JNJ and KO are two of my favorite current dividend plays yielding near 3%.

Both are dividend aristocrats/kings and on sale.

The Gordon Growth Model shows both as being undervalued with their exceptionally low betas.

Richard Drury

Dividend growth

The dividend aristocrats are one of my favorite places to hunt for deals and portfolio income. Compound interest of both capital appreciation and a high dividend yield that grows over time is essential to a long-term portfolio that rolls up like a big ball of cash. I love them so much that I literally shotgun blast the list of aristocrats from top to bottom to make sure that I have comprehensive ownership of all names on the list. There are currently 66 names on the list of stocks that have paid and raised dividends for at least 25 years.

Two of my current favorites, Coca-Cola (KO) and Johnson and Johnson (JNJ) have been paying and raising dividends longer than that at more than 50 years each. Based on their low beta and consistent growth, these are two stocks that are worth locking up in the compound interest safe for generations. I'm buying both of these stocks currently in outsized portions for my income portfolio.

SEEKING ALPHA

SEEKING ALPHA

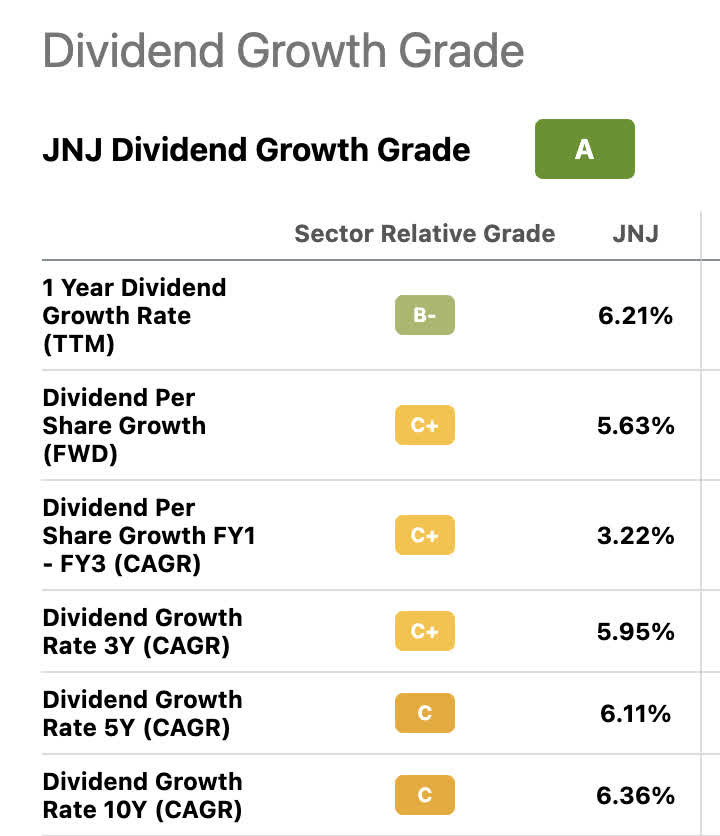

We can see for both Coca-Cola and Johnson and Johnson that the overall dividend scorecard rating is an A for both on Seeking Alpha. We can also see the one-year growth rate on both getting closer to the 10-year CAGR vs the three and the 5-year rates. The uptick in growth is partially good business execution and partially needing to compete with high short-term yields on competing bonds and high-yield savings accounts.

Grabbing good dividend stocks now could wind up being a great deal later if/when the Fed pivots. Bond rates and HYSA yields change with government policy and inflation, but dividends are sticky. Once they're in a place with a traditional payer that increases rates every year, those rates are only going up, not down. The opposite will likely be true on short-term debt and high-yield accounts/CDs.

What they do

Quick looks at the businesses courtesy of Yahoo Finance:

Coca Cola

The Coca-Cola Company, a beverage company, manufactures, markets, and sells various nonalcoholic beverages worldwide. The company provides sparkling soft drinks, sparkling flavors; water, sports, coffee, and tea; juice, value-added dairy, and plant-based beverages; and other beverages. It also offers beverage concentrates and syrups, as well as fountain syrups to fountain retailers, such as restaurants and convenience stores.

Johnson and Johnson

Johnson & Johnson, together with its subsidiaries, researches, develops, manufactures, and sells various products in the healthcare field worldwide. Johnson & Johnson was founded in 1886 and is based in New Brunswick, New Jersey.

Low betas

Johnson and Johnson

yahoo finance

Coca-Cola

yahoo finance

Steady eddy. Both of these betas are ultra-low when compared to the market. There is a reason for this, dividend aristocrats almost always provide a staple product that the economy needs in any environment. They grow with inflation because their products are usually purchased by almost every household. Both Johnson and Johnson and Coca Cola have solid moats with their tentacles piercing every segment of their sectors.

CAPM

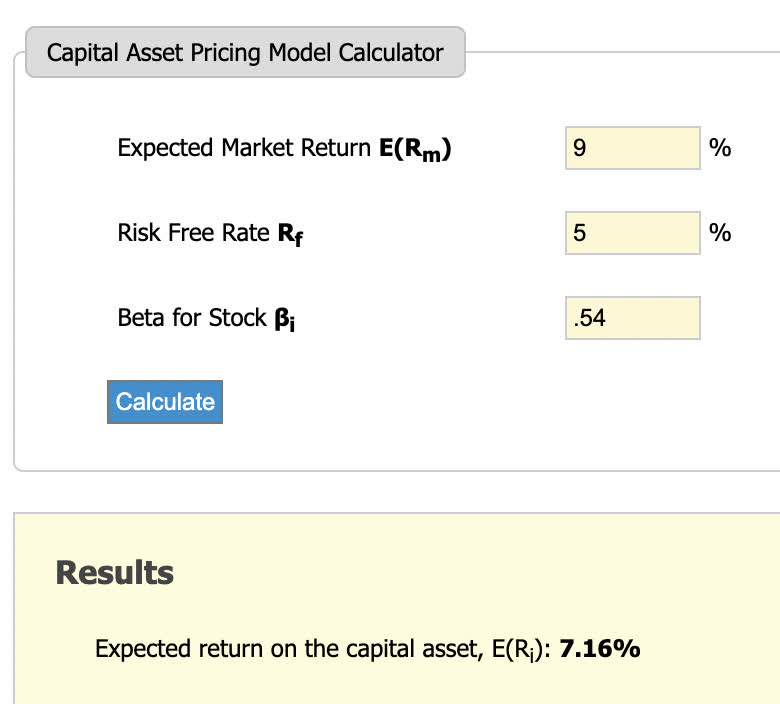

The capital asset pricing model is the first item we will look at for these two SWAN darlings. The low beta of both of these stocks is very bond-like by nature, with both businesses able to grow their businesses and dividend yields along with inflation. Low beta has intangible value as it protects the investor's psychology. Time is our best friend, and when compounding a dividend aristocrat or king, the more steady our brains are, the better decisions we will make. It might not be a coincidence that the very brain waves we need to control, beta waves, are also the type of volatility we are looking to decrease in our portfolios. Sometimes a crossing of vernacular is more than a coincidence.

Coca-Cola CAPM

Our inputs for Coca-Cola will be a market return of 9%, and a beta of .54 with a risk-free rate of 5%:

goodcalculators.com/

Johnson and Johnson CAPM

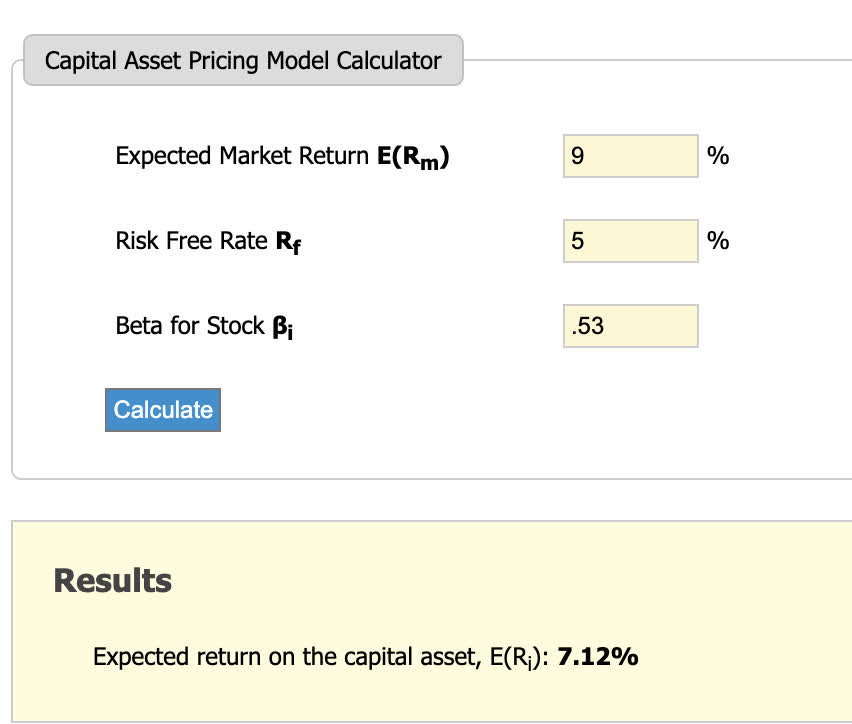

Our inputs for Johnson and Johnson will be a market return of 9%, and a beta of .53 with a risk-free rate of 5%:

goodcalculators.com/

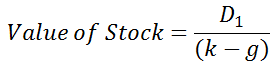

Gordon growth model

The Gordon Growth Model is one of my favorite ways to evaluate low-beta dividend aristocrats and kings. A good layout of the formula can be found here:

Stable Gordon Growth Formula

Using a stable model, we get the value of the stock as below:

wallstreetmojo

Where,

D1: it is next year's expected annual dividend per share

k: discount rate or the required rate of return estimated using the CAPM

g: expected dividend growth rate (assumed to be constant)

For those unfamiliar, the model has been attributed to professor Myron J. Gordon of MIT. It is one of the simplest ways to peg a price target on a dividend stock for which you believe the dividend will be paid and grown for the life of your holding. This is not a model I would use outside of the aristocrats or kings. The formulas can grow more complex when we make more assumptions about the stability of the yield and its growth. Those are not weeds I choose to wade into.

Coca Cola GGG model

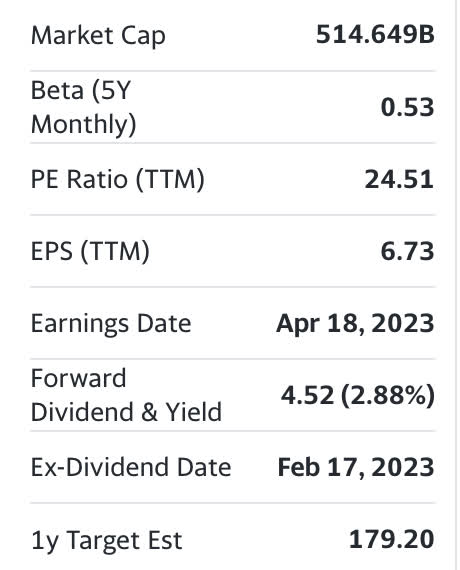

This price takes into consideration the dividend of $1.84/(7.16%-4.34%). The forward dividend growth rate is being used here.

This price takes into consideration the dividend of $4.53/(7.12%-5.63%). The forward dividend growth rate is being used here. While the price may be a bit too optimistic here using this model, Johnson and Johnson appears the most undervalued of the two when looking at the long term dividend growth rates.

Payout ratios for both stocks are high but well-managed. I like to look at the ratios from a free cash flow percentage versus a payout of earnings. Earnings are also a good metric as earnings increase the net worth of a company, which it could borrow against or sell assets should it fall short of free cash flow to cover the dividend. I prefer to look at the payout without having to disrupt the business or take on debt, thus using free cash flow.

As we can see from the above, both dividends are covered by free cash flow but are still a tad high. Both of these companies are no longer in growth mode and the payouts combined with share buybacks are something more akin to the functionality of a REIT (minus the fact that REITS normally add shares rather than subtract them from the market). The benefit here is that qualified dividends will always be taxed at a lower rate than ordinary income from a REIT.

I would be remiss without mentioning the new news regarding possible settlement agreements that are being proposed in the Johnson and Johnson talcum powder case. With $8.9 Billion being proposed as a possible 25 year payment to injured litigants, that's a $356 million hit to free cash flow on an annual basis. With 2.613 billion shares outstanding, that would reduce the FCF per share by 13.6 cents. That would bring the current coverage down to $6.41 a share and a payout ratio of 70.5% of FCF per share. With the payments being spread out over a long period, the risk seems minimal. Keep an eye on this in case the duration or amount changes of course.

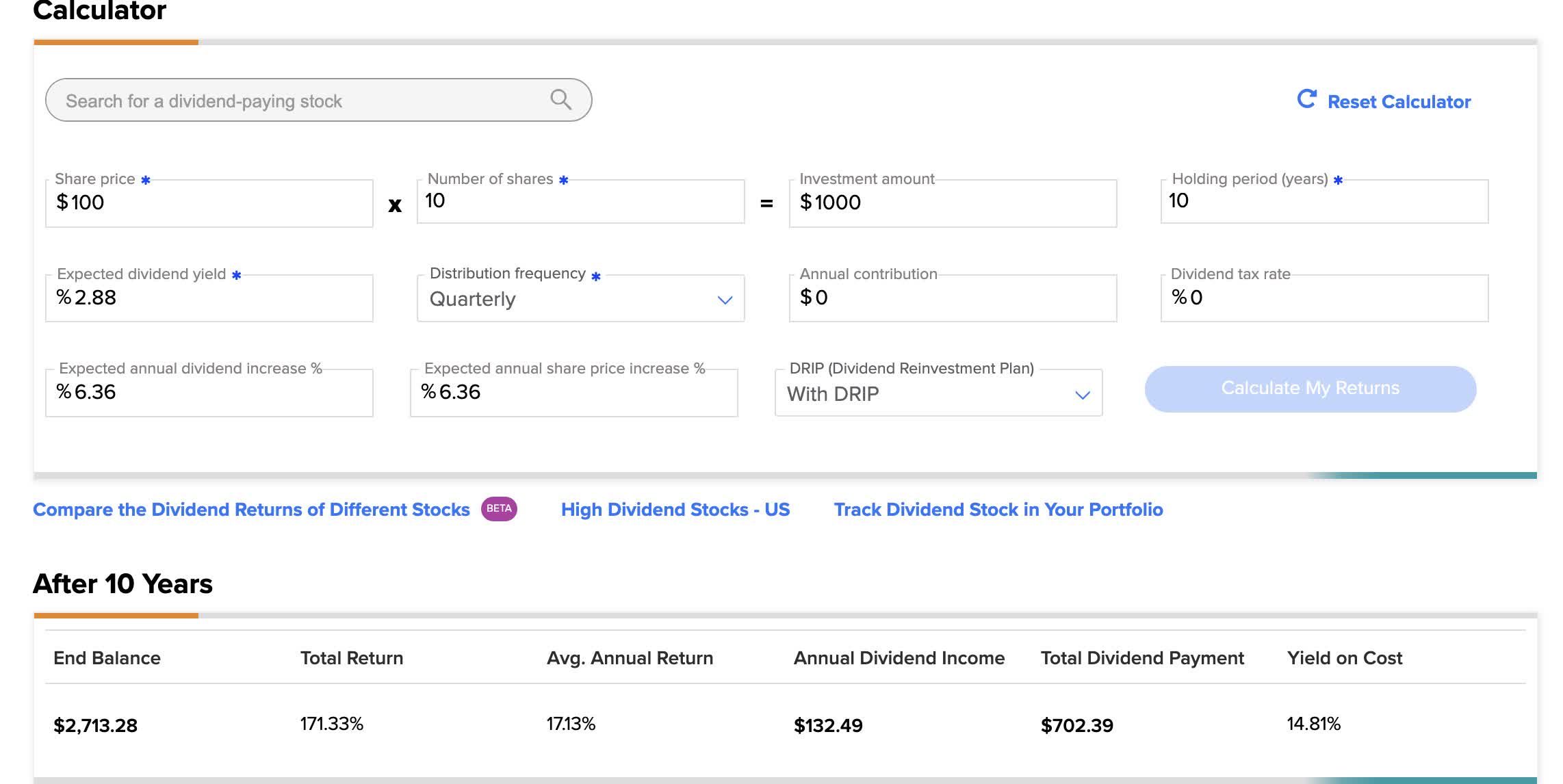

Compound dividend models

It's pretty well accepted that dividend stocks that have low betas tend to have a total return that tracks their yield plus the CAGR in dividend growth rate. The stock appreciation often mimics the dividend growth rate from a conservative assumption. Let's take a couple of looks at $1,000 drip investments for both stocks using their current yields and 10-year CAGR dividend growth, since these are both stocks I certainly intend to hold for 10 years+.

Johnson and Johnson

TIPRANKS

Johnson and Johnson has the highest 10-year growth rate of the two at 6.36%. We are also assuming that the stock appreciates modestly just by tracking the dividend growth rate. Even under these conservative assumptions, an average annual return of 17.13% turns $1,000 into $2713 after 10 years.

Coca Cola

TIPRANKS

Coca-Cola has a lower 10-year growth rate and a higher current yield. Making the same assumptions as Johnson and Johnson, where the appreciation simply tracks the dividend yield increase, you still get an average annual return of 14.79%, turning $1,000 into $2479 after 10 years.

Summary

Both of these stocks are popular dividend picks and for good reason. Stocks that can both pay a good yield and increase that yield year after year are far superior to high-yielding fixed-income or high-yield savings accounts. At current, however, it's hard to blame the investor for being in high-yield savings or money market funds. As rates rise, so do those yields, functioning almost like dividend growth stocks themselves. When the rates turn the other way, I, and investors that have been attracted to the short end of the yield curve, will certainly be returning to putting all of our capital to work in dividend growth stocks for the income-centric parts of our portfolios.

I am buying both of these stocks right now and they continue to grow into larger and larger positions in my portfolio. Both are buys with low betas and amazing records of returning capital to investors. Controlling our beta brain waves with low beta stocks should have satisfactory results. Green tea and decaf coffee help as well. Good luck!

I'm a value investor who enjoys using classical value ratios to pick my portfolio. Long-term focused on low P/B, P/FCF, PEG ratios, the Graham Number and an occasional net-net hunter. I have an MBA, but do not follow valuation methodology promoted by traditional academia. I believe investment philosophy is best learned post University indoctrination, by oneself in the comfort of their own mind. I also believe in self-indexing primarily using the Dow Jones Industrial Average as my index of choice combined with Joel Greenblatt's Magic Formula.I'd like to consider my thought process to be an amalgamation of Ben Graham, Joel Greenblatt, and Peter Lynch. I'm an avid reader with an extensive library of value investment-based books. Many of my articles are effectively book reviews through application.My working background is in private debt financing and real estate. I'm also a fluent Mandarin speaker in both business and court settings. I have spent a good chunk of my adult working life in China and Asia.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of KO, JNJ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

Comments (8)

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.