ALTY Has Some Advantages In A Higher Volatility Environment

Summary

- A lot of ALTY is invested in buy-write strategies that work pretty well in higher volatility environments.

- Moreover, rates are likely approaching their peaks sooner rather than later, and therefore the longer duration exposures aren't as bad.

- The MLP exposures also may make good sense right now as high, stable yield works while risk free rates peak due to the potential onset of credit declines.

- Expense ratios are a little high, and the yield puts pressure on NAVs, but it's not a bad pick, it would seem.

- Looking for a helping hand in the market? Members of The Value Lab get exclusive ideas and guidance to navigate any climate. Learn More »

Torsten Asmus

The Global X Alternative Income ETF (NASDAQ:ALTY) provides relatively appropriate income strategies for both a volatile and potentially rate-peaking environment. While the high yield does mean that AUM declines with large redistributions, the banking sector stresses are a good set up for underlying yield from ALTY both as duration risks diminish as well as volatility in equity markets support the buy-write option strategy that some of ALTY's biggest allocations use. The instrument is probably not the best over longer-terms, as the distributions of capital are high, not necessarily fundamentally supported, and destroy value due to withholding taxes, but over short-to-medium term periods it could make a lot of sense right now.

ALTY Breakdown

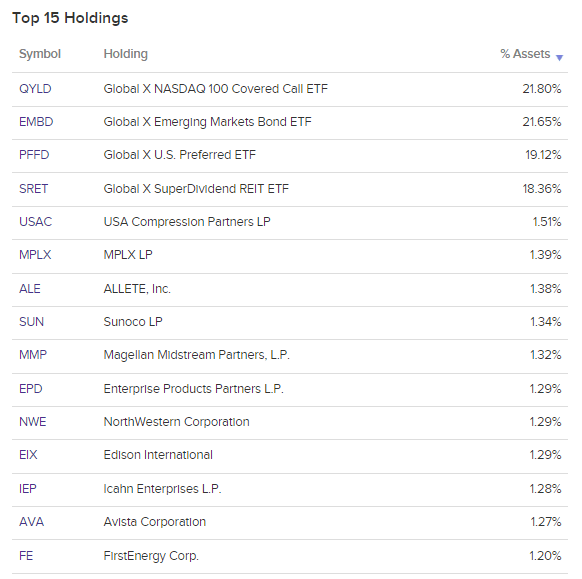

ALTY is composed primarily of other ETFs that follow income strategies with the balance being mostly MLPs in the US focused on the pipeline industry from the shale basins.

ALTY Top Holdings (Globalxetfs.com)

The Nasdaq 100 Covered Call ETF (QYLD) follows a buy-write strategy for a pretty standard looking value weighted portfolio of tech stocks that drive the majority of US market returns. The strategy is to write pretty short duration call options that rollover monthly and then buy stock in the same companies in order to hedge the unlimited liability risk, where the ETF looks for yield from writing options and where writing terms are better in periods of greater market volatility, where the long-value of call options would be higher.

Outside of the QYLD, the exposures are focused on preferred shares and bonds which have been subject to pretty substantial duration risk as these are very long-term securities. This has been bad as rates rise.

Besides those exposures are ETFs that are focused on high yielding dividend stocks or MLPs in the US that are focused on the pipeline business for transporting oil and other liquid products from shale basins to end customers through their infrastructure.

Bottom Line

While QYLD makes sense in a more volatile environment, as there is more scope for writing calls for a good yield, the longer duration instruments also have a certain logic considering the macroeconomic backdrop. Markets should be pretty concerned about the situation in banking stocks these days. Tightening credit conditions is what the Fed has been looking for, and hopefully this will start to do a number on demand conditions and drive down inflation, allowing for rate hikes to end. While it may not happen exactly now, it could be soon, and longer-duration instruments are starting to make a lot more sense. With commercial real estate being the next line of vulnerabilities at US banks, we could see more catalysts for credit tightening and more deflationary pressures. Stable incomes from MLPs whose revenues should be quite market agnostic, and income from hedged and countercyclical strategies, makes a good deal of sense - as well as the bets on duration.

Expense ratios are quite high at 0.54%, and because of the commitment to high yields, the ETF pays out more yield than it can actually support with its underlying instruments at 8%. With over-distribution that gets taxed away, there is going to be long-term declines in AUM and value, but the yield could still be attractive as an interim play around the rate peak as a speculative instrument. Still, there would be better and sharper ways to play for higher total return around rate peaks speculation than ALTY like direct exposure to fixed income or preferreds in credit-safe industries.

Thanks to our global coverage we've ramped up our global macro commentary on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We've done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it's for you.

This article was written by

Formerly Bocconi's Valkyrie Trading Society, seeks to provide a consistent and honest voice through this blog and our Marketplace Service, the Value Lab, with a focus on high conviction and obscure developed market ideas.

DISCLOSURE: All of our articles and communications, including on the Value Lab, are only opinions and should not be treated as investment advice. We are not investment advisors. Consult an investment professional and take care to do your own due diligence.

DISCLOSURE: Some of Valkyrie's former and/or current members also have contributed individually or through shared accounts on Seeking Alpha. Currently: Guney Kaya contributes on his own now, and members have contributed on Mare Evidence Lab.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.