Bit Digital: Turning Bits Into Bytes

Summary

- Bit Digital presents a unique investment opportunity to invest in the Bitcoin mining business.

- Largely based on its asset-light, lean operating structure, BTBT presents a more robust business model than most of its peers.

- We initiate with a Buy Long-Term rating and a $3.00 price target.

- Looking for a portfolio of ideas like this one? Members of Best of the Uncovereds get exclusive access to our subscriber-only portfolios. Learn More »

I going to make a greatest artwork as I can, by my head, my hand and by my mind.

Investment Thesis

Bit Digital (NASDAQ:BTBT) is a franchise that specializes in digital asset mining, specifically in the Bitcoin (BTC-USD) mining business, through its wholly-owned subsidiaries in the United States and Canada. Incorporated in 2017, BTBT's mining facilities operate with the intent of accumulating Bitcoin and Ethereum (ETH-USD) and seek to sell for fiat currency opportunistically depending on market conditions. Started as a peer-to-peer lending business, BTBT now has become a mainstay cog in the global adoption of blockchain technology, especially in terms of its application to Bitcoin production. Additionally, the company has recently entered Ethereum staking, thereby diversifying its digital asset mining business.

While there has been volatility in the price of Bitcoin, there's no debate, from our perspective, about its long-term value. As the economy increasingly relies on digital means of payments, e-commerce, and globalization, the digital currency system, which suffers from a double-spending problem, is not equipped with the growing complexity of current economic demands and a growing public desire to partake in a completely decentralized financial system. We believe Bitcoin and other cryptocurrencies are here to not only fill that void but also serve other facets of the financial system.

Apart from institutionalizing Bitcoin mining, which offers economies of scale, BTBT has incorporated a cost advantage (due to its judicious equipment procurement) and an asset-light strategy (courtesy of its hosting arrangements) into its business model, which differentiates the company from its competition.

Under the leadership of its new CEO Sam Tabar, in 2023, BTBT is poised to make a potentially strong 71% surge in revenues, essentially due to strong growth in Hash rate (to 2.7 EH/s in Q3:22 from 1.6 in Q3:21 - almost a 70% increase), positive momentum in the Bitcoin price (a 47% increase since FY:22 year-end) and the company's recent thrust in the Ethereum staking business. We expect the expansion to be fully reflected in gross margin expansion and EBITDA margin recovery.

We initiate coverage with a Buy long-term rating and a $3.00 price target (a 50:50 hybrid of an EV/revenue valuation of $2.72 and a book value-based valuation of $3.22), implying a capital appreciation potential of almost 110%).

Economic Prospects of Bitcoin Remain Strong

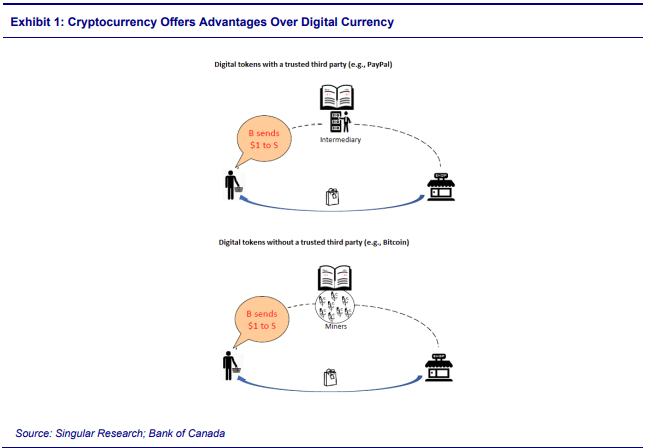

Global economies are relying increasingly on digital means of payments. Almost 90% of Americans are now using some form of digital payments, and digital-payments penetration increased to 89% in 2022. With increasing market penetration of e-commerce, the global adoption of digital means payments will continue to rise. The digital currency system, which is essentially a string of bits, suffers from a double-spending problem, in which a digital record can easily be copied and reused for payment. Traditionally, most of the digital payments have relied on a trusted third party, who, for a fee, prohibits double spending. Cryptocurrencies such as Bitcoin have replaced that third party, thereby democratizing the digital payment process by the introduction of a blockchain ledger, which ensures the distributed verification, updating, and storage of the record of digital transactions.

Singular Research; Bank of Canada

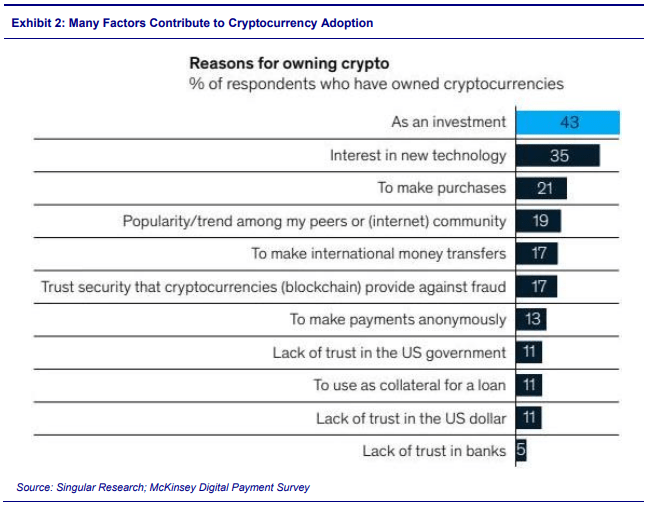

Bitcoins are becoming increasingly mainstream. A recent survey concluded that cryptocurrency is the future of finance. Conducted by the Harris Poll, this recent (October 2022) survey of over 2,000 adults found that nearly half of Americans are familiar with cryptocurrencies. The familiarity was especially higher in young adults, with more than 70% of those between the ages of 18-34 knowledgeable about cryptocurrencies. Increasing interest in cryptocurrencies is at least in part a result of individual investors looking for investment opportunities beyond equities and mutual funds, as over a quarter of Americans saw cryptocurrencies as a means of investment diversification. High inflation also piqued interest in adopting cryptocurrencies.

Singular Research; McKinsey Digital Payment Survey

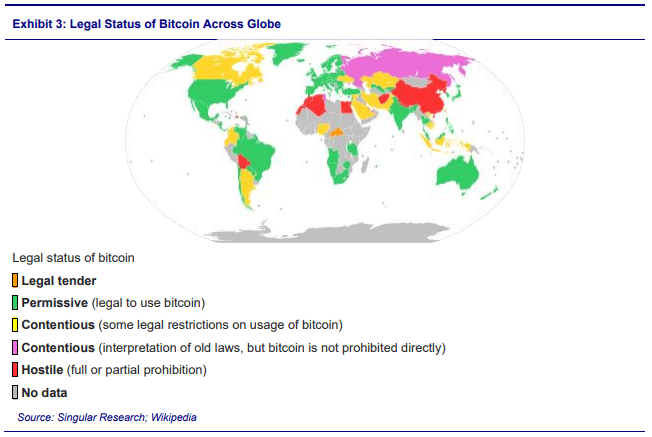

Bitcoin has gained acceptance as legal tender across the globe. As shown in Exhibit 3, various government agencies have classified cryptocurrencies differently - some states have explicitly allowed its use and trade, and others have banned or restricted it. Though the legal status of Bitcoin varies substantially across countries, it's widely adopted globally. The legal status of cryptocurrencies is undefined in substantial parts of the globe, and we believe over time, the legality and usability of cryptocurrencies and Bitcoin as a means of payment will increase. We note that unless Bitcoin is explicitly prohibited by the central bank of a country, it's up to vendors to accept it as a legal tender for sundry goods. As the usage of Bitcoin increases globally, especially for international trade, the risk a vendor does not accept Bitcoin decreases. On the flip side, though a ban on Bitcoin by central banks in China is a major impediment to the currency's global adoption and considering China's large population of 1.4 billion residents and status as the second-largest global economy, we emphasize that the ban on Bitcoin is not a referendum on utility of cryptocurrencies, but rather an affirmation of its broadening economic prospects, as it is widely speculated that China's ban was motivated by its own interests to support its own government-controlled cryptocurrency. Ever since El Salvador's adoption of Bitcoin as legal tender in June 2021, several developing countries have followed suit. These nations see Bitcoin acquiescence as a means of global financial inclusion that can foster investment, innovation, and economic development. So, we believe that cryptocurrencies are an integral part of the global financial system.

Singular Research; Wikipedia

Bitcoin has gained traction in other facets of the financial system as well. Last year, Fidelity Investments included Bitcoin as an option for its employees' 401(k) accounts. Similarly, Mastercard (MA) will start allowing merchants to accept Bitcoin over its network. Likewise, Visa (V) has started a reward program in Bitcoin for its credit card customers.

Lean Cost Structure

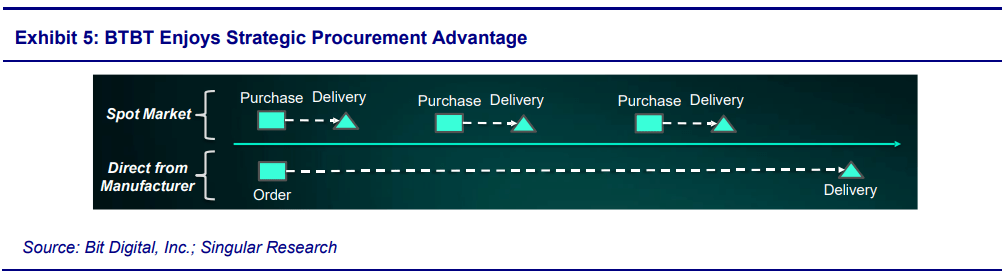

The company's focus on second-hand miners helps keep its cost structure lean. Unlike its competitors, who order brand-new miners from manufacturers, BTBT purchases miners on the spot market. Additionally, the company can deploy these miners into production much quicker than its competitors and hence enjoys one of the shortest purchase-to-deployment lead times in the industry.

Bit Digital, Inc.; Singular Research

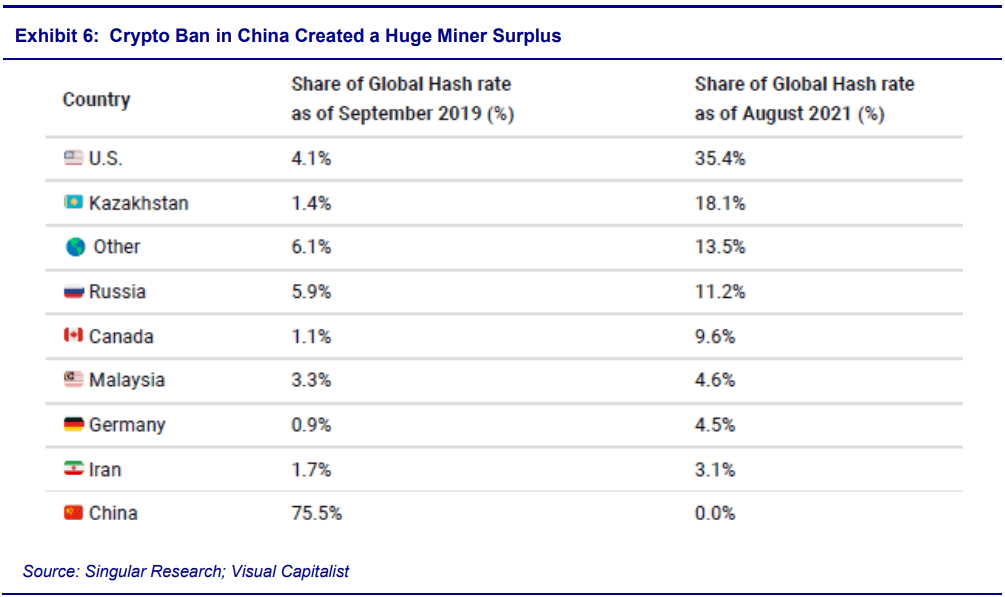

BTBT's deep roots in China were instrumental in building this cost-based competitive advantage. A crackdown on crypto mining in China presented this opportunity - essentially, strict restrictions on mining produced a huge surplus of miners. As the restrictions were implemented, China went from a market that had excess demand for mining equipment to one that had a huge surplus. Many Chinese crypto mining firms had to curtail or even cease operations. Consequently, most Chinese crypto mining firms went out of business, which made a large inventory of miners available at discounted prices in the spot market. Similarly, even manufacturers had to drop prices on new miners. Leveraging this anomaly, BTBT was able to purchase miners opportunistically from China. BTBT's North America-based competitors did not have this sourcing advantage and hence are exclusively dependent on more new miners that they buy directly from manufacturers. BTBT, on the other hand, had relationships throughout China that provides it unfettered access to new and used machines. By doing so, the company has managed to build a cost-effective fleet of miners.

This dynamic continued throughout 2021 but played out by the end of H1 2022 when BTBT had fulfilled most of its mining equipment requirements. Interestingly, however, in H2 2022, as the Chinese procurement advantage disappeared, opportunity opened in the U.S. Due to the collapse of the price of Bitcoin last year, a secondary market for mining equipment took shape and developed. As a result of difficult economics of Bitcoin mining at that time, several BTBT competitors faced liquidity issues and some faced bankruptcy. Some of these competitors sold their mining equipment in the secondary market at distressed pricing, and companies like BTBT, which conserved a robust balance sheet, have been able to procure equipment opportunistically. Therefore, we believe a comparative cost advantage will likely continue in the near future.

Singular Research; Visual Capitalist

Outsourced Business Model

In addition to cost advantages the company enjoys due to its strategic procurement of equipment, it has instituted certain other measures that keep its fixed costs down. Importantly, these measures help the company remain focused on Bitcoin mining and not engage in other vertical industry activities like hosting and power management. Following this strategy, the company is able to limit its spending elsewhere and focus on just equipment, as discussed in the previous section, instead of maintaining direct relations to power suppliers and related infrastructure vendors.

Under hosting arrangements, BTBT's miners are maintained by third-party hosting companies that install and operate miners, provide IT consulting, maintenance, and repair work on-site. The third parties that the company has engaged in include Core Scientific Inc., Blockfusion USA Inc., Coinmint LLC, Digihost Technologies Inc., and Blockbreakers Inc. In addition to these hosting agreements, BTBT has further engaged in rate swap agreements with companies such as Riot Blockchain Inc.

As of Q3 2022, BTBT has hosting arrangements in place of 228 MW, which provides the company enough hash power to support growth to over 6 EH/s.

Investment Risks

- As a company that's engaged in the Bitcoin mining business, BTBT is exposed to fluctuations in Bitcoin prices, which affect both its profitability and valuation.

- BTBT has a substantial amount of cryptocurrency as part of its current assets on the balance sheet. A steep decline in cryptocurrencies held by the company could lead to weakening of the financial condition of the company.

- The company is currently not free cash flow positive, so the firm might need additional capital infusions to fulfill its operational needs.

- The company's operations and the cryptocurrencies held in inventory are vulnerable to cybercrime. Fintech companies and holders of cryptocurrencies are frequent targets of sophisticated hackers. A successful cyberattack could disrupt BTBT's operations.

- The cryptocurrency industry has made significant headway in several facets of the financial industry, but it's far from becoming a mainstream financial instrument. The company's long-term prospects hinge on cryptocurrencies becoming mainstream. Though we believe cryptocurrencies are gaining adoption, but if the momentum stalls and its usage remains limited to the early adopters, BTBT's long-term prospects will diminish.

- The cryptocurrency industry is increasingly coming under financial regulatory preview. Some governments have been proactive in adopting regulations, but others have essentially shunned cryptocurrencies altogether due to complex regulatory requirements. Evolving and unpredictable regulations that may be imposed on cryptocurrencies could pose a business risk to BTBT.

Valuation

We value BTBT using a combination of multiple based on industry peer companies (an EV/revenue multiple) blended with a balance sheet-based intrinsic valuation to derive a fair value target price for the company.

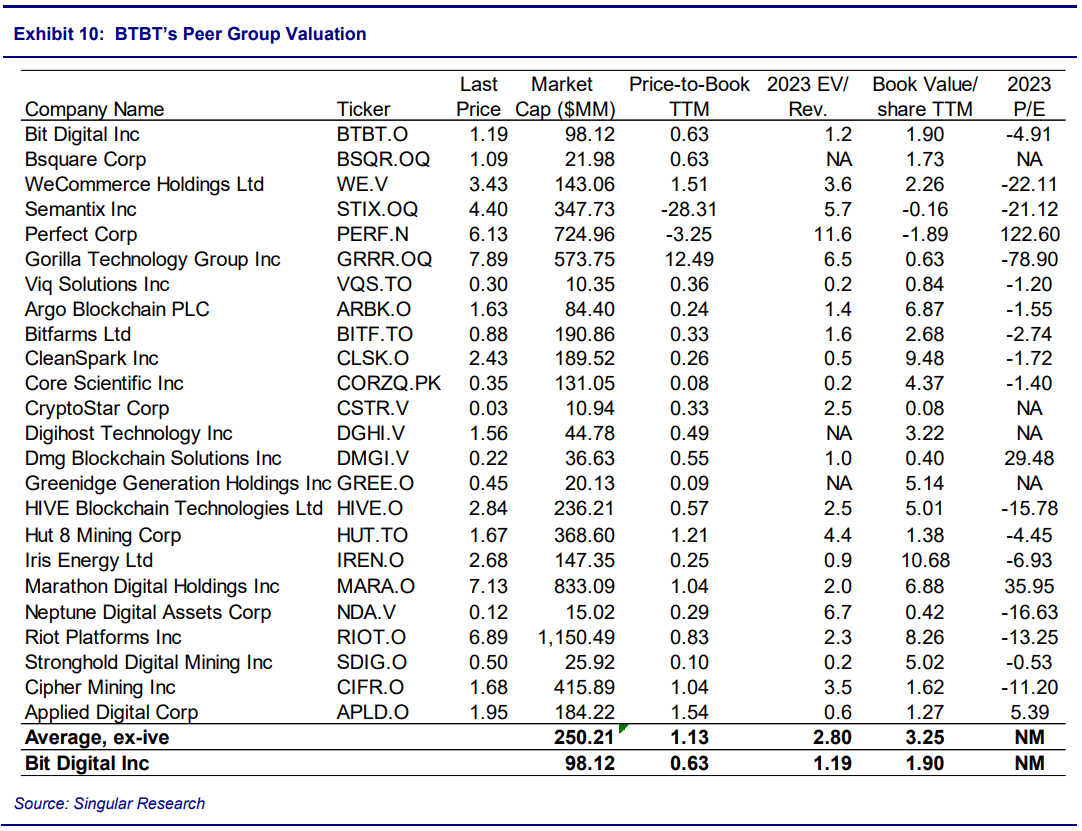

In terms of the peer group, as shown in Exhibit 10, most of BTBT's peer companies are not profitable - with negative earnings, and hence a P/E valuation would not be appropriate. Similarly, most of BTBT's peers are not operationally profitable, making an EV/EBITDA valuation also not suitable. Therefore, we believe EV/Revenue would be the best multiple for the company. The Cryptocurrency peer group is currently trading at a 2.80x forward EV/Revenue multiple. We ascribe BTBT an EV/revenue multiple of 3.50x, a 25% premium to its peer group, essentially due to superior growth prospects and a better business strategy. Based on an EV/revenue multiple of 3.50x, we value BTBT at $2.72.

Singular Research

We also value the company using a book value-based valuation. As shown in Exhibit 10, the peer group is trading at 1.13x, trailing twelve-month book value. Attributing a 1.69x multiple, a 50% premium to the peer multiple, essentially due to its stronger balance sheet and improving cash flow position, based on a book value/share of $1.90, we value BTBT at $3.22.

The combination of $2.72 at 50% and $3.22 at 50% results in a weighted average price target of $3.00, which represents an upside of over 110% as of the closing price of $1.43 on March 23, 2023.

Best of the Uncovereds offers new initiation reports on roughly two dozen companies per year, with a focus on under-followed small and mid caps with significant potential. We provide a quarterly earnings update reports on all companies covered, as well as flash reports on significant news announcements by companies. We go further for members, providing recorded interviews with management teams of covered companies when available and a monthly quantitative based "Market Indicators and Strategy Report."

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BTBT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.