Allied Motion Technologies: Growth Being Achieved At A Cost

Summary

- Although Q4 earnings missed estimates, fiscal 2023 was a blowout year in terms of sales growth.

- Furthermore, organic growth of 12% and a backlog of $330+ million points to further growth going forward.

- We did not get the breakout we wanted, however, which means investors may be looking for more earnings and less leverage in order to price shares higher.

IvelinRadkov

Intro

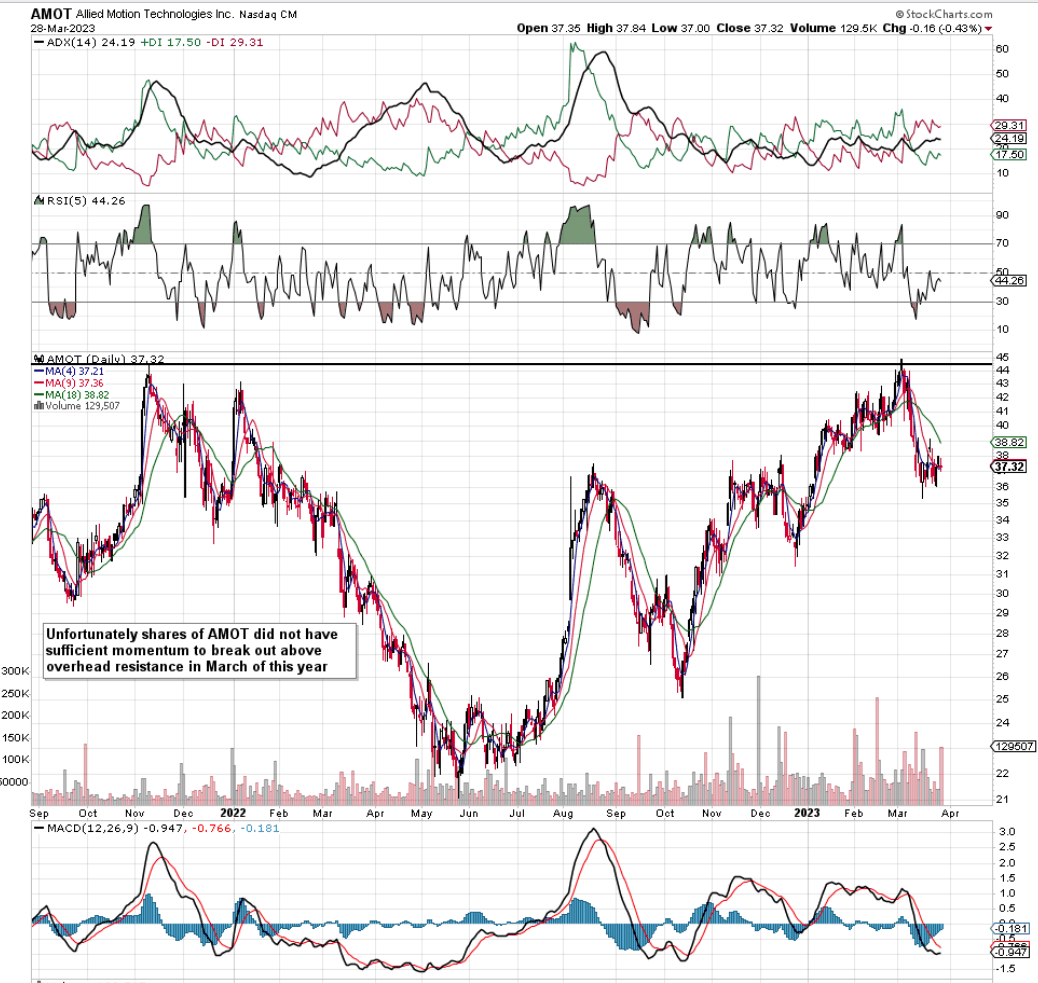

We wrote about Allied Motion Technologies Inc. (NASDAQ:AMOT) in early January post the company's third-quarter earnings when we issued a "Buy" signal on the stock (Through the use of a trailing stop-loss). The reasons for our bullishness at the time were due to the strong earnings beat in Q3 and how the company's key gross margin metric was trending upward. Although shares managed to rally some 6% post our buy recommendation, they could not build up sufficient momentum to break out above overhead resistance which they encountered in early March (Shown Below). Suffice it to say, considering how selling volume has come to the fore in recent sessions, we do not foresee another breakout in the immediate future. Therefore, we are reverting back to a "Hold" stance and will reconsider our options if indeed overhead resistance eventually gets taken out to the upside.

AMOT Technical Chart (Stockcharts.com)

Q4 & Fiscal 2022 Growth Trends

Now the bulls may state that they intend to use AMOT stock's lower prices in order to average down on their existing positions. In fact, one does not have to look further than the company's recently announced fiscal 2022 numbers to see the strong fundamentals Allied Motion Technologies has going for it. Top-line growth of 35% & organic growth of 18% in the company's most recent fourth quarter pushed full-year fiscal 2022 revenues to $503 million. Furthermore, bulls will be encouraged that the six acquisitions which the company undertook in late 2021 & mid-2022 (Although being margin accretive) were not the sole reason for the aggressive jump in top-line sales. Organic growth for the year for example (On the back of solid performances within the Industrial & Aerospace defense segments) came in at 12% which was a solid result given the challenging trading conditions AMOT had to cope with.

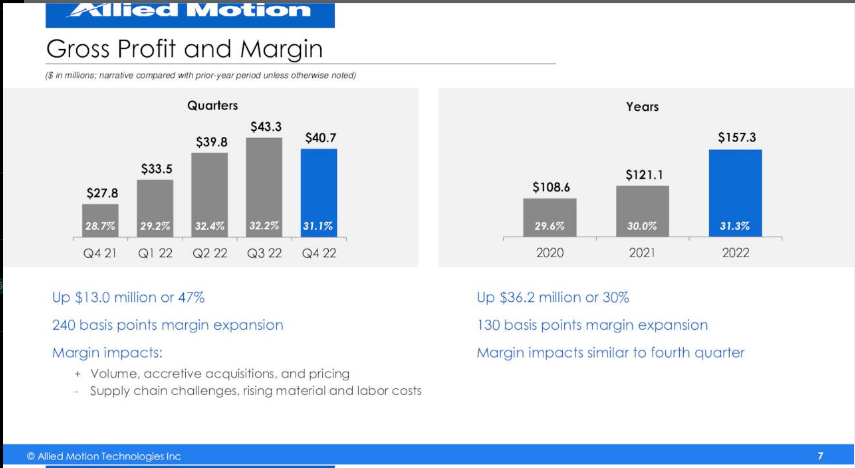

Furthermore, bulls will have been encouraged by the 30% increase in gross profit which outpaced the company's revenue growth for the year (25%). Moreover, the gross margin expansion (130 basis points) increased the full-year gross margin percentage to 31.3%. This is a key trend from a bullish standpoint as AMOT's trailing net earnings margin of 3.46% remains well below the average in this sector (6.35%). Suffice it to say, a 1% drop in AMOT's gross margin could easily result in the corresponding net profit margin (Assuming costs cannot be taken out of the system) dropping to a corresponding 2.46%. This is obviously not what investors want which is why margin-accretive acquisitions are what will be continually sought after.

Allied Motion: Gross Profit Trends (Seeking Alpha)

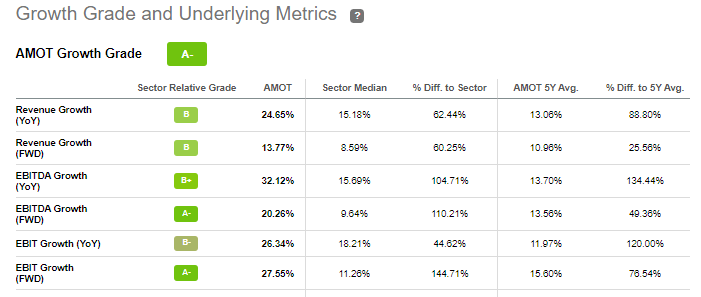

Fortunately, management believes that higher-than-average operating costs are principally acquisition led which means they should improve over time as those recent acquisitions get properly embedded within the company as a whole. This is the point though, isn't it? The market will continue to give AMOT the benefit of the doubt (When it comes to how forward-looking earnings will play themselves out) as long as key metrics such as top-line growth & gross margin growth remain intact. As we can see below, AMOT has been reporting excellent growth numbers which is the reason why shares tested their 2022 highs in March of this year.

AMOT Growth Trends (Seeking Alpha)

Suffice it to say, although as mentioned AMOT reported 12% organic top-line growth in fiscal 2022, you can bet that ongoing M&A activity by means of strategic acquisitions simply MUST take place in order to keep those growth metrics intact.

Growth Brings Risk When It Is Fueled By Debt

Now in saying this, followers of our work will be aware that we believe growth metrics many times are over-emphasized. However, in companies such as AMOT where its forward GAAP multiple comes in at a very elevated 23.70, investors NEED to remain focused on the company's growth path to ensure the company can remain healthily profitable over time. The cash-flow statement where we see reduced operating cash flow of $5.6 million in fiscal 2022 also demonstrates that debt will most likely need to go higher if AMOT remains aggressive with its M&A strategy.

Suffice it to say, the key to AMOT's forward-looking success will be the following. As the company continues to acquire more companies by means of debt, it will be taking on more goodwill and intangible assets which will inevitably come with those purchases. Now, although the company's debt-to-capital ratios may not change much (As AMOT's assets will increase alongside the higher debt load), the taking on of more debt, goodwill & intangibles all increase the risk for the investor over the long term. Therefore growth simply has to continue to justify that increasing leverage as well as the pretty high valuation mentioned earlier.

Conclusion

To sum up, AMOT couldn't muster up the required momentum to punch through overhead resistance earlier this month. Although the company's growth metrics remain to the fore, higher earnings and specifically cash flow are required to essentially finance this growth. Let's see what Q1 brings. We look forward to continued coverage.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.