Micro-Cap Energy Stocks Ranked By Quality

Summary

- Twenty-one micro-cap energy producers were evaluated using a quality matrix with factors including Price/Sales, YOY Revenue Growth, Net Income Margin, Free Cash Flow Margin, and Total Debt/Market Cap.

- I would advise only those investors with a high risk tolerance to consider micro-cap energy producers.

- The micro-cap producers discussed here may be particularly exposed in the event of further commodity declines or economic contraction.

- Investors are once again cautioned to consider every investment carefully and on its own merits; diamonds can quickly morph into teardrops.

tiero/iStock via Getty Images

Author's Note: This review is a follow up to The Largest Global Energy Companies Ranked By Quality wherein I reviewed world's largest energy companies using a quality matrix. I intend to complete the series evaluating small and mid-cap producers in future analyses.

If Teardrops Were Diamonds

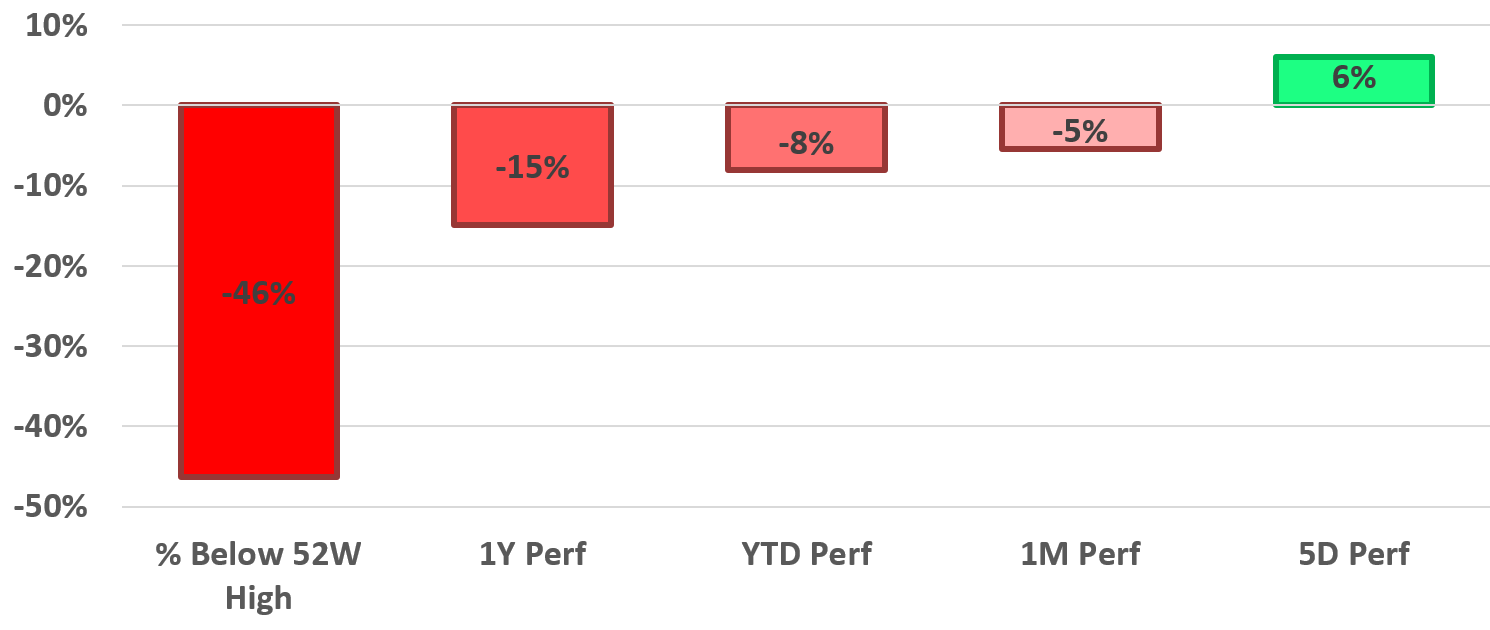

Seeking Alpha's stock screening tool was used to assemble a list of 21 micro-cap energy producers with market caps between $50M and $300M. The average performance of these energy producers is summarized in the table below.

Micro-Cap Energy Producers: Average Performance 1YR

Author, SA Data

Here's where the bitter teardrops start flowing, particularly for those investors who bought near the 52 week high of many of these micro-caps. The average energy producer analysed is down 46% with relation to its 52 week high. As a group, they are down over every period except the last five days; most recently the group has climbed 6%. Regardless of whether an investor is trying to manage a losing position or shopping for a bargain, it would be advantageous to first identify the likely diamonds in the group.

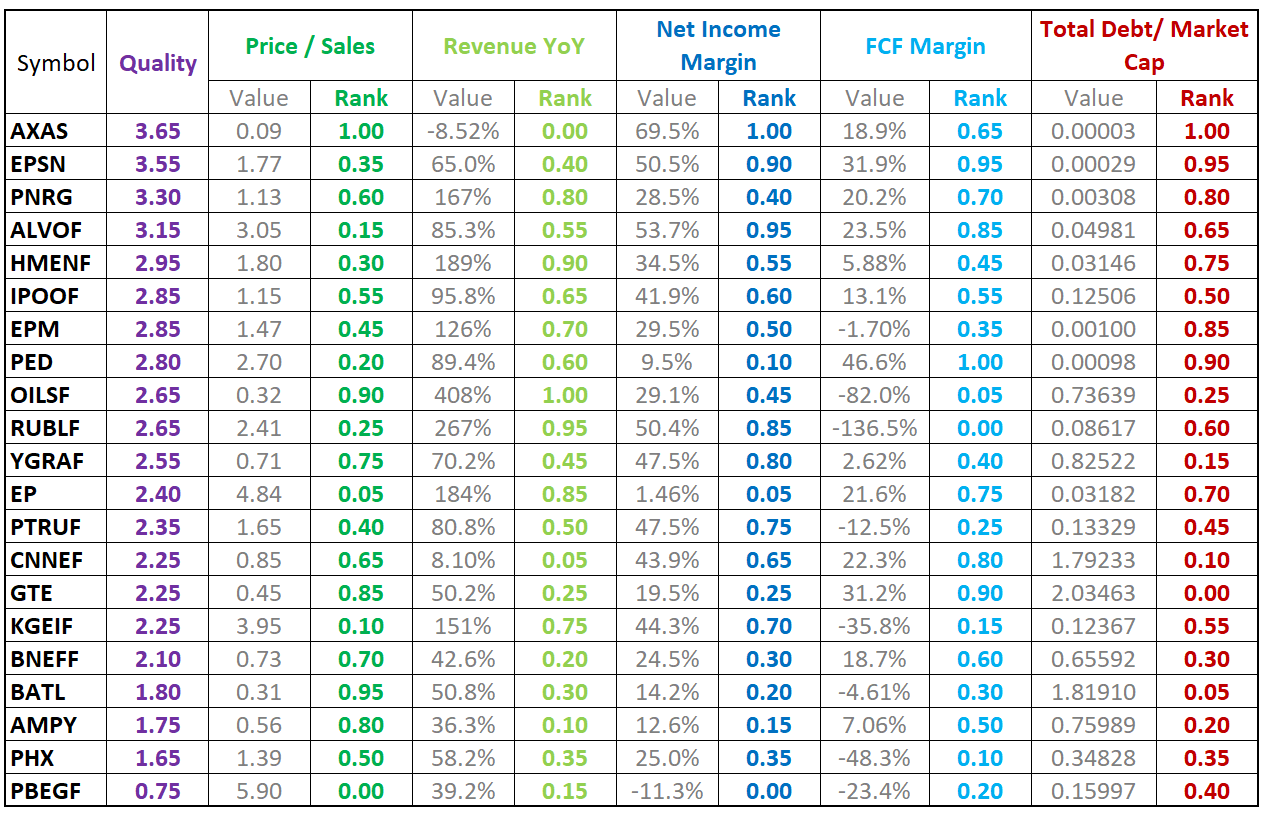

Relative Quality Evaluation

The 21 micro-cap energy producers were evaluated using a quality matrix with factors including Price/Sales, YOY Revenue Growth, Net Income Margin, Free Cash Flow Margin, and Total Debt/Market Cap. The values for each company's factors were normalized by means of statistical percent ranking with relation to the group. The quality matrix was calculated as the sum of the percent ranks of the factors.

Quality Matrix Chart

Author, SA Data

The above chart is sorted in descending order of the best quality (highest matrix score) to the poorest quality (lowest matrix score).

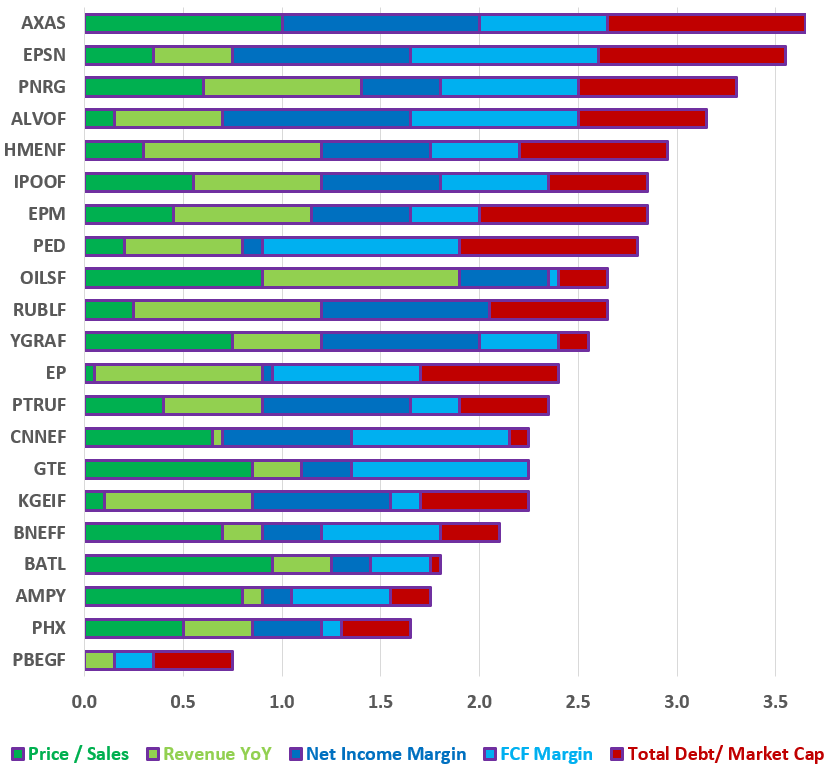

Quality Matrix Plot

Author, SA Data

The quality matrix is presented graphically in the stacked bar chart above with cumulative inputs for each factor. Based on this analysis, the diamonds in the group are likely to include: Abraxas Petroleum Corporation (OTCPK:AXAS), Epsilon Energy Ltd (EPSN), PrimeEnergy Resources Corporation (PNRG), Alvopetro Energy Ltd. (OTCQX:ALVOF), Hemisphere Energy Corporation (OTCQX:HMENF), InPlay Oil Corp. (OTCQX:IPOOF), and Evolution Petroleum Corporation (EPM).

AXAS appears compelling (with caveats) in the top spot despite negative revenue growth YOY with top ranking in Price/Sales, Net Income Margin, and debt. In early January 2022, AXAS became a pure-play Delaware Basin producer when it sold its Williston Basin Assets and used the proceeds to repay the entirety of its revolving credit facility. However, only 10% of shares are owned by individuals after investor Sardar Biglari acquired 90% of the company in October 2022. Further, it would be exceptionally difficult to build a position as less than 4000 shares (about $2500 market value) were traded on March 31st.

Quality Matrix Limitations

Investors should consider the quality matrix a screen only. The matrix and its factors, normalization method, and weights could all be adjusted and yield different results. Further, the matrix is based on the most readily available and common metrics. These metrics can change rapidly with share price or as new company reports are released. It does not include company-specific data available in quarterly reports and presentations. The quality of a producer's reserves, planned Capex, expected production, and hedging are amongst the factors not addressed here. Every investment decision regarding an individual equity should be based on comprehensive analysis of that equity.

Conclusions and Recommendations

Investors are once again cautioned to consider every investment carefully and on its own merits; diamonds can quickly morph into teardrops. Broadly speaking, energy producers and particularly the small producers discussed here may be particularly exposed in the event of further commodity declines or economic contraction.

I would advise investors with a high risk tolerance to consider micro-cap energy producers even those with the highest quality scores. Setting aside AXAS, the diamonds in the group appear to be; EPSN, PNRG, ALVOF, HMENF, IPOOF, and EPM.

If teardrops were diamonds and only mine were used, they could pave every highway coast to coast. - Dwight David Yoakam

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of GTE either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.