Primoris Services Corp: Promising Investment Opportunity, Strong Growth Prospects

Summary

- PRIM’s revenue growth should benefit from the healthy order backlog and acquisition of PLH in the near term.

- In the long term, the company should benefit from the healthy growth opportunities across its end markets, including energy, renewables, communications, and oil & gas.

- PRIM stock is currently undervalued.

LeoPatrizi

Investment Thesis

Primoris Services Corporation (NASDAQ:PRIM) should see a boost in revenue in 2023, thanks to its strong order backlog levels and the recent acquisition of PLH. The company has secured $290 million worth of projects related to the construction of solar facilities in the Midwest, which is in line with the growing trend toward renewable energy. Additionally, the government's tax credits for renewable energy, funding for communication infrastructure development, and investments in oil and gas pipelines should provide long-term benefits for PRIM. The company's attractive valuations and promising growth prospects make it a good investment opportunity.

Financial Performance Review

In 2022, PRIM’s revenue grew 26% Y/Y to $4.4 billion with 15% organic growth. The revenue growth was primarily driven by a healthy solar market, the expansion of PRIM’s communication services, and the acquisitions of PLH and B Comm. The revenue in the Utilities segment increased 22% Y/Y due to the acquisitions of PLH and B Comm and increased activity across the power and communications end markets. PRIM acquired PLH Group (PLH) in August 2022 to expand its capabilities in the utility markets, including power delivery, communications, and gas utilities. PLH is a utility-focused specialty construction company with a presence across the United States. PRIM acquired B Comm in June 2022 to expand its communications services in the utility markets. B Comm is a provider of maintenance, repair, upgrade, and installation services in the communications market. The revenue in the Energy/Renewables segment grew by 48.2% Y/Y due to the strong solar EPC business and the acquisition of PLH, partially offset by supply chain constraints. The Pipeline segment’s revenue declined by 28.4% Y/Y due to the substantial completion of pipeline projects in 2021 and a decline in midstream pipeline market demand.

The company’s gross margin in 2022 declined by 160 bps Y/Y to 10.3% due to the closeout of multiple projects in the Pipeline segment in 2021 and increased labor and fuel costs in the Utilities segment. The adjusted EBITDA margin declined 210 bps Y/Y to 6.4% due to the lower gross margins and increased SG&A expenses due to the integration of PLH.

Near-term Outlook

PRIM’s order backlog grew by $1.5 billion, or 37% Y/Y to $5.5 billion in 2022, with $570 million of the increase coming from acquisitions. The backlog in the Utilities, Energy/Renewables, and Pipeline segments grew by 32%, 29%, and 197% Y/Y, respectively. The Utilities segment’s order backlog benefited from the acquisitions of B Comm and PLH. The company was able to add new customers in the Central Texas region with the communication services provided by B Comm. In the Energy/Renewable segment, the company secured $400 mn worth of projects in Q4 FY22, including two $100 mn power projects and four $200 mn heavy civil construction projects. In the Pipeline segment, the company secured a large pipeline project in Q3 FY22, valued at more than $120 million. This project involves constructing approximately 60 miles of pipeline in Texas.

Looking ahead, I am optimistic that the company's order backlog will continue to reap the rewards of the robust demand in the communications and renewable energy markets, specifically solar energy. The increased shift towards renewable energy post-Ukraine war has benefited the company. PRIM has recently secured multiple solar projects worth $290 million, covering the engineering, procurement, and construction of utility-scale solar facilities in the Midwest. In the communications market, the need for better connectivity has driven the deployment of fiber and 5G across the United States. These developments should drive the company's revenue in the near-to-medium term. Despite facing supply chain constraints, notably in the delivery of solar modules, which has affected the company in the last few quarters, the situation is gradually improving in 2023, and this should benefit the company. Overall, I believe the company’s revenue in 2023 should benefit from the healthy order backlog, supply chain improvements, and the acquisition of PLH.

On the margin front, the company should benefit from declining SG&A expenses. With the completion of PLH’s integration into PRIM’s business and the elimination of duplicate overhead costs, the adjusted EBITDA margin should improve. Based on my revenue growth estimate of 22% for 2023 and the midpoint of management’s adjusted EBITDA guidance range of $350 mn to $370 mn, the adjusted EBITDA margin should improve by 30 bps Y/Y to 6.7% in 2023.

Medium and Long-term growth prospects

PRIM serves several end markets, including renewable energy, communications, power delivery, electric and gas utility, industrial, and oil & gas. These markets are experiencing significant medium- to long-term opportunities, which should benefit the company. PRIM's Energy/Renewable segment should reap the benefits of the growing demand for renewable energy sources. As the need for power continues to increase, more power generation facilities are being developed that rely on renewable energy sources. Furthermore, the Inflation Reduction Act (IRA) has spurred an influx of capital investment in renewable projects by offering tax incentives for wind and solar facilities, as well as provisions for green hydrogen.

In the Utilities segment, the increasing demand for electricity and the expansion and modernization of the electric grid in the United States should benefit the company. Recently, the Department of Energy (DOE) announced $13 billion in funding to upgrade the existing grid and build a new transmission line. The funding includes $10.5 billion in funding under the Grid Resilience and Innovation Partnership (GRIP) program and $2.5 billion under the Transmission Facilitation Program. The segment should also benefit from the developments in the communications market. The Infrastructure Investment and Jobs Act (IIJA) and several state funds are provided to construct and improve broadband infrastructure across the United States. In the Pipeline segment, the company should benefit from the regulatory measures around the maintenance, repair, and inspection of pipelines in the oil and gas industry.

The healthy trends across all of PRIM's end markets should benefit revenue growth in the medium- to long-term.

Balance Sheet & Cash Flow Analysis

The long-term debt at the end of 2022 was $1.14 billion, with net debt under $900 million. The net debt to EBITDA ratio was 3x compared to 3.25x at the end of the third quarter of 2022. Management is planning to bring down its leverage ratio to 2x by the end of 2024 by paying off its debt and improving EBITDA. This move towards a more sustainable financial position will position PRIM to pursue additional acquisitions like PLH Group and expand its utilities business. With adequate liquidity on hand, I am optimistic that the company can execute its growth strategy effectively

The capital expenditure in 2022 was $95 million, which was lower compared to the prior year’s $135 million. The company anticipates CapEx to be between $80 mn and $100 mn in 2023, of which 50% will be utilized for new equipment to meet the demand in its end markets and the remaining for maintenance of equipment.

Valuation

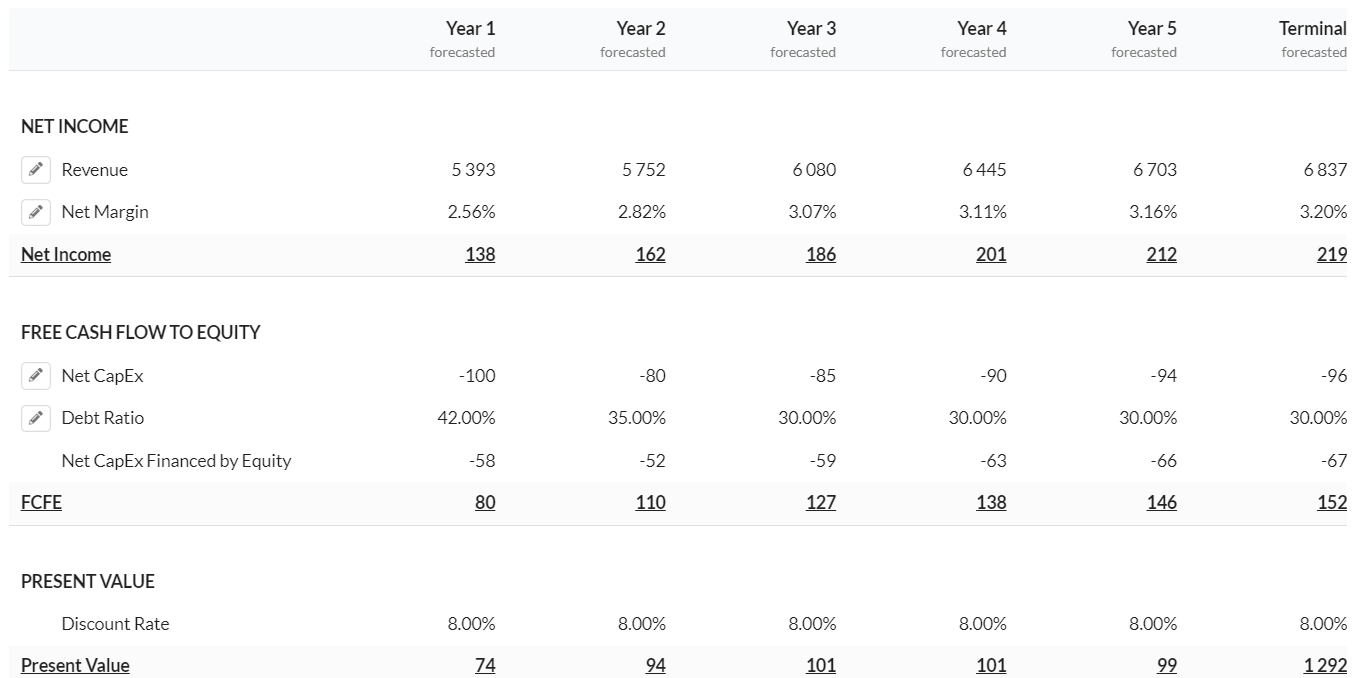

DCF valuation (Created by DzD Analysis using Alpha Spread)

In my DCF calculations, I am assuming revenue growth to be in double digits in 2023, given the healthy order backlog and the acquisition of PLH. Beyond 2023, I have assumed growth to be high single digits, with a terminal growth rate at mid-single digits. I have assumed the debt ratio to decline as the company pays off its debt and reaches its historical levels of 30% in the long term. I used a discount rate of 7.86% by using the cost of equity of 9.85% and a cost of debt of 3.95%, which is below the industry level, and arrived at a fair value of $33.17 for PRIM.

Using the relative valuation, the stock is currently trading at 8.97x FY23 consensus EPS estimate of $2.65 and 7.39x FY24 consensus EPS estimate of $3.21, which is below its five-year average forward P/E of 11.98x.

Conclusion

To sum it up, I am bullish on PRIM stock, as I see the potential for an approximately 40% increase in stock price. The company has a robust order backlog that will likely benefit its revenues in the short term, in addition to the recent acquisition of PLH. As PRIM continues to pay down its debt and improve its leverage ratio, it should be better positioned to pursue more acquisitions and expand its business further. Looking ahead, PRIM has solid growth prospects that should support long-term revenue growth, and I believe the company is well-positioned for future success.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.