China Eastern Airlines: A Risky Buy On Reopening Surge

Summary

- China only re-opened in late 2022, so significant improvements in financial results for airlines remain absent.

- Rate of capacity recovery will be a watch item this year.

- China Eastern Airlines Corporation Limited stock could provide an opportunity to capitalize on the Chinese recovery, but risks are clear and need to be understood.

- Looking for a helping hand in the market? Members of The Aerospace Forum get exclusive ideas and guidance to navigate any climate. Learn More »

viper-zero/iStock Editorial via Getty Images

With China opening up for business again, Chinese airlines could be an interesting opportunity to explore. However, don't expect that with a reopening in Q4 2022 that their most recent results are pretty. One should also carefully keep in mind any risk related to China. In this report, I will analyze the 2022 results for China Eastern Airlines Corporation Limited (OTCPK:CEAYY, OTCPK:CHEAF) and briefly look at the capacity recovery in the first two months of 2023.

The Risks Surrounding China

I wouldn't say that Chinese stocks do not offer any opportunity, but I do believe that there are significant elements that put a damper on foreign investments to capitalize on the re-opening of the Chinese economy. A concentration of power for President Xi Jinping is one of those, and another is the constant fear of an escalation with Taiwan.

Moreover, with conflicts mounting and the Sino-American relation at a low, we see that China and the West are ending on opposing sides more and more, which obviously does not remedy any risks and concern that already exists.

Ticker Risk: Low Volume

The Sino-American tension also has its impact on the ticker risk. Chinese stocks were at a risk of being delisted. As part of this tension, the U.S. went after Chinese companies seeking more power to audit Chinese companies with a listing on U.S. stock exchanges. In December, China agreed to this, but that wasn't the end of it. Following the agreement, China Eastern Airlines decided it would delist from the NYSE. With that, any audit or filing requirements associated with an NYSE listing would also lapse.

China Eastern Airlines' stock now trades over the counter/OTC as a pink sheet, which is the least regulated OTC tier. So, that also means that useful disclosures might not be provided, as they might not be required.

Beyond that, there is a volume risk as an OTC stock. Due to the low volume, there might be a lack of liquidity, which makes quick buying and selling and constant prices more challenging. The lack of volume makes buying and selling more difficult and might also increase volatility. Investors should be aware of these additional risks when making investment decisions.

China Eastern Airlines' Results Worsened In 2022

China Eastern Airlines

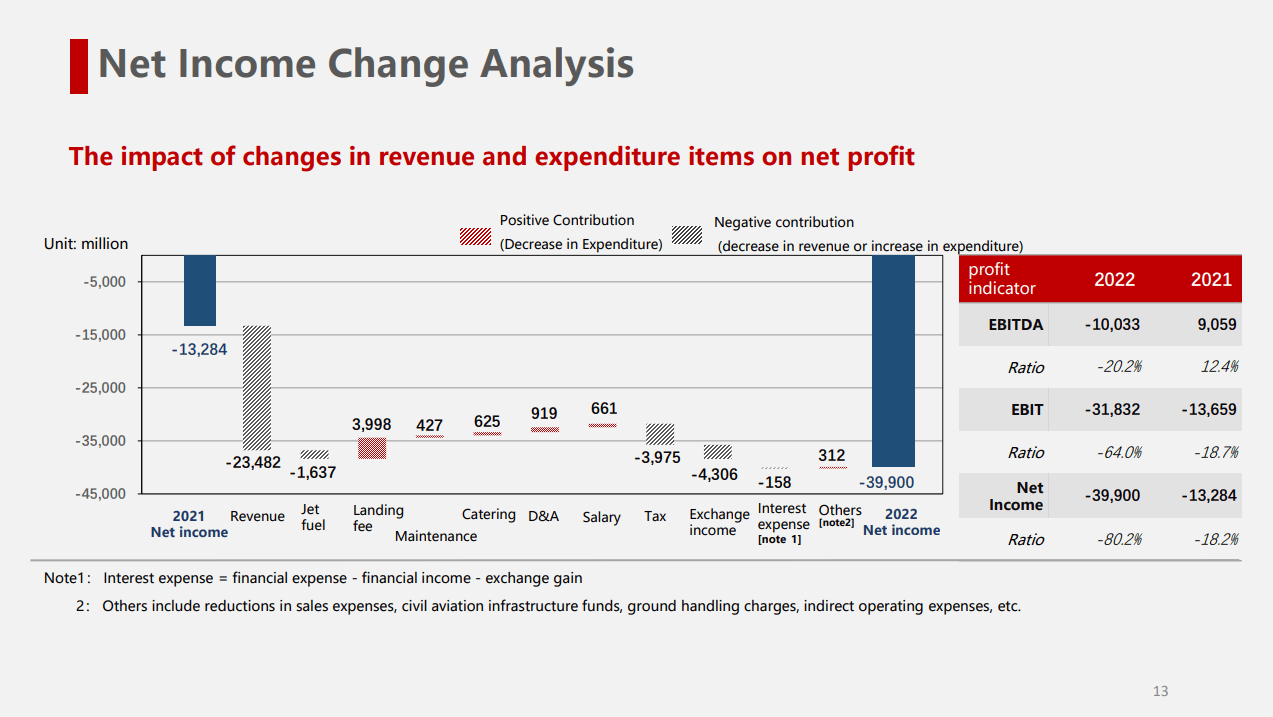

Not completely unexpected, the results for China Eastern Airlines heavily contrast with the results seen among most carriers outside of China. The rapid opening and closing of major parts of China are to blame for that. The strict lockdowns might curb the spread of COVID-19, but once society reopens the spreading continues, and we saw that happening in China, and it has had an impact on airlines. Year-over-year, revenues declined by 32.4% providing the biggest setback to profits. Costs also declined, but on a 40% lower capacity year-over-year the cost balance only declined by 6% driven by higher fuel costs and cost reductions in amortization, salaries and marketing not declining in line with the lower capacity production.

China Eastern Airlines

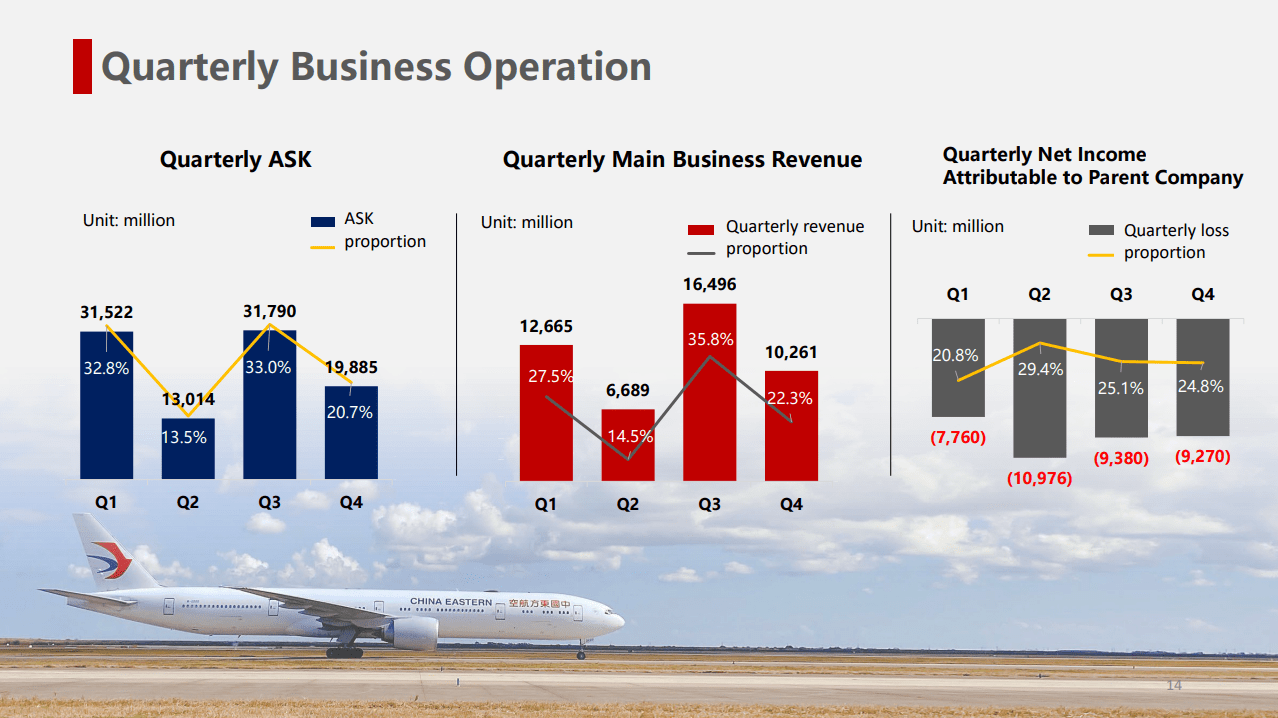

If we look at the ASK production, we see that the re-opening of China did not have a major impact, or at least not when we view it within the year. We did see net losses stabilize despite lower revenues and revenue proportion exceeding the capacity proportion, but we cannot speak of mountains of profits and cash being generated. That could also not be possible because restrictions were eased by the end of November 2022, and realistically a December month would not turn the quarter into a winner.

A Gradual Path of Recovery

Boeing

While the operations are expected to improve strongly, the path toward full recovery to pre-pandemic levels remains long. International travel revival will help, but the path is still long. Cargo is expected to be soft as inflation and interest rates put pressure on disposable income. Passenger capacity in the first two months this year is up 21.6% with a 267% increase in international capacity and the unit revenues are up 43% and even over 400% for international traffic. Compared to pre-pandemic levels, the capacity is only 70% recovered. We do expect significant year-over-year changes to close the capacity gap with pre-pandemic levels, but it will take a while before we will see the full recovery in capacity and financial results.

The positive is that in January capacity was recovered 66% compared to pre-pandemic levels and by February the recovery was 70% year-to-date. So, there is an acceleration, but even with a rate of 4% per month, it will take towards the end of the year to be fully recovered. We don't know whether the rate of recovery will accelerate or whether it will stabilize, but what we do know is that 2022 will be a lot about capacity recovery which will significantly boost the year-over-year financial results, but I'd expect that in 2024-2025 we should have better chances at seeing pre-pandemic profits.

Who Owns China Eastern Airlines?

China Eastern Airlines is 61.6% owned by the Chinese government, making them the majority owner while the remainder is held publicly via A and H class shares.

Conclusion: China Eastern Airlines Stock Offers A Way To Capitalize On Reopening

I believe that China Eastern Airlines stock offers an opportunity to capitalize on the re-opening of China, but one should be aware of two things. The first one is that from an operational perspective there is a ramp-up in capacity towards pre-pandemic levels this year, and we don't know for sure whether that ramp will accelerate or not but what we do know is that full annualized effects will only be visible in 2024 or perhaps 2025. So, patience is needed here. Secondly, we should keep in mind that the stock trades OTC with its associated risks

While I am not generally negative on China, I cannot deny that with the alliance formed around the world, China and the West are not aligned well at the moment. This does not really provide the desired stability for putting your dollars into Chinese companies like China Eastern Airlines Corporation Limited.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you want full access to all our reports, data and investing ideas, join The Aerospace Forum for the #1 aerospace, defense and airline investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.

This article was written by

His reports have been cited by CNBC, the Puget Sound Business Journal, the Wichita Business Journal and National Public Radio. His expertise is also leveraged in Luchtvaartnieuws Magazine, the biggest aviation magazine in the Benelux.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.