Alibaba Stands To Lose Its Cloud Crown In 2023

Summary

- Alibaba stands to lose its cloud leadership in China.

- Alibaba remains attractive and cheaply valued when compared to Western alternatives.

- Alibaba stands to gain from China's post-COVID economic reacceleration.

- However, if it loses its cloud leadership, it's likely that a cloud premium can no longer be ascribed to Alibaba. And there are much cheaper Chinese alternatives.

- Looking for a helping hand in the market? Members of Idea Generator get exclusive ideas and guidance to navigate any climate. Learn More »

metamorworks/iStock via Getty Images

There is something I already talked about in the past, in an article where I turned less positive on Alibaba (NYSE:BABA). The theme was that the Chinese mobile telephony companies were growing their cloud businesses at an incredible pace and were taking cloud share from Alibaba. This was making it hard for Alibaba’s cloud segment to grow.

This trend, motivated by State-linked entities favoring SOEs (State-Owned Enterprises) cloud services due to national security considerations, has continued. Of course, in spite of the private sector’s expansion in China, the public sector remains very large, not just in terms of the central and local administrations, but also due to a large presence of enterprises where the State owns significant equity stakes.

The trend has continued to such an extent, that it motivates today’s article. The reason is simple: there’s a high likelihood Alibaba will lose its cloud leadership in China already in 2023. This loss will happen to China Telecom’s cloud operations. Let’s see why.

Current And Prospective 2023 Cloud Segment Sizes For Alibaba And China Telecom

As of 2022, projecting Alibaba’s cloud revenues to a full year (from the latest reported 9M results), we have Alibaba’s cloud operations at around RMB78.2 billion ($11.3 billion with USD/RMB @ 6.90), growing around 3% yoy (year-on-year).

As for China Telecom, it just reported its 2022 cloud revenues as being RMB57.9 billion ($8.4 billion). However, these grew 108% yoy, after also growing at 102% yoy the year before.

Hence, as of 2022, Alibaba‘s cloud operations were still much larger than China Telecom’s. However, China Telecom was growing much, much faster than Alibaba.

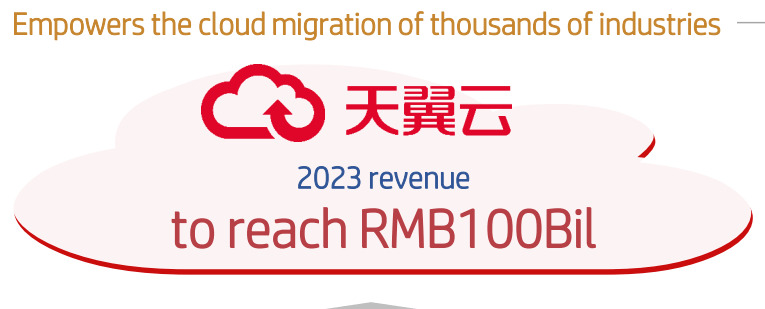

Now, here’s the problem for 2023. China Telecom has guided its 2023 cloud segment to grow to RMB100+ billion ($14.5+ billion), up 70%+ yoy:

China Telecom

Needless to say, Alibaba’s cloud operations are growing quite slowly (+5% yoy in the 9 months to December 2022, +3% in the last quarter, as per Alibaba's most recent earnings report), and even if its growth accelerates, it’s unlikely that Alibaba’s cloud segment will exceed RMB100 billion in 2023 . This would require Alibaba cloud to grow +28% yoy from its currently rather stagnated state. Alibaba cloud growth is likely to rekindle in 2023 because of China’s COVID reopening, but it’s not at all likely to accelerate to those levels.

Hence, come 2023, China Telecom will become China’s largest cloud provider. And Alibaba will lose that crown.

Why Is Losing The Cloud Crown So Relevant?

This relevance has to do with Alibaba’s “story”. Alibaba is in many ways, China’s Amazon.com (AMZN). Alibaba is China’s dominant eCommerce leader by far. And also its cloud leader. Now, over the past few years, Amazon.com’s valuation has been more and more reliant on its AWS (cloud) segment, not just because of its growth, but also because all of Amazon.com’s earnings now come from the AWS segment (though this ought to be temporary).

Hence, although Alibaba’s earnings come entirely from its eCommerce operations, if the market sees Alibaba as China’s Amazon.com, it naturally highly values its cloud operations as being the equivalent to AWS. And of course, AWS turned out to be Amazon.com’s most valuable asset. So, the same could easily be thought about Alibaba.

Of course, if Alibaba loses its cloud leadership – as it seems set to lose, already in 2023, as explained – then the Amazon.com parallel stops working. Its cloud operations become a lot more mundane, and less deserving of a “dream multiple”, which would now need to be based on a multiple of the segment’s revenues, since Alibaba’s cloud segment isn’t yet very profitable (unlike Amazon.com’s).

Talking About Valuations

It’s not that Alibaba is a very expensive stock. Quite the contrary.

At $100, Alibaba trades for 5.8x EV/EBITDA (due to a large net cash position, as well as investments and its Ant Group shareholding). It also carries a 2023 12.8x Price/Earnings. These aren’t demanding multiples, especially if compared to Amazon.com’s 13x forward EV/EBITDA and 67x forward non-GAAP Price/Earnings. However, these multiples should now reflect mostly Alibaba’s eCommerce market position, and not so much its vanishing cloud leadership – while Amazon.com’s can still comfortably continue to reflect its ongoing AWS cloud leadership. For growth investors, this distinction can be very relevant.

Moreover, within the context of Chinese companies, Alibaba now falls into the position of it possibly being compared with the company that’s taking its cloud leadership away. And in that case, things don’t look rosy from a valuation standpoint.

This is so because China Telecom trades significantly cheaper. At HKD4.00, as quoted in Hong Kong, China Telecom trades for 2.2x EV/EBITDA, 10.6x Price/Earnings and carries an estimated 6.6% 2023 gross dividend yield. It's thus significantly cheaper than Alibaba, yet is set to overtake it when it comes to the cloud segment. It’s not hard to think that growth investors might start shifting their investments from Alibaba to China Telecom as a result.

There’s Also A Final, Interesting, Detail About China Telecom

Not only is China Telecom cheap when bought in Hong Kong, but it might actually be artificially cheap. Why? Because the same China Telecom trades at a 70% premium in Shanghai, when compared to the stock in Hong Kong.

This happens because presently it’s impossible to arbitrage easily between Hong Kong and Shanghai, as the H-shares (listed in Hong Kong) aren’t directly convertible into A-shares (listed in Shanghai) and vice-versa, even though both carry the same rights.

At some point this premium will disappear, and the Hong Kong-listed stock will likely head higher as a result, since it’s a clearly absurdly discounted stock given its prospects.

Conclusion

There are some good reasons to buy Alibaba:

- Alibaba remains the Chinese eCommerce leader and given its nature (mostly a 3rd party marketplace), Alibaba’s eCommerce operations are very profitable.

- At the same time, China will see a significant economic reacceleration during 2023, given the COVID reopening.

- China is promoting consumption as the driver of economic reacceleration, as well as promoting “common prosperity” which should also favor consumption – both of these factors will favor retail / eCommerce.

- Finally, Alibaba remains quite cheap when compared to alternative Western stocks.

However, when it comes to its cloud operations, Alibaba is clearly set to lose its leadership of the Chinese cloud market to China Telecom. This will weaken Alibaba’s overall story.

Also, although Alibaba stock is very cheap when compared to Western alternatives, it’s actually much more expensive than China Telecom when it comes to Chinese alternatives. This is so even though China Telecom is the one displacing it from its cloud leadership in China.

Given all of this, I like Alibaba, but I like China Telecom a whole lot more. That said, China Telecom isn’t available to US investors due to legislative actions taken against it in the US (mostly due to 5G jealousy, in my opinion). The stock does remain available in more rational jurisdictions, though. China Telecom (at its cheapest) trades in the Hong Kong stock exchange. It also trades in Shanghai, but it wouldn’t be rational to buy it there (as it trades 70% more expensively there).

A final note. Breaking Alibaba into several separate entities, as reported in the news yesterday, won’t be as positive now as before the event I describe here became obvious. Sure, Alibaba cloud might still command a premium valuation, but this premium cannot be very large if one has China Telecom as an alternative which is larger and growing massively faster, yet trading for a much lower valuation.

Idea Generator is my subscription service. It's based on a unique philosophy (predicting the predictable) and seeks opportunities wherever they might be found, by taking into account both valuation (deeply undervalued situations) and a favorable thesis.

Idea Generator has beaten the S&P 500 by around 74% since inception (in May 2015). There is a no-risk, free, 14-day trial available for those wanting to check out the service.

This article was written by

Portuguese independent trader and analyst. I have worked for both sell side (brokerage) and buy side (fund management) institutions. I've been investing professionally for around 30 years.

I have a Marketplace service here on Seeking Alpha called Idea Generator that's focused on deep value, real-time actionable ideas based on valuation and catalysts. The Idea Generator portfolio has beaten the S&P 500 by more than 74% since inception (2015).

I can be reached at paulo.santosATthinkfn.com.

Disclosure: I/we have a beneficial long position in the shares of CHINA TELECOM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.