Shell Can Generate Strong Returns In A Transitioning Market

Summary

- Shell plc has a unique portfolio of assets and has continued to generate strong returns despite its investments in changing markets.

- The company is high-grading its core energy portfolio, and it has some substantial assets, especially in integrated natural gas and LNG, which will remain in high demand.

- We expect the company to continue generating double-digit returns in the current pricing environment while protecting itself from a downturn.

- We're currently running a sale for our private investing group, The Retirement Forum, where members get access to portfolios, market alerts, real-time chat, and more. Learn More »

Anski

Shell plc (NYSE:SHEL) is one of the largest petroleum companies in the world, with a market capitalization of just under $200 billion. However, the company has also worked hard to respond to the potential impacts of climate change. As we'll see throughout this article, its unique and distributed assets should enable substantial shareholder returns.

Shell Results

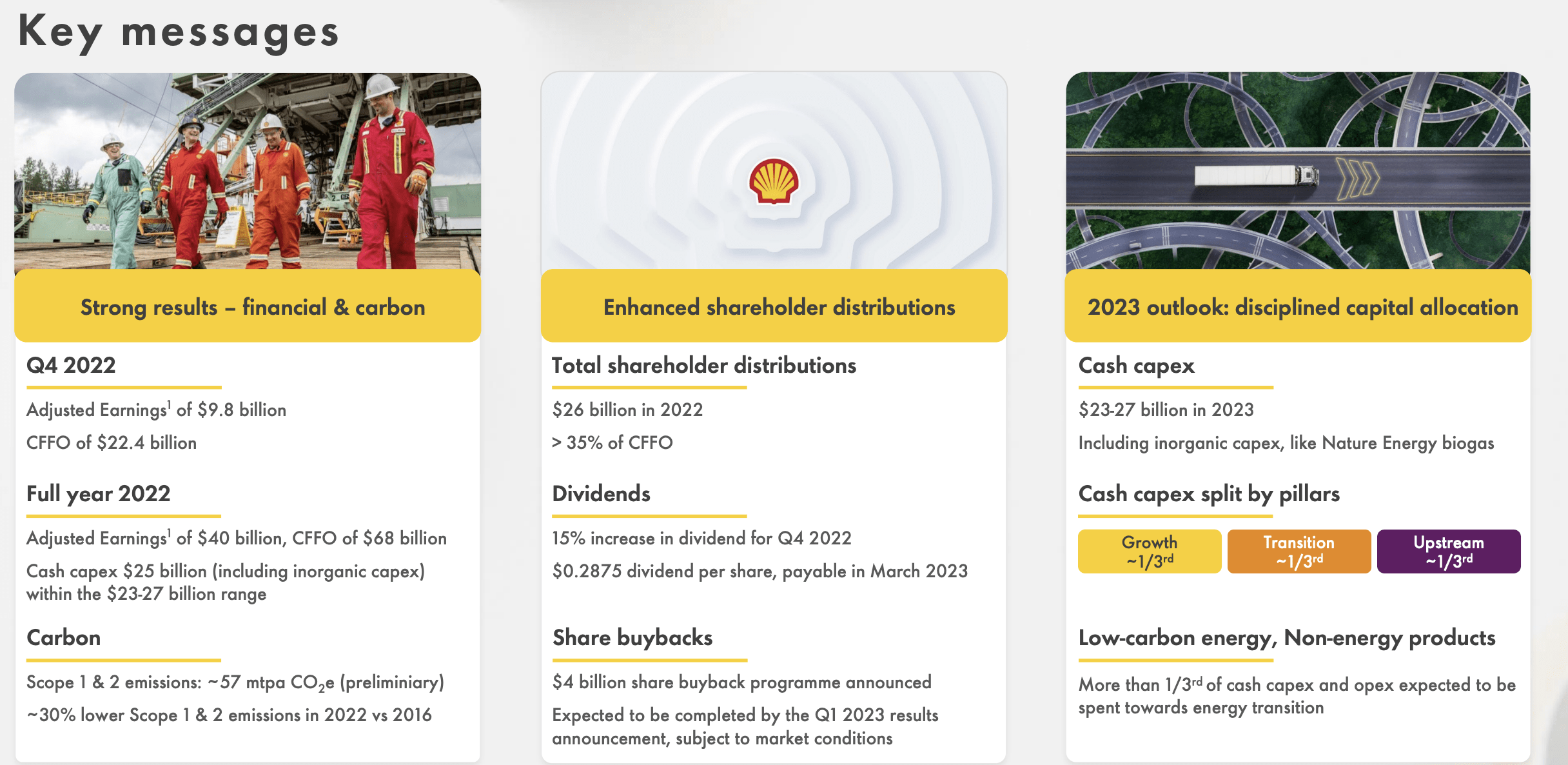

The company achieved strong shareholder returns, taking advantage of higher prices in the most recent quarter.

Shell Investor Presentation

The company earned $9.8 billion in adjusted earnings for the quarter and $22.4 billion in CFFO. For the year, the company had $25 billion in capital expenditures, or $43 billion in FCF after the $68 billion in CFFO. That's a more than 20% FCF yield, highlighting the strength of the company's balance sheet in a quarter with higher average prices.

The company achieved $26 billion in 2022 shareholder distributions, or a 13% shareholder yield. It increased its dividend by 15% and now yields almost 5%, highlighting the strength of its balance sheet. The company announced a $4 billion share buyback that it can comfortably afford, and we expect buybacks to remain strong.

Shell Value Creation

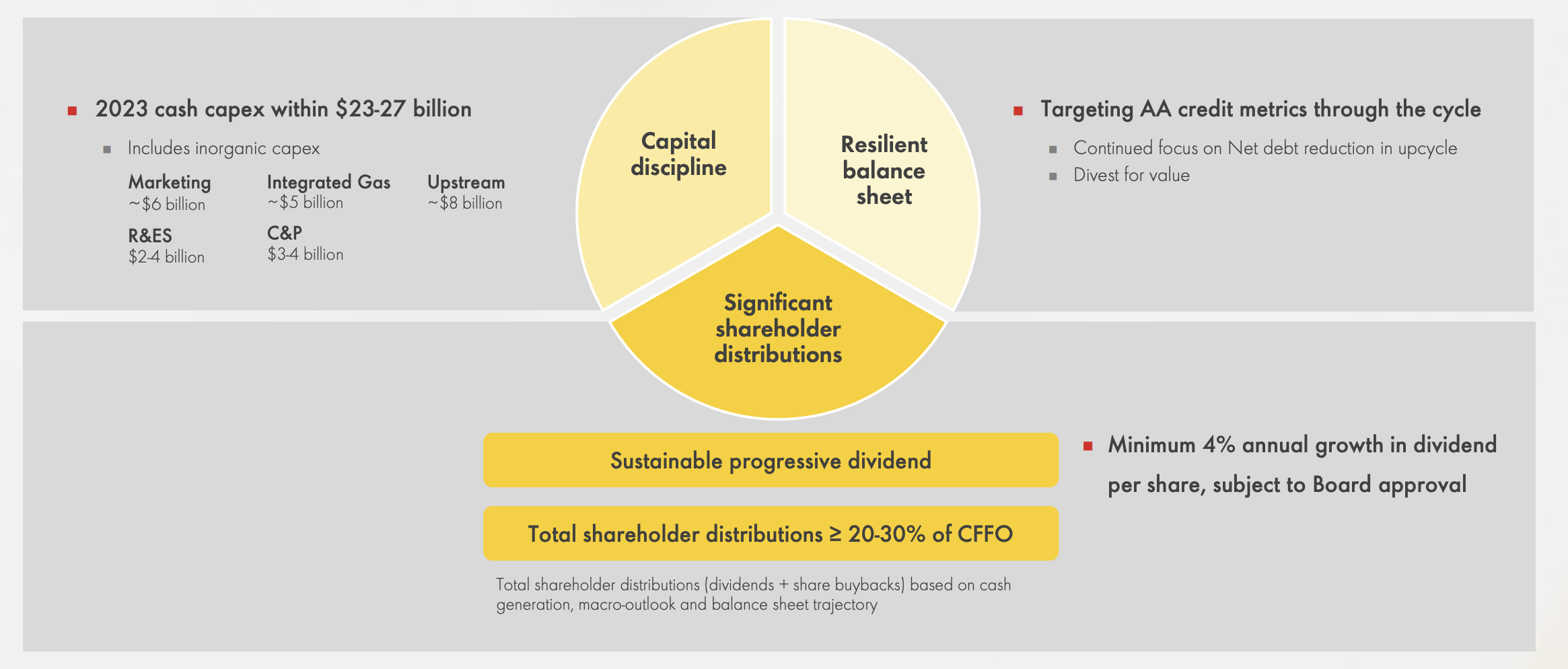

The company is focused on continuing to generate value to shareholders.

Shell Investor Presentation

The company expects 2023 cash capital expenditures to be $25 billion. The company expects to generate AA credit metrics and with the recent announcement of a production cut, we expect prices to remain higher. The company expects minimum 4% annualized growth in its dividend going forward, highlighting its continued strength.

The company's largest source of spending remains its upstream business, and the company is continuing to target shareholder distributions 20-30% of CFFO. We expect the company will be able to generate returns for shareholders in a variety of pricing environments.

Shell Capital Expenditures

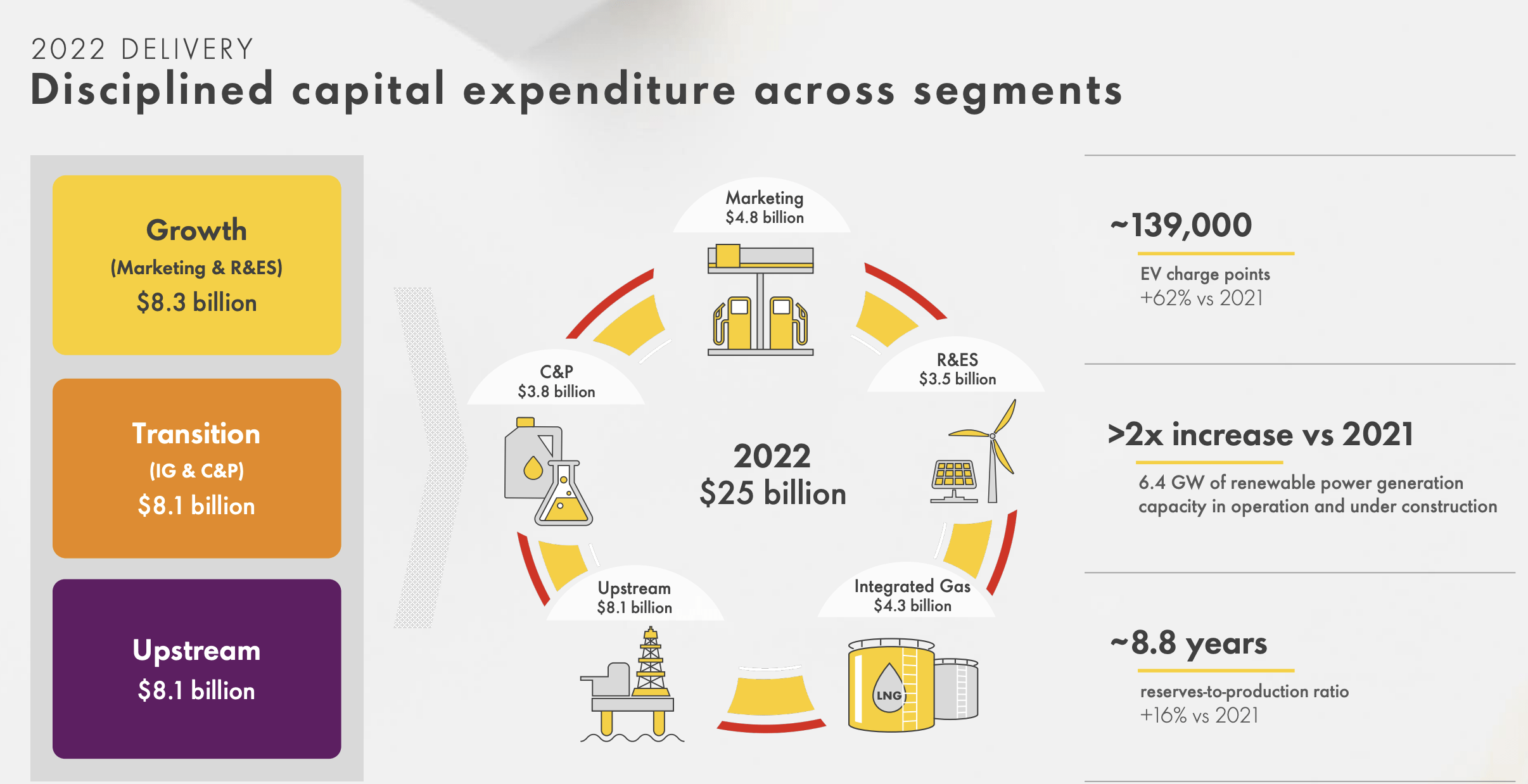

The company is investing heavily in a variety of businesses.

Shell Investor Presentation

The company invested $8.1 billion in upstream in 2022 with record cash flow, but it also built out its transition businesses. It doubled renewable power transition and added 139 thousand EV charge points. Transition spending was at $8.1 billion while growth was at $8.3 billion. In 2023, the company expects spending to be roughly equivalent broken out versus 2022.

Shell Investor Presentation

The potential rewards for shareholders are based on the company's pipeline of major projects. There are many of major upstream projects coming into service in 2023-2024. These projects will together result in hundreds of thousands of barrels/day attributable to the company, especially in Brazil and the USA.

Additionally, the company has a number of major renewable products, which will increase its attributable renewable production and earnings. The company is high-grading its portfolio, and we expect strong returns from invested capital.

Our View

As much as some oil companies like to deny it, the markets are changing. Even if you don't agree with the impacts of climate change, if it changes the demand business and enough research is done to lower the cost of alternatives, it still changes the market. We expect natural gas demand to remain strong for electricity, but crude oil demand to decrease.

However, the substantial decrease in the production of oil wells, means that only capital spending needs to decrease without companies losing money. Shell has done an impressive job of both maintaining strong production and investing in alternative fuel sources, and we expect that to result in strong and diversified shareholder returns.

The company has a more than manageable debt load, a strong and increasing dividend, and continued share buybacks. All of that means the company can generate double-digit shareholders, making it a valuable investment.

Thesis Risk

The largest risk to our thesis is crude oil prices. At Brent prices of more than $80/barrel, with OPEC+'s recently announced production cut, we expect Shell will be very profitable. As prices drop to less than $60/barrel, however, that story changes. Prices have dropped substantially before, and it could happen again.

Conclusion

Oil prices have slowly trended down since they peaked after Russia's invasion of Ukraine. However, they've started to recover recently, and OPEC+'s recent production cut is a major benefit for the market and shows an indication to want to support prices at $70-80 minimum. That's a level where Shell is very profitable.

Shell plc can continue to afford its dividend of more than 4%, which it intends to increase each year. At the same time, the company is continuing to commit to share buybacks. That combination could result in double-digit shareholder returns, making Shell plc a valuable investment. Let us know your thoughts in the comments below.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

You Only Get 1 Chance To Retire, Join The #1 Retirement Service

The Retirement Forum provides actionable ideals, a high-yield safe retirement portfolio, and macroeconomic outlooks, all to help you maximize your capital and your income. We search the entire market to help you maximize returns.

Recommendations from a top 0.2% TipRanks author!

Retirement is complicated and you only get once chance to do it right. Don't miss out because you didn't know what was out there.

We provide:

- Model portfolios to generate high retirement cash flow.

- Deep-dive actionable research.

- Recommendation spreadsheets and option strategies.

This article was written by

#1 ranked author by returns:

https://www.tipranks.com/experts/bloggers/the-value-portfolio

The Value Portfolio focuses on deep analysis of a variety of companies across a variety of sectors looking for alpha wherever it is to maximize reader returns.

Legal Disclaimer (please read before subscribing to any services):

Any related contributions to Seeking Alpha, or elsewhere on the web, are to be construed as personal opinion only and do NOT constitute investment advice. An investor should always conduct personal due diligence before initiating a position. Provided articles and comments should NEVER be construed as official business recommendations. In efforts to keep full transparency, related positions will be disclosed at the end of each article to the maximum extent practicable. The majority of trades are reported live on Twitter, but this cannot be guaranteed due to technical constraints.

My premium service is a research and opinion subscription. No personalized investment advice will ever be given. I am not registered as an investment adviser, nor do I have any plans to pursue this path. No statements should be construed as anything but opinion, and the liability of all investment decisions reside with the individual. Investors should always do their own due diligence and fact check all research prior to making any investment decisions. Any direct engagements with readers should always be viewed as hypothetical examples or simple exchanges of opinion as nothing is ever classified as “advice” in any sense of the word.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SHEL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.