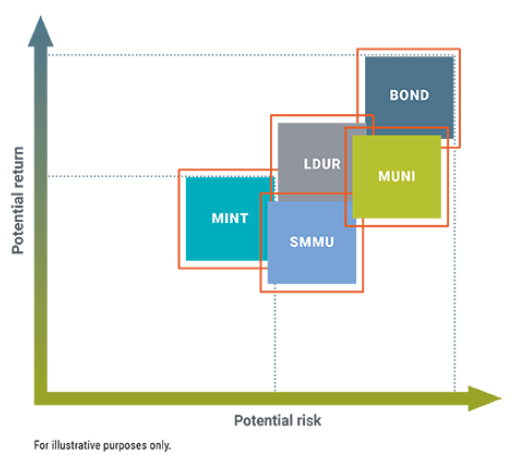

Being a major player in the fixed income sector, they included the following chart showing where BOND falls on the risk/return spectrum (though note the disclaimer).

pimco.com

Final thoughts

When picking a bond fund, after having decided what allocation you want, here are some questions to ask in selecting that fund.

When will you need to sell to raise cash? Selection of a fund with a duration shorter than that is a good strategy.

Do you want to avoid currency risk? If yes, you need a fund like BOND or one that hedges their currency risk if it holds non-USD bonds.

Are you willing to accept a lower yield to avoid owning non-investment-grade bonds? If just maybe, combining BOND with a HY ETF would be a possible strategy.

As a Core Fixed Income ETF for the US market, I would give the BOND ETF a Buy rating based on its since-inception record.

I ‘m proud to have asked to be one of the original Seeking Alpha Contributors to the 11/21 launch of the Hoya Capital Income Builder Market Place.

This is how HCIB sees its place in the investment universe:

Whether your focus is high yield or dividend growth, we’ve got you covered with high-quality, actionable investment research and an all-encompassing suite of tools and models to help build portfolios that fit your unique investment objectives. Subscribers receive complete access to our investment research - including reports that are never published elsewhere - across our areas of expertise including Equity REITs, Mortgage REITs, Homebuilders, ETFs, Closed-End-Funds, and Preferreds.

Build sustainable portfolio income with premium dividend yields up to 10%.

I have both a BS and MBA in Finance. I have been individual investor since the early 1980s and have a seven-figure portfolio. I was a data analyst for a pension manager for thirty years until I retired July of 2019. My initial articles related to my experience in prepping for and being in retirement. Now I will comment on our holdings in our various accounts. Most holdings are in CEFs, ETFs, some BDCs and a few REITs. I write Put options for income generation. Contributing author for Hoya Capital Income Builder.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.